Snowflake Inc.'s Financial Growth and AI Cloud Platform Innovation in 2026

An analytical review of Snowflake's revenue expansion, platform evolution, capital moves, and regulatory landscape in fiscal year 2026.

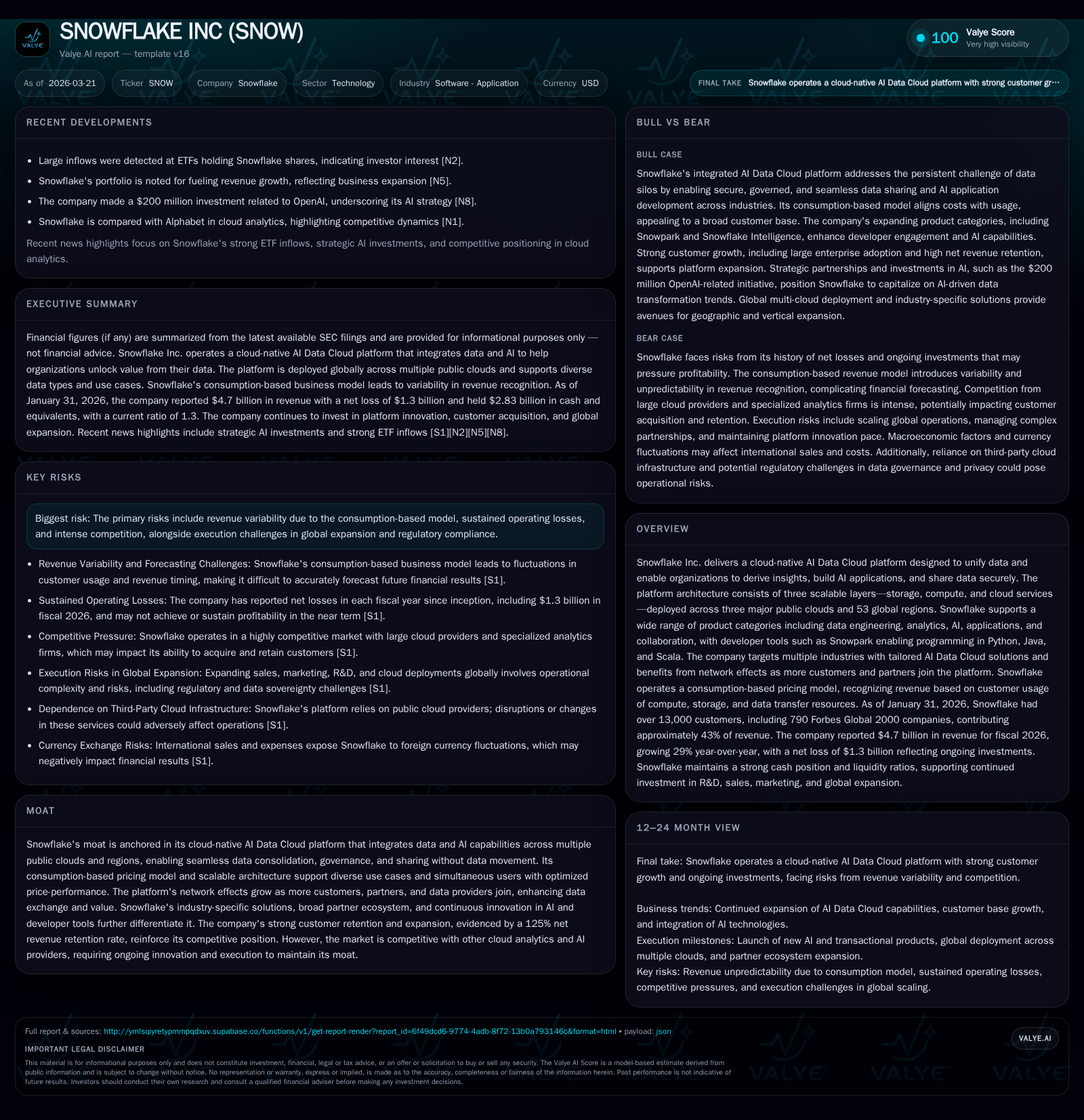

Snowflake Inc. demonstrated substantial revenue growth from $2.8 billion in FY24 to $4.7 billion in FY26, driven by its cloud-native AI Data Cloud platform combining a multi-layer scalable architecture with consumption-based pricing. The company’s innovation pipeline includes support for diverse programming languages via Snowpark and widespread deployment across 53 global regions, enhancing adoption among various industries. Despite growing operating cash flow and increased capital expenditures, Snowflake continued to incur significant net losses, highlighting a tradeoff between expansion investments and profitability. Competitive pressure from major cloud analytics players and ongoing litigation pose notable operational risks. Monitoring execution on government and regulated sector expansion alongside product rollout cadence will be critical for near-term assessment.

Historical Revenue Growth and Drivers Behind Platform Adoption

Snowflake Inc. has experienced rapid revenue acceleration over recent fiscal years, with revenues increasing from $2.8 billion in FY24 to $4.7 billion in FY26 [F1]. This growth is underpinned by broad adoption of its AI Data Cloud platform that unifies data across multiple clouds using a consumption-based business model where customers pay based on actual use of compute, storage, and data transfer resources [S5][N1]. The company benefits significantly from a net revenue retention rate exceeding 125%, indicating that existing customers are not only renewing contracts but expanding usage within the platform [S6]. Technical features that have been pivotal drivers include the multi-layer architecture—storage, compute clusters with elastic scaling capabilities, and cloud service orchestration—that supports diverse simultaneous workloads with optimized price-performance profiles [S9]. These scalable features contribute to supporting both new customer acquisitions and upselling within existing accounts.

Innovation in AI Data Cloud Offerings and Multi-Cloud Architecture

Snowflake’s continuous investment in innovation is illustrated by enhancements such as the Snowpark developer framework allowing customers to build data applications using Python, Java, or Scala [S5]. Its platform is deployed globally across three leading public clouds within 53 connected regions worldwide delivering consistent low-latency access [S12]. A key innovation differentiating Snowflake is its capability for frictionless governed data sharing without physical movement or duplication of datasets between users or clouds—this supports enterprise-grade governance while enabling real-time collaboration [S9][S12]. The integration of AI primitives natively into the platform through offerings such as Cortex AI enhances analytics processing power along with natural language querying capabilities [S11]. This seamless embedding of AI accelerates data science workflows and application development on the unified data fabric.

Emerging Growth Opportunities and Market Expansion Challenges

Looking ahead, Snowflake aims to expand penetration into heavily regulated sectors including financial services, healthcare, and the public sector which present both growth potential and complexities [S1][S6]. These sectors impose heightened compliance requirements necessitating additional internal controls and may extend sales cycles due to auditing demands [S20]. Correspondingly, these factors increase operating costs associated with regulatory certifications like FedRAMP High relevant for government contracts [S22]. Meanwhile macroeconomic uncertainty may influence client budgets causing variability in consumption patterns—clients might optimize usage thereby constraining revenue growth [S1]. Moreover, competition intensifies from legacy cloud analytics providers as well as emerging AI-focused platforms requiring ongoing innovation commitments to maintain differentiation [S18][N2]. Execution risk during global scaling persists given diverse regulatory landscapes.

Capital Allocation, Cash Flow Generation, and Shareholder Returns

In FY26, Snowflake generated positive operating cash flow totaling $1.22 billion—a strong 27% increase over the prior year—and after deducting capital expenditures of $102 million (which nearly doubled from FY25 levels), free cash flow remained robust at over $1 billion [F1][S10]. These cash generation improvements reflect operational efficiencies materializing despite continuing investments in infrastructure expansion necessary to support global deployments and advanced AI features [S26]. Share repurchases amounted to $874 million under an ongoing buyback program authorized through March 2027; however no dividends have been issued as per company policy [F1][S10]. The return on equity stands negative at approximately -69%, indicative of substantial net losses sustained during aggressive scaling phases [F1]. This capital allocation suggests a preference for investing cash in growth initiatives while using buybacks opportunistically to support stock liquidity.

Financial Performance Trends: Earnings, Cash Flow, and Profitability Metrics

The following table summarizes key financial trends for fiscal years ended January 31:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | -1332 | 1222 | -1435 | 102 | -3.6% |

| 2025 | -1286 | 960 | -1456 | 46 | -53.8% |

| 2024 | -836 | 848 | -1095 | 35 | -4.9% |

| 2023 | -797 | 546 | -842 | 25 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 874 | 1120 | -69.2 |

| 2025 | 1932 | 913 | -42.9 |

| 2024 | 592 | 813 | -16.1 |

| 2023 | 521 | -14.6 |

Source: SEC companyfacts cache [F1].

This table reveals accelerating top-line momentum while operating income remains negative albeit stabilized around -$1.4 billion due to elevated expenses largely driven by R&D and sales & marketing related to platform innovation [F1]. Notably the growing operating cash flow highlights an improving conversion efficiency despite ongoing losses.

Competitive Landscape and Snowflake’s Differentiating Moat

Snowflake competes headlined by large cloud providers including Alphabet's Google BigQuery alongside specialized analytics vendors deploying AI capabilities [S18][N2]. Its moat comprises network effects arising from the growing interconnected ecosystem facilitated by its secure data exchange capabilities allowing live data sharing across organizations without replication or complex integrations [S25][N2]. This unique ability simplifies multi-cloud operations while reducing switching costs for customers embedded deeply within Snowflake’s marketplace ecosystem featuring third-party datasets and partner solutions [S15][S16]. Consumption-based pricing further aligns incentives with customer value derived rather than fixed subscription fees but introduces revenue volatility tied to usage patterns [S5][S9]. Maintaining rapid innovation especially around AI integration remains critical against competitive pace.

Regulatory Risks and Legal Challenges Impacting Operations

The company faces several ongoing legal proceedings including securities class actions initiated in early 2024 alleging violations relating to disclosures under Sections 10(b) and 20(a) of the Exchange Act; these cases remain active with motions pending dismissal filings [S21][S13]. Additional multidistrict litigation addresses alleged security breaches exposing personally identifiable information resulting in consolidated class actions within U.S. District Courts as well as Canadian courts [S8][S21]. Furthermore, copyright infringement claims concerning unauthorized use of copyrighted works for training large language models have also been filed recently [S13]. Beyond litigation volumes themselves lies the risk associated with dealing extensively with government agencies alongside regulated commercial industries subjecting contracts to complex audit regimes increasing operational compliance burdens and potential penalties for non-compliance [S20][S22].[S4] details emergent ESG-related risks amid evolving stakeholder expectations imposing additional reporting obligations which might not fully align politically or regulatorily going forward.

Near-Term Milestones and Strategic Initiatives to Monitor

Investors should track planned rollouts of enhanced AI feature sets within the AI Data Cloud platform that drive deeper application development capabilities leveraging native model integrations reported recently [N1][N9]. Expansion progress into new jurisdictional regions especially where regulatory hurdles are pronounced warrants attention given associated higher implementation costs affecting gross margins [N9][S3]. Usage metrics including computing cycles consumed per customer alongside storage footprint expansions serve as leading indicators tied directly to revenue growth dynamics under the consumption pricing approach [N1]. Legal developments particularly outcomes stemming from securities fraud claims could materially affect governance perception affecting investor appetite [S3][S13]. Share price volatility over recent months captured by market analyst coverage underscores both momentum opportunities along with caution flags factoring SCLOUD’s cost structure vis-à-vis profit pathway execution uncertainties [N11].

Disclaimer: This report provides an analytical summary based solely on disclosed public financial filings ([F1],[S#]) and credible news sources ([N#]). It does not constitute investment advice or recommendations nor does it predict future results beyond stated facts or company disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments