Solarius Capital Acquisition Corp.’s IPO Strategy and SPAC Execution Risks Through Early 2026

Solarius Capital Acquisition Corp. raised $172.5 million via a SPAC IPO targeting asset and wealth management businesses but faces execution and timing risks.

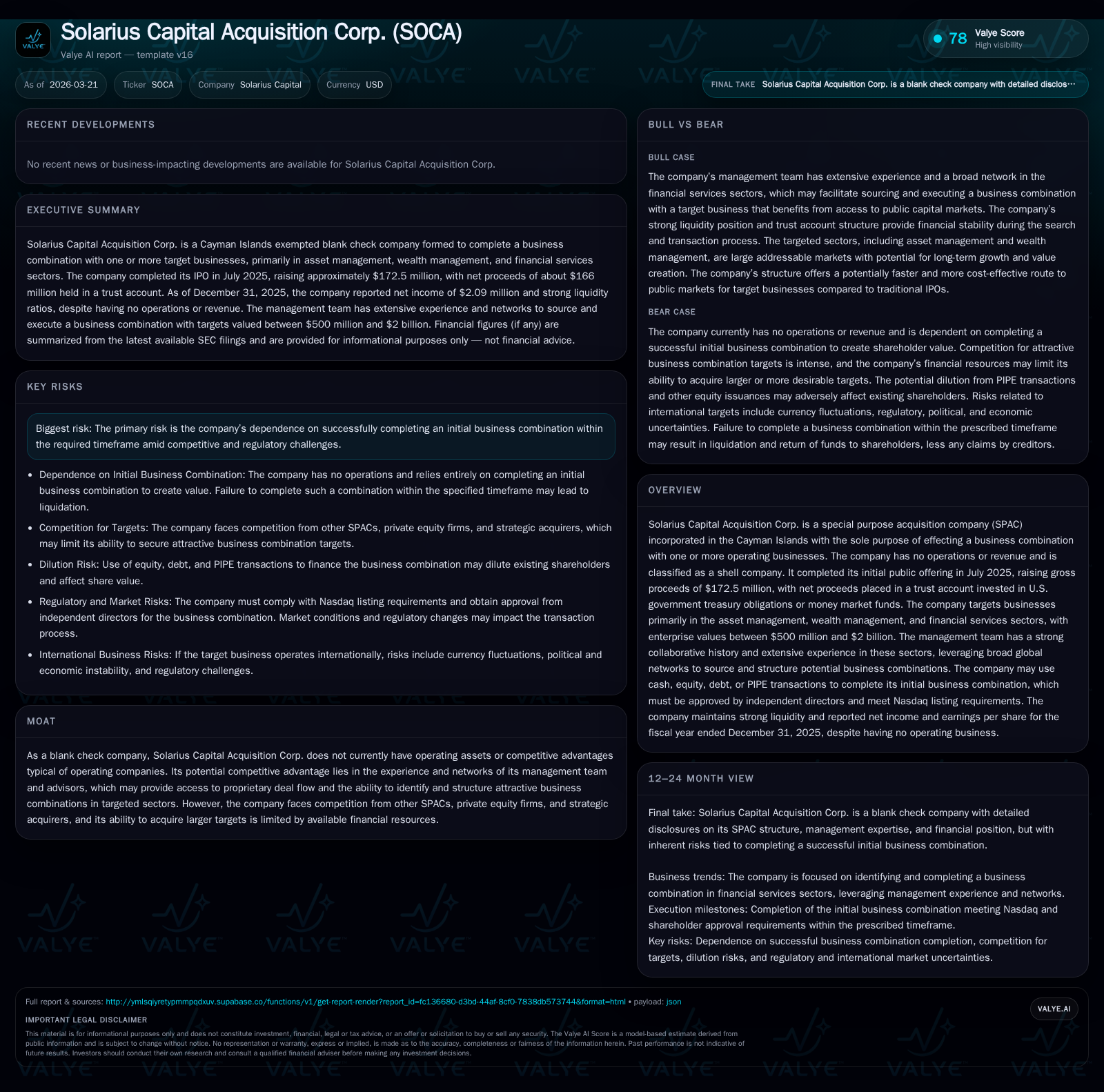

Formed as a Cayman-Islands-based blank check company, Solarius Capital Acquisition Corp. completed its initial public offering in mid-2025, raising gross proceeds of $172.5 million to pursue acquisitions in financial services sectors. Its management team’s extensive experience and network are posited as competitive advantages in sourcing deals valued between $500 million and $2 billion. However, the firm has yet to generate revenue or complete a business combination, facing inherent SPAC risks including shareholder redemption pressures, potential conflicts of interest, and a limited timeframe to consummate an acquisition. Financial statements show minimal operating activity to date, with net income reflecting minor gains attributable mostly to non-operating factors.

Company Overview

Solarius Capital Acquisition Corp. (SOCA) is a special purpose acquisition company incorporated as an exempted company in the Cayman Islands with the sole objective of effecting one or more business combinations.[S1] Having no operating history, revenues, or ongoing business activities, SOCA qualifies as a shell company under the U.S. Exchange Act definition.[S1]

The firm completed its initial public offering on July 17, 2025, raising gross proceeds of approximately $172.5 million through issuance of 17.25 million units priced at $10 per unit. This included an over-allotment exercise of 2.25 million units.[S1][S6] Net IPO proceeds after underwriting fees (~$7.35 million) were placed into a trust account invested conservatively in U.S. government treasury obligations with maturities of less than 185 days or money market funds.[S20]

SOCA targets acquisition candidates primarily within asset management, wealth management, and broader financial services—sectors characterized by both established firms and growth potential from capital infusion and operational scaling.[S3] The preferred enterprise value range is stated between $500 million to $2 billion.[S8] This strategic focus leverages the professional backgrounds of its management team who collectively have multiple decades of experience working together in these markets,[S16] as well as their global networks facilitating access to proprietary deal flow.

Historical Financial Performance

Given its blank check status, SOCA has no operational revenues or costs driving traditional performance metrics. Its sole assets principally comprise cash equivalents stemming from IPO proceeds held in trust for intended use in a business combination transaction.[F1][S20]

The year ended December 31, 2025 shows:

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Net income was positive at roughly $2.1 million despite an operating loss of about $555 thousand,[F1] attributable largely to non-operating items such as interest income on the trust account funds less administrative expenses.[S1] The current ratio above five indicates robust near-term liquidity.[F1]

There have been no dividends distributed or share buybacks initiated since inception,[S14] consistent with standard SPAC lifecycle practice where capital preservation precludes returns until target acquisition.

Growth Prospects and Strategic Positioning

SOCA’s future value creation depends on successfully identifying a suitable target business that fits their sector focus and valuation range,[S3][S8] followed by executing an initial business combination (IBC) within the SEC-mandated timeframe (typically around two years post-IPO).[S12][S28]

Management emphasizes their capability to add value post-merger through six identified levers: applying operational expertise; recruiting senior executives; crafting equity stories; leveraging strategic relationships for growth; advising on acquisitions and financing; and marketplace intelligence delivery.[S3][S16]

The preference for developed companies with capacity for scalable growth suggests an emphasis on both steady cash flow generation potential and long-term appreciation opportunity.[S3]

However, several constraints exist:

- The reliance on public shareholder redemption rights may constrain deal negotiation leverage since large-scale redemptions reduce available deal financing.[S12][S22]

- Competition is intense from other SPACs and private equity funds targeting similar asset classes,[S28] which can inflate valuations or narrow target availability.

- Regulatory scrutiny over SPAC structures continues to evolve,[S19] increasing compliance costs.

- The company does not preclude pursuing transactions with affiliated entities but must obtain independent fairness opinions if so.[S23]

No specific targets or definitive transaction milestones have been announced publicly as of March 2026; thus investors should monitor filings closely for proxy statements or tender offer documents signaling imminent deal activity.

Forecasts, Milestones & What to Watch

SOCA must complete its IBC within the operating window specified in its articles (usually up to two years from IPO).[S12] Failure results in liquidation where shareholders receive pro rata distributions from the trust account less expenses.[S12][S24]

Key upcoming milestones include:

- Identification and announcement of a proposed initial business combination target.

- Filing proxy statement/tender offer documents providing comprehensive disclosures on the target.

- Shareholder voting events or commencement of redemption offers tied to the IBC proposal.

- Closing of the initial business combination transaction.

No explicit financial guidance exists due to the company’s blank check status; performance will ultimately hinge on post-merger integration success.

Returns & Capital Allocation

With no operational revenues or cash generation activities currently underway,[F1] SOCA’s return metrics are limited in meaning at this stage; reported net income likely reflects interest earned net of minimal costs rather than core profitability.[F1]

No dividends have been declared nor share repurchase programs initiated—standard among SPACs pending completion of their first merger.[S14]

The trust account balance as of December 31, 2025 totaled roughly $166 million (net of underwriting fees), constituting almost all current assets.[F1][S20]

Sponsor shares (Founder Shares) acquired pre-IPO carry certain voting rights but do not participate in trust account liquidation proceeds if no IBC occurs. Public shareholders enjoy share redemption rights allied with full or partial closure on deal approval votes.[S24][S25]

Potential issuance of debt or equity-linked securities may occur concurrent with business combination consummation to optimize capital structure depending on deal terms.[S14]

Risks Summary

Principal risks detailed by SOCA include:[S12][S28]

- Failure to complete an initial business combination within prescribed deadlines resulting in wind-up.

- Adverse shareholder voting dynamics exacerbated by founder voting block participation.

- Redemption rights diluting deal capital potentially limiting attractive target opportunities.

- Competitive pressure increasing cost structures for acquisitions.

- Changing legislative and regulatory landscapes heightening compliance demands.

- Potential conflicts arising if affiliated targets are pursued without independent fairness endorsement.

- Limited operating history restricting credibility versus other sponsors with track records.

Overall risk is elevated given inherent SPAC characteristics compounded by market competition dynamics prevalent post-SPAC boom years.

Conclusion

Solarius Capital Acquisition Corp., positioning itself with experienced leadership focused on high-value sectors within financial services, raised significant capital through its July 2025 listing culminating in over $166 million available for deployment after fees.[F1][S20] However, continuing absence of identifiable initial business combinations leaves it exposed to typical blank check company risks including potential shareholder disaffection related to dilution or redemption outcomes.

Critical forward-looking signals reside predominantly around announcements related to merger targets alongside associated proxy disclosures required by SEC regulations prior to transaction consummation—events that will significantly impact SOCA’s corporate trajectory post-IPO phase transitioning toward operating entity status.

Disclaimer: This report summarizes publicly available regulatory filings and company disclosures without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments