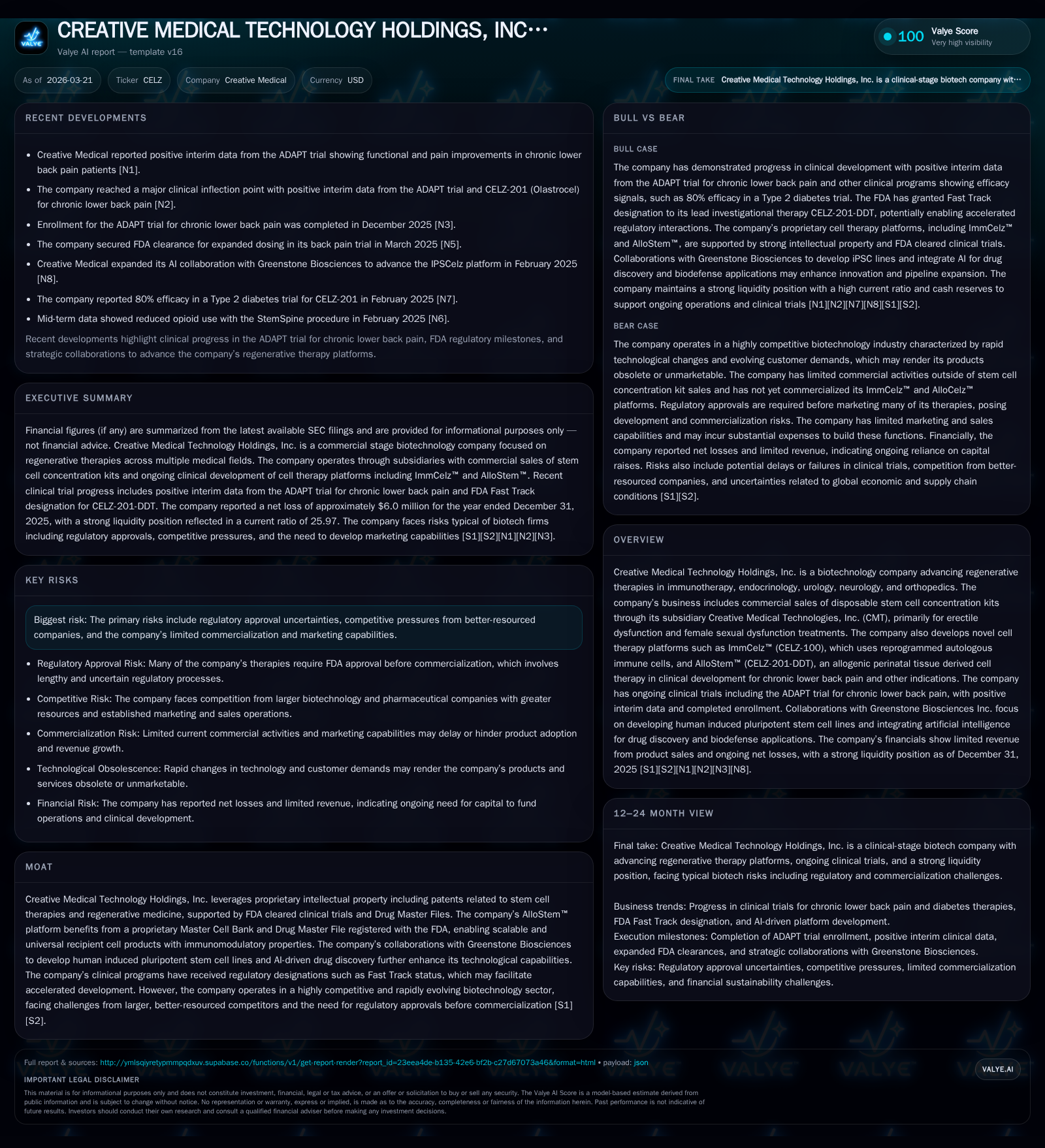

Creative Medical Technology Holdings' Progress Amidst Ongoing Development and Capital Challenges

CELZ advances regenerative cell therapy platforms while navigating sustained operating losses and capital requirements.

Creative Medical Technology Holdings, Inc. (CELZ) continues to develop innovative regenerative therapies through its proprietary stem cell platforms and active clinical trials. The company’s financial history shows minimal commercial revenues primarily from CaverStem® kits, alongside persistent operating losses driven by clinical trial investments and research and development expenditures. CELZ holds valuable intellectual property assets, FDA-registered Drug Master Files, and strategic collaborations but faces challenges related to scaling commercialization, regulatory complexities, competitive pressures, and ongoing funding needs. Upcoming clinical milestones and financing activities will be key indicators of its future trajectory in the evolving biotechnology sector.

Historical Financial Overview: Revenue and Operating Results

Creative Medical Technology Holdings (CELZ) generates revenue primarily through sales of disposable stem cell concentration kits under the CaverStem® brand. Revenues have been minimal and declined from $11,000 in 2024 to $6,000 in 2025 [F1], illustrating limited market penetration.

Operating income remains significantly negative due to heavy investments in clinical trials and research activities. Operating losses increased modestly to approximately -$6.14 million in 2025 from -$5.74 million in 2024 [F1], with net losses following a similar trend (-$5.99 million in 2025).

The following table summarizes key financial metrics:

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 6000 | -6 | -6 | -6 | -45.5% | -9.1% |

| 2024 | 11000 | -5 | -5 | -6 | +22.2% | -3.9% |

| 2023 | 9000 | -5 | -8 | -6 | -89.8% | +47.9% |

| 2022 | 88600 | -10 | -8 | -10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | 10000 | -79.8 |

| 2024 | 174964 | -86.6 |

| 2023 | 270952 | -51.1 |

| 2022 | -63.9 |

Source: SEC companyfacts cache [F1].

Drivers of Operating Losses and R&D Investments

The company's ongoing operating deficits stem largely from substantial research and development expenses totaling roughly $2.26 million for the year ended December 31, 2025 [S3]. These expenses support multiple clinical programs including Phase I/II trials such as the AlloStemSpine® CELZ-201 ADAPT trial targeting chronic lower back pain.

CELZ’s therapeutic approach involves both autologous therapies like ImmCelz™ where patients’ immune cells are extracted and "reprogrammed" ex vivo before reinfusion [S1], as well as allogenic therapies under the AlloStem™ platform that utilize a proprietary Master Cell Bank registered with the FDA via a Drug Master File to enable off-the-shelf universal cell products [S6][S10].

Despite this innovative pipeline differentiation relative to competitors with greater resources [S11], commercial sales remain negligible due to limited marketing capabilities and capital constraints impeding scale-up efforts [S10].

Clinical Pipeline and Regulatory Progress

Key clinical milestones include:

- Type I Diabetes candidate (CELZ-201 CREATE-1), which has received regulatory approval for clinical trials [S1].

- Completion of enrollment for the AlloStemSpine® CELZ-201 ADAPT trial addressing chronic lower back pain with positive interim results anticipated [S1][S10].

- Strategic collaboration with Greenstone Biosciences on developing human induced pluripotent stem cell (iPSC) lines designed to accelerate product development timelines by an estimated two to three years while enabling viral-free biologics production [S1].

These developments align with regulatory strategies aiming for accelerated approvals such as Fast Track designations , although commercial revenues remain contingent on successful trial outcomes.

Capital Allocation and Financial Position

Since 2021 CELZ has raised over $40 million gross through securities offerings including warrant exercises that generated net proceeds of approximately $3.7 million in early 2025 [S1][S5]. As of December 31, 2025 cash balances stood at about $7.2 million against annual cash used in operations near $6 million reflecting limited runway without additional financing [F1][S1].

Share repurchases amounted to just $10 thousand during the first half of 2025 compared with approximately $175 thousand repurchased during full-year 2024 highlighting conservative capital deployment prioritizing liquidity preservation amid ongoing development needs [F1][S5].

Return on equity remains negative at approximately -80% based on net loss relative to equity at year-end 2025 consistent with investment-phase biotech companies without meaningful commercial revenues yet realized [F1].

Intellectual Property and Competitive Positioning

CELZ’s intellectual property portfolio comprises patents covering stem cell therapies initially focused on erectile dysfunction but expanded into broader immunotherapy applications under platforms like ImmCelz™ [S6]. The FDA Drug Master File supporting their proprietary allogenic Master Cell Bank further strengthens manufacturing exclusivity enabling scalable cellular therapy production [S6][S10].

Collaborations extending biological capabilities via iPSC line development enhance potential pipeline diversity beyond current indications.

Patent litigation risk exists as a typical industry challenge requiring ongoing enforcement efforts to preserve competitive advantages [S6].

Risk Factors: Regulatory Landscape and Market Challenges

The company faces multiple risks including:

- Complex evolving regulations worldwide governing cell therapies with uncertain implementation creating potential barriers for international expansion [S3].

- Limited reimbursement pathways for autologous products like CaverStem® kits necessitating out-of-pocket payments by patients which constrain market adoption [S4][S19].

- Dependence on successful clinical trial outcomes; delays or negative results could extend timelines or impede commercialization prospects [S19].

- Competition from larger biotech firms with greater R&D budgets threatens market share especially if competitors develop safer or more effective treatments targeting similar indications such as chronic lower back pain or autoimmune diseases addressed by CELZ's platforms [S11].

- Limited internal sales infrastructure requiring external partnerships or investment amidst constrained capital resources impeding commercialization scale-up efforts [S10].

Outlook: Key Catalysts to Monitor

Investors should watch for:

- Data readouts from the ADAPT trial evaluating the AlloStemSpine® candidate providing efficacy and safety signals critical for next-phase development.

- Advances toward scalable manufacturing leveraging FDA Drug Master File-backed Master Cell Bank technologies alongside iPSC-derived biologics.

- Additional fundraising activities including equity or debt offerings indicating management’s ability to secure capital necessary for continued operations.

- Potential strategic partnerships or licensing agreements leveraging CELZ’s intellectual property portfolio enhancing market access or financial stability.

In summary, CELZ operates at the intersection of innovative regenerative medicine development coupled with typical early-stage biotech financial challenges requiring prudent capital management amid competitive industry dynamics.

This analysis is based on publicly filed SEC documents through March 20th, 2026 together with company disclosures; it reflects historical financial data without projecting future stock performance or providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments