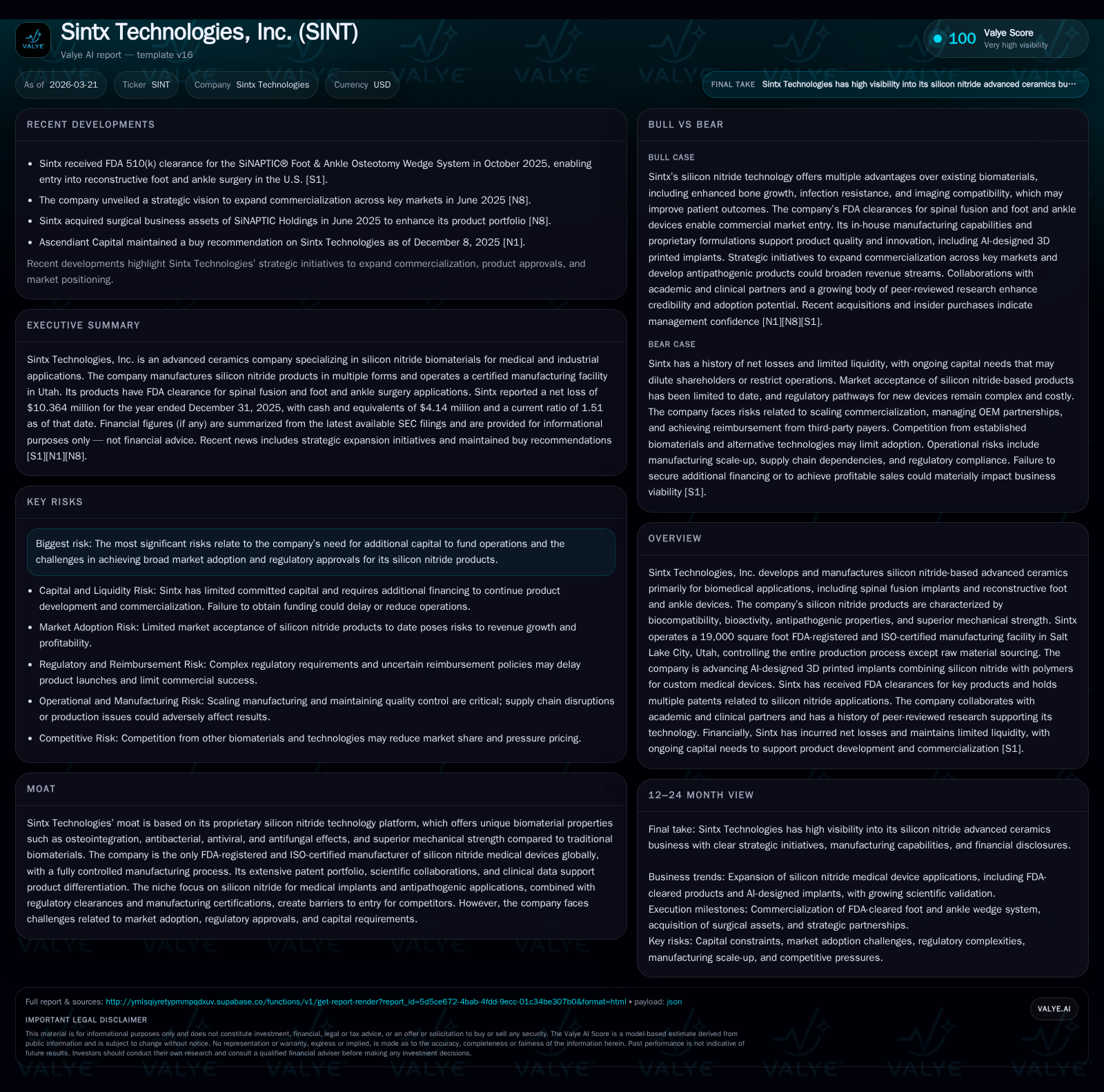

Sintx Technologies' Struggle and Potential in Silicon Nitride Biomaterials

Sintx blends pioneering silicon nitride implant technology with financial hurdles as it pursues commercial scale and regulatory milestones.

Sintx Technologies offers a distinctive silicon nitride platform delivering biocompatible, antibacterial medical implants with FDA clearance for spinal and foot applications. While its proprietary biomaterial properties and controlled manufacturing create a technical moat, the company is entrenched in significant operating losses, negative cash flows, and capital constraints, requiring additional financing to advance commercialization. Key near-term dynamics include regulatory milestones for product approvals, adoption challenges in orthopedic markets, and evolving commercialization strategies involving AI-driven 3D printed implants. Monitor upcoming clinical validations, sales scaling efforts, and funding access as critical indicators of Sintx's path toward sustainable growth.

Sintx Technological Edge: Silicon Nitride’s Unique Properties and Applications

Sintx Technologies centers its innovation on a proprietary silicon nitride (Si3N4) ceramic platform engineered for advanced biomedical applications. Silicon nitride implants offer attributes rare among biomaterials: superior osteointegration facilitating bone ingrowth; intrinsic antibacterial, antiviral, and antifungal activity reducing infection risks; outstanding mechanical strength and fracture resistance; biocompatibility; resistance to corrosion; and radiolucency enabling improved diagnostic imaging. These qualities support durable spinal fusion implants alongside reconstructive devices such as foot and ankle wedges cleared by the FDA's 510(k) pathway in October 2025.

The company’s tightly controlled manufacturing facility in Salt Lake City is both FDA-registered and ISO-certified, qualifying Sintx as the sole global producer of silicon nitride medical devices with comprehensive production oversight save raw material sourcing [S1]. Clinical publications have validated silicon nitride’s antipathogenic properties and bioactivity extensively. This combination anchors a durable moat given competing biomaterials—metal alloys or polymers—lack such integrated antibacterial action or osteophilic character without coatings or additives.

Evolving Revenue Trends and Past Segment Performance

Historically, Sintx has witnessed notable revenue contraction: top-line peaked at $22.7 million in fiscal 2014 before declining to approximately $11.2 million by fiscal 2017—a near 50% two-year drop driven by limited market penetration of silicon nitride products [F1]. This decline reflects challenges typical of breakthrough materials requiring physician education, reimbursement acceptance, and competitive positioning against established implant technologies.

More recently, despite efforts to broaden application areas, revenue data after 2017 are unavailable explicitly but operating losses highlight financial strain persisting through at least fiscal year-end 2025 where operating income was negative $10.7 million, albeit improved by nearly 24% versus prior years [F1]. Net income followed a similar pattern with a loss of $10.36 million in the same period.

Operating cash flows remain significantly negative at -$8.57 million for the year ending December 31, 2025 and capital expenditures have been curtailed aggressively (down ~73% YoY), pointing to stringent cost containment amid shrinking revenues [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -10 | -9 | -11 | 185000 | +6.0% |

| 2024 | -11 | -9 | -14 | 690000 | -33.5% |

| 2023 | -8 | -14 | -13 | 530000 | +31.4% |

| 2022 | -12 | -10 | -11 | 1405000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -9 | -353.8 |

| 2024 | -9 | -283.1 |

| 2023 | -15 | -94.2 |

| 2022 | -12 | -211.1 |

Source: SEC companyfacts cache [F1].

Note: Operating income and net income only available for later years per latest filings [F1].

Critical Impact of Regulatory Milestones on Market Expansion

Regulatory clearances form a pivotal growth catalyst for Sintx. The October 2025 FDA clearance for the SiNAPTIC® Foot & Ankle Osteotomy Wedge System marked an important entry into reconstructive foot/ankle surgery within the U.S., expanding beyond spinal fusion implants that have been commercialized since approximately 2008 across various international markets [S1]. This clearance through the FDA’s less onerous but rigorous 510(k) pathway denotes substantial equivalence to predicate devices but typically relies heavily on bench testing rather than extensive long-term clinical trials — potentially limiting initial adoption until clinical evidence accumulates further [S13][S19].

Nonetheless, regulatory pathways remain fraught with uncertainty including risks of shifting FDA requirements such as transitioning from Quality System Regulation (QSR) to Quality Management System Regulation (QMSR), enhanced post-market surveillance obligations, potential need for investigational device exemptions (IDE) for certain studies, or reconsideration of predicate device status [S13]. Outside the U.S., diverse international standards including EU MDR impose added validation demands that can delay or restrict access [S6].

Failure to maintain clearances or meet evolving standards could materially constrain market access or increase costs significantly.

Capital Access and Financial Health: Navigating Cash Flow and Funding Needs

As of December 31, 2025, Sintx reported only $4.14 million cash on hand augmented by an At-The-Market stock offering program initiated in October 2025 with approximately $6 million capacity remaining under a $6.4 million umbrella facility [S1][F1]. Ongoing operations burn through over $8.5 million annually in operating cash flow while capex demands are minimal (~$185k), underscoring an unsustainable cash consumption rate absent new capital injections.

With equity down from nearly $8.77 million at end-2023 to roughly $2.93 million at end-2025 accounting for accumulated losses, solvency metrics erode correspondingly while dilution risks intensify should further stock issuances occur [F1]. Failure to secure timely financing would force deferral or discontinuation of R&D programs critical to pipeline progression and commercial scale-up activities.

Intellectual Property Strengths versus Market Adoption Barriers

Sintx holds multiple patents covering specific applications of silicon nitride biomaterials paired with trade secrets governing manufacturing processes ensuring competitive edge [S4][S6]. However, no patent covers the fundamental composition of matter for their solid silicon nitride or all production facets leaving room for competitors to develop analogous formulations without infringing established patents [S16].

Such gaps heighten reliance on know-how protection mechanisms including confidentiality agreements with employees and collaborators along with extensive clinical data contributing to product differentiation.

Further complexity arises from potential litigation risks given industry prevalence of intellectual property disputes over orthopedic device technologies that may divert management focus while incurring legal costs [S10][S12][S16]. Adoption is tempered not only by patent landscape ambiguities but also by entrenched competition from legacy metallic implants widely reimbursed across healthcare systems.

Strategic Focus on AI-Designed Custom Implants and Product Pipeline

In response to stiff competition and unmet clinical needs for tailored solutions, Sintx is advancing additive manufacturing capabilities integrating AI-driven design algorithms that combine silicon nitride ceramics with polymers enabling patient-specific customized implants [S1]. This innovative engineering approach targets markets demanding precision fit implants which traditional mass-production methods cannot address effectively.

The intersection of AI design optimization with advanced biomaterial functionality builds upon Sintx’s core technological moat while expanding into higher-value segments within orthopedics deserving bespoke device geometry combined with inherent antipathogenic properties.

This initiative aligns well with emerging trends favoring digital health integration in medtech device development but remains contingent on successful scale-up validation alongside regulatory clearances.

Financial Forecasting: What Metrics to Watch Going Forward

Explicit forward guidance is absent from recent SEC filings; however key indicators warrant monitoring as proxies for near-term progress:

- Regulatory updates regarding additional FDA clearances or approvals particularly outside spinal/foot domains,

- Sales trends linked to newly cleared products such as SiNAPTIC foot wedge adoption,

- R&D expenditures indicating pipeline investment trajectory,

- Capital raises evidencing successful funding access or dilution events,

- Operating cash flow improvements signaling scalability gains. Future capital requirements loom large influencing pace of development/commercial rollout given existing liquidity shortfalls [S1].

Operational Efficiency: Cost Controls, Capex Trends, and Profitability Pathways

Sintx has trimmed capital spending year-over-year almost three-quarters from $690k in FY24 to just $185k in FY25 demonstrating heightened cost vigilance amidst persistent top-line pressure [F1]. Though operating losses remain sizable (-$10.7M in FY25), incremental improvement relative to prior years (+23.7% op inc YOY) shows tentative operational leverage.

That said return on equity remains deeply negative (~-354%) reflecting accumulated deficit burdens burdening shareholder value despite underlying personnel effort toward tightening expenses. The sustained negative free cash flow (>-$8M annually) underscores earnings challenges balancing R&D intensity required to break commercialization bottlenecks against cost-cutting limits.

Compliance Complexities in Healthcare Distribution and Sales Practices

Sintx operates within an intricate U.S. regulatory framework governed by healthcare fraud-and-abuse laws including federal Anti-Kickback Statute prohibiting incentives tied to federal healthcare program referrals; False Claims Act exposing companies to liability from fraudulent government claims; HIPAA privacy/security mandates concerning health information; Physician Payments Sunshine Act requiring disclosure of payments/transfers of value to physicians; alongside comparable state statutes imposing added restrictions [S4][S6][S7].

Additional regulatory burdens derive from distribution channel management where OEM partnerships complicate compliance oversight enforcing strict anti-collusion practices along with alignment of incentives across hospital customers and surgical professionals [S17]. Noncompliance risks encompass steep financial penalties plus reputational damage illustrating the necessary balance between aggressive commercialization efforts versus rigorous legal adherence.

Internationally divergent medical device regulations add layers of complexity ranging from EU MDR certifications imposing expanded clinical evidence requirements to country-specific customs controls affecting export/import licensing sustainability presenting ongoing operational overhead risk exposures [S6][S20].

This analysis synthesizes publicly available SEC filings alongside company disclosures as of March 2026 without forecasting future stock performance or issuing investment recommendations. Readers are advised that Sintx Technologies’ highly specialized market position coupled with significant financial resource dependencies mark it as an enterprise balancing breakthrough medical innovation against execution risks common within early-stage medtech ventures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments