Jackson Acquisition Co II's Path from IPO to Healthcare SPAC Strategy

Analyzing how Jackson Acquisition Co II is leveraging its capital raise and management expertise to target healthcare sector acquisitions.

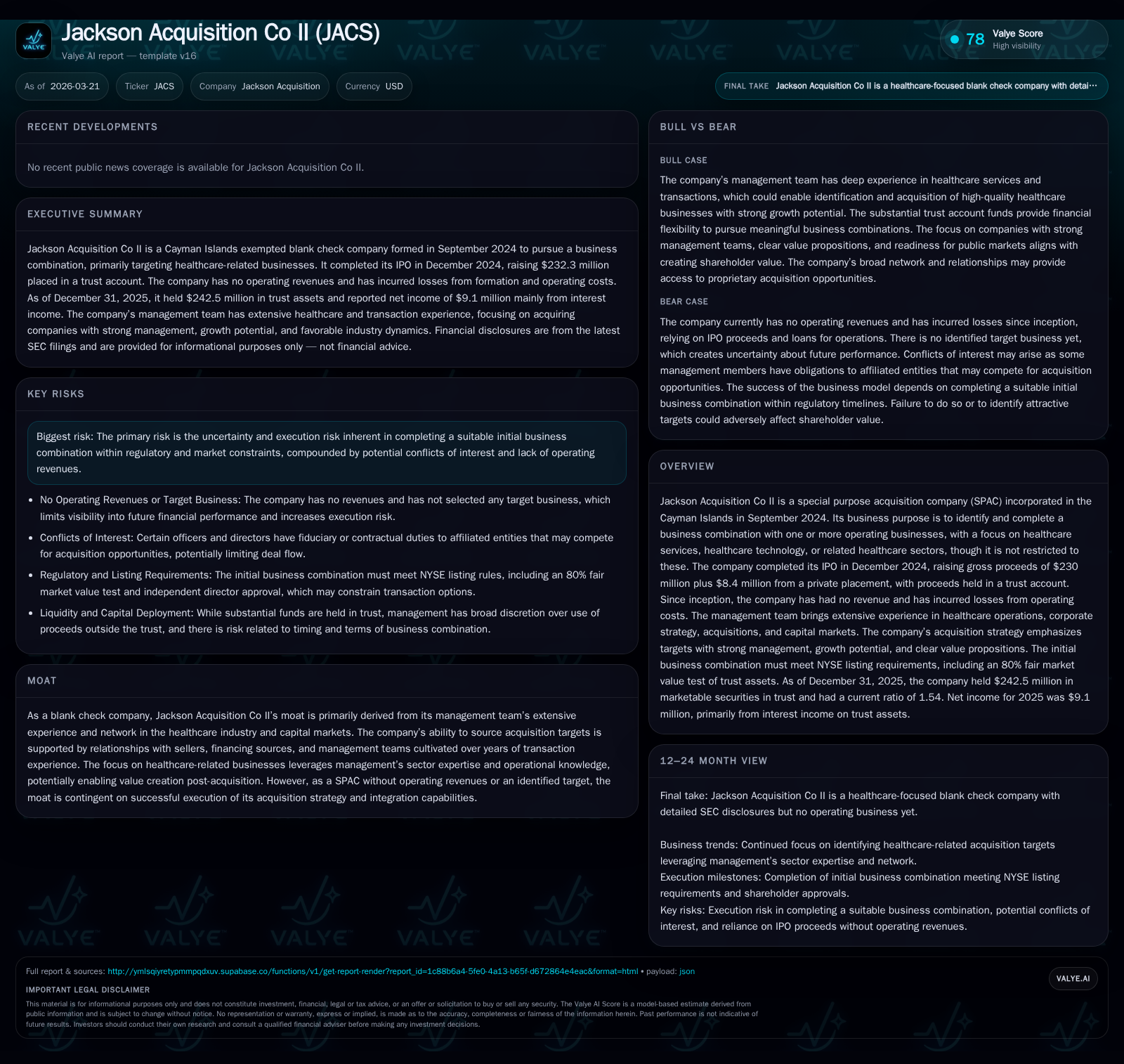

Jackson Acquisition Co II, a Cayman Islands-incorporated SPAC, raised $238.4 million in late 2024 focusing on acquiring healthcare businesses. Despite no operating revenues since inception, the company reported growing net income driven by trust account interest income, offsetting rising operating costs. The seasoned management team’s healthcare experience forms the core of the company’s moat, but successful execution of a business combination within the regulatory timeframe remains the key challenge. Investors should monitor milestone announcements and liquidity alongside evolving regulatory constraints.

Formation and Capital Raise: Building the Financial Foundation

Jackson Acquisition Co II was established as a Cayman Islands exempted company on September 11, 2024, formed to effectuate a business combination primarily focused on healthcare services or technology sectors. The company completed its initial public offering (IPO) on December 11, 2024, issuing 23 million units at $10 per unit including full exercise of underwriters’ over-allotment options. Concurrently, it completed a private placement of 840,000 units to its Sponsor and Roth Capital Partners for an additional $8.4 million [S1].

Gross proceeds from these financings totaled approximately $238.4 million, placed into a trust account managed by Continental Stock Transfer & Trust Company acting as trustee. These funds are earmarked principally for consummating a business combination and related working capital needs. Transaction expenses including underwriting fees amounted to about $5.16 million [S1].

This trust capital forms the financial foundation securing investor principal pending acquisition activity.

Tracking Financial Performance Since Inception: Income, Cash Flow, and Balance Sheet Snapshot

Since inception through fiscal year-end 2025, Jackson Acquisition Co II has had no operating revenues or substantive operations beyond preparatory IPO activities and target evaluation [S1]. Its income statement reveals losses from operating expenses offset by significant non-operating income derived from interest earned on trust-held securities.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 9 | -427590 | -569113 | +2292.0% |

| 2024 | 0 | -302833 | -177396 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 4129.4 |

| 2024 | 48.2 |

Source: SEC companyfacts cache [F1].

Operating expenses nearly tripled year-over-year reflecting increased public company compliance costs such as legal and accounting fees alongside due diligence efforts [F1][S1]. Despite an operating loss of $569k in FY2025 compared to $177k in FY2024 ([F1]), substantial interest income from money market funds—primarily invested in U.S. Treasury securities—held in the Trust Account totaled approximately $9.68 million for FY2025 ([S1],[S4]). This interest income more than offset operating costs leading to materially positive net income.

Liquidity remains robust with cash outside the Trust Account totaling approximately $522k at year-end 2025 and current assets supporting a healthy current ratio above 1.5 ([F1],[S5]).

Management Expertise and Healthcare Industry Focus: The Strategic Moat

The company's competitive advantage lies in its management team's extensive operational and transactional experience within healthcare sectors spanning acute care, post-acute services, and multi-site healthcare technology companies [S6]. Their expertise includes corporate strategy development, talent recruitment, regulatory compliance navigation, and capital markets access.

Management targets multi-site healthcare services that benefit from operational integration improvements and enhanced payor/referral networks — areas where their prior track record provides differentiated sourcing capabilities [S6].

This expertise equips Jackson Acquisition Co II not only to identify promising acquisition candidates but also to execute post-combination growth initiatives based on sector-specific value drivers.

Acquisition Criteria and Market Positioning in Healthcare Sectors

While not strictly limited to healthcare domains, Jackson Acquisition Co II prioritizes businesses within healthcare services or technology exhibiting strong growth potential backed by capable management teams [S6]. Targets sought possess defensible business models offering downside protection through predictable cash flows.

Deal structures may include cash consideration drawn from the Trust Account supplemented by issuance of shares or assumption of debt instruments [S1]. This flexibility facilitates accommodating transaction complexities encountered during negotiations.

Strategic focus on proprietary sourcing distinguishes Jackson Acquisition Co II from broader SPAC strategies reliant on commoditized deal flow.

Operational Costs and Growth Drivers – Understanding Expenses Without Revenue

Absent operating revenues until consummation of its business combination, Jackson Acquisition Co II’s cost base comprises organizational expenses including legal fees associated with SEC compliance and due diligence expenditures linked to potential transaction assessments [S1,F1].

Year-over-year increases — reflected by nearly tripled operating losses — correspond with scaling public company governance standards ([F1]). Sponsor funding has supported this burn rate without compromising timelines.

Such operational burn is typical among early-stage blank check companies where administrative overhead precedes revenue generation.

Executing the Initial Business Combination: Risks and Considerations

Execution risks center on identifying and successfully negotiating with suitable acquisition candidates within the regulatory deadline of December 11, 2026—after which failure triggers mandatory liquidation [S1,S10].

Potential conflicts inherent in SPAC sponsor arrangements combined with market volatility affecting deal pricing further complicate execution.[S10]

If no business combination occurs by deadline, dissolution will proceed despite sponsors waiving liquidating distributions related to founder shares but not public shares ([S18]). This timing constraint generates urgency while challenging negotiation credibility.

Capital Allocation Outlook: Trust Account Utilization and Shareholder Value Impact

With approximately $242.5 million held in a low-risk trust account invested chiefly in U.S. Treasury-backed money market funds as of December 31, 2025 ([S4],[F1]), Jackson Acquisition Co II safeguards principal allocated for its initial business combination.

Interest generated net of taxes may be used toward working capital or transaction-related costs; no dividends or share repurchases have been declared or executed thus far [S18,S20,F1]. The Sponsor may advance working capital loans if required pending deal closure but had none outstanding as of fiscal year-end [S15].

Capital deployment remains conservative pending target identification to preserve shareholder value pre-combination.

Key Milestones to Monitor in the Upcoming Period

While explicit guidance on forthcoming catalysts is unavailable [N/A], investors should watch for:

- Public announcements identifying definitive acquisition targets,

- SEC filings of merger agreements or proxy statements,

- Initiation of shareholder voting or redemption offer processes,

- Changes in trust account balances signaling preliminary transactions,

- Insider transactions indicating sponsor confidence levels.

These events will materially influence timing feasibility perceptions amid regulatory deadlines.

What Investors Should Watch: Liquidity, Regulatory Constraints, and Potential Targets

Investors should note liquidity backing chiefly comprises secured trust funds insulated from operational volatility but constrained by regulatory redemption rights protecting public shareholders [S5,S7,S10].

The company's emerging growth status offers some disclosure flexibilities but entails heightened vulnerability during SPAC transition phases requiring transparent governance before consummation [S7].

With no long-term debt other than modest administrative rent commitments [S5], liquidity depends heavily on sponsor support covering operating expenses ahead of deal closure [S15].

Scrutiny on potential targets’ industry positioning will intensify due to macroeconomic valuation pressures affecting healthcare M&A landscapes—Jackson’s sector expertise is critical for discerning high-value opportunities amid pricing dislocations typical since late-cycle SPAC consolidations.

This analysis is based solely on verified company filings and validated sources up to March 21, 2026. It does not constitute investment advice but aims to provide comprehensive insight into Jackson Acquisition Co II’s operational status within its sector-specific SPAC framework.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments