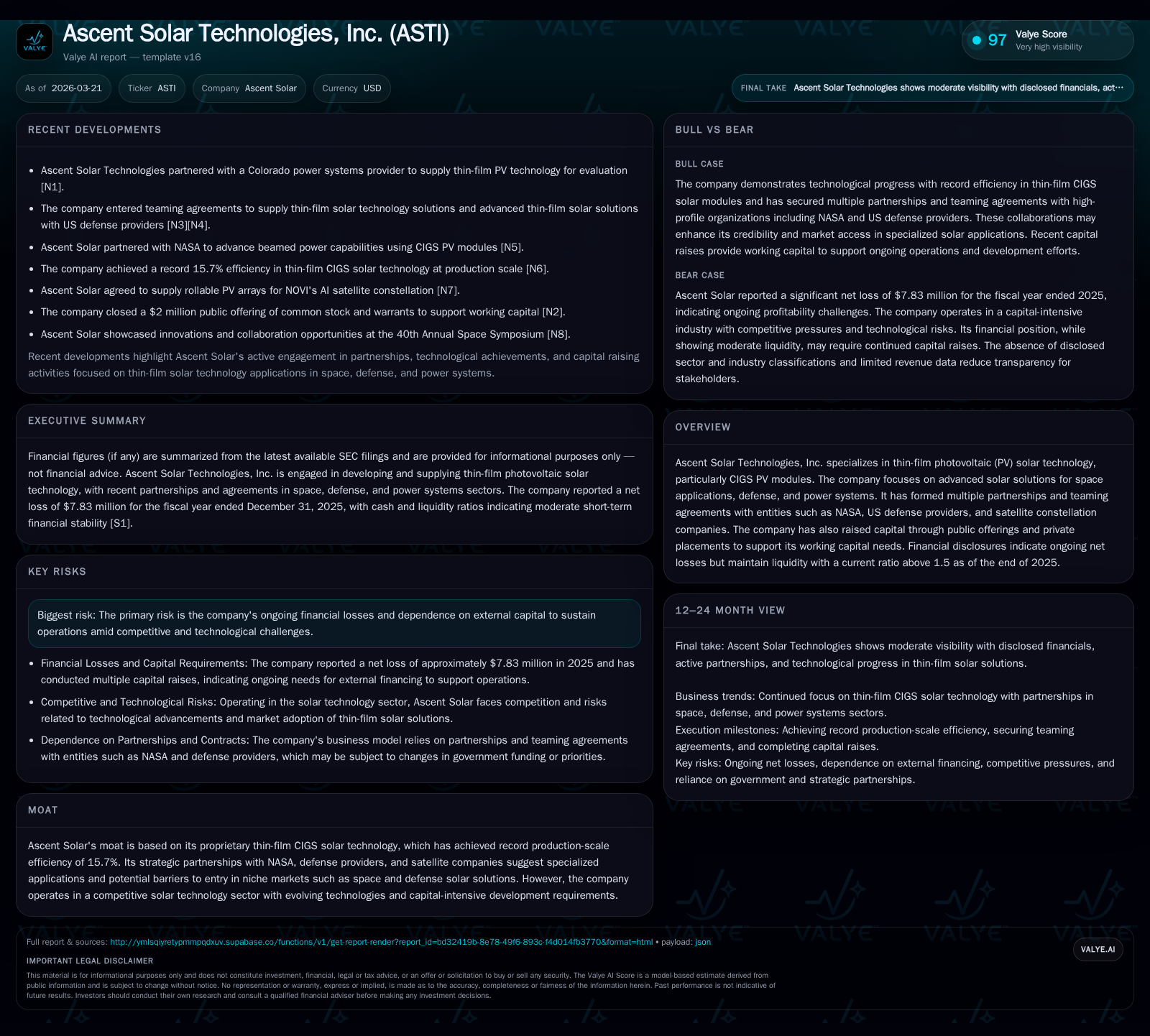

Ascent Solar Technologies Advances Flexible CIGS Modules Amid Reduced Operating Losses and Strategic Aerospace Deals

The company narrows losses and sustains liquidity through private placements while leveraging specialized thin-film solar technology for aerospace and defense applications.

Ascent Solar Technologies leverages its patented flexible CIGS photovoltaic technology to serve niche aerospace and defense sectors. Despite persistent net losses, the company has reduced operating losses year over year and maintains sufficient liquidity supported by recent private placements. Strategic partnerships underpin its specialized market positioning, while SEC filings highlight risks tied to capital needs and competitive pressures.

Financial Performance Overview

Ascent Solar Technologies reported an operating loss of approximately $7.87 million for fiscal year 2025, improving from an $8.54 million loss in the previous year — a reduction of 7.8% that indicates progress in managing costs despite continued unprofitability [F1]. Net losses also narrowed by around 14.2%, from roughly $9.13 million in FY2024 to about $7.83 million in FY2025. Revenue data beyond 2011 is unavailable; the last reported figure was approximately $3.95 million in that year [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -8 | -7 | -8 | 0 | +14.2% |

| 2024 | -9 | -8 | -9 | 0 | +46.5% |

| 2023 | -17 | -10 | -16 | 4 | +13.6% |

| 2022 | -20 | -11 | -17 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | -234.7 |

| 2024 | -8 | -270.1 |

| 2023 | -13 | 1118.2 |

| 2022 | -11 | -430.8 |

Source: SEC companyfacts cache [F1].

Note: Revenue is only reported for FY2011; subsequent years' data is not disclosed.

Technological Differentiation

The company's core asset is its proprietary copper indium gallium selenide (CIGS) thin-film photovoltaic technology. Production-scale efficiencies have reached up to approximately 15.7%, establishing a competitive edge in manufacturing flexible and lightweight solar modules vital for aerospace applications where weight savings are paramount . This technology supports use cases including satellite constellations and defense platforms.

Strategic Market Positioning

Partnerships with NASA and U.S. defense contractors provide Ascent Solar with tailored revenue sources within specialized aerospace markets less exposed to typical price competition seen in commercial solar sectors . These relationships also facilitate compliance with stringent regulatory standards and foster co-development opportunities that mitigate individual investment risks.

Capital Structure and Liquidity

Ascent Solar continues to depend on equity financing to support operations amid ongoing losses. Private placements conducted through early 2026 generated net proceeds near $9 million after fees [S11–S17]. Since mid-2024 under-at-the-market offerings have raised over $11 million gross proceeds [S18]. At fiscal year-end 2025, the company held approximately $2.79 million in cash and equivalents with a current ratio of about 1.53 — indicating reasonable short-term liquidity coverage [F1].

No dividends or share repurchases have been reported; capital allocation focuses on sustaining research efforts and operational needs.

Operational Efficiency Trends

Year-over-year improvements in operating income and operating cash flows reflect incremental efficiency gains despite continued negative free cash flow driven by capital expenditures [F1]. Capex declined sharply from a peak of nearly $3.86 million in FY2023 to around $32 thousand in FY2025 suggesting a shift from heavy investments toward more controlled spending.

Risk Factors and Outlook

SEC filings highlight risks related to sustained losses requiring continuous external funding and competitive challenges from emerging photovoltaic technologies necessitating ongoing R&D investment [S4–S8].

Without explicit company guidance or forecasts available publicly, key near-term milestones include contract renewals with aerospace clients and certification achievements validating product suitability for space applications — critical steps toward commercial scalability.

This analysis is based exclusively on publicly available SEC filings ([S#]) and financial data ([F1]), supplemented by Valye research excerpts focusing on technology and partnerships; no speculative projections are included.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments