AudioEye Updates Preliminary Q1 2026 Results Highlighting Growth Challenges and Liquidity Constraints

AudioEye reported preliminary Q1 2026 financial estimates alongside full-year 2025 results showing ongoing net losses and liquidity pressure amid market competition.

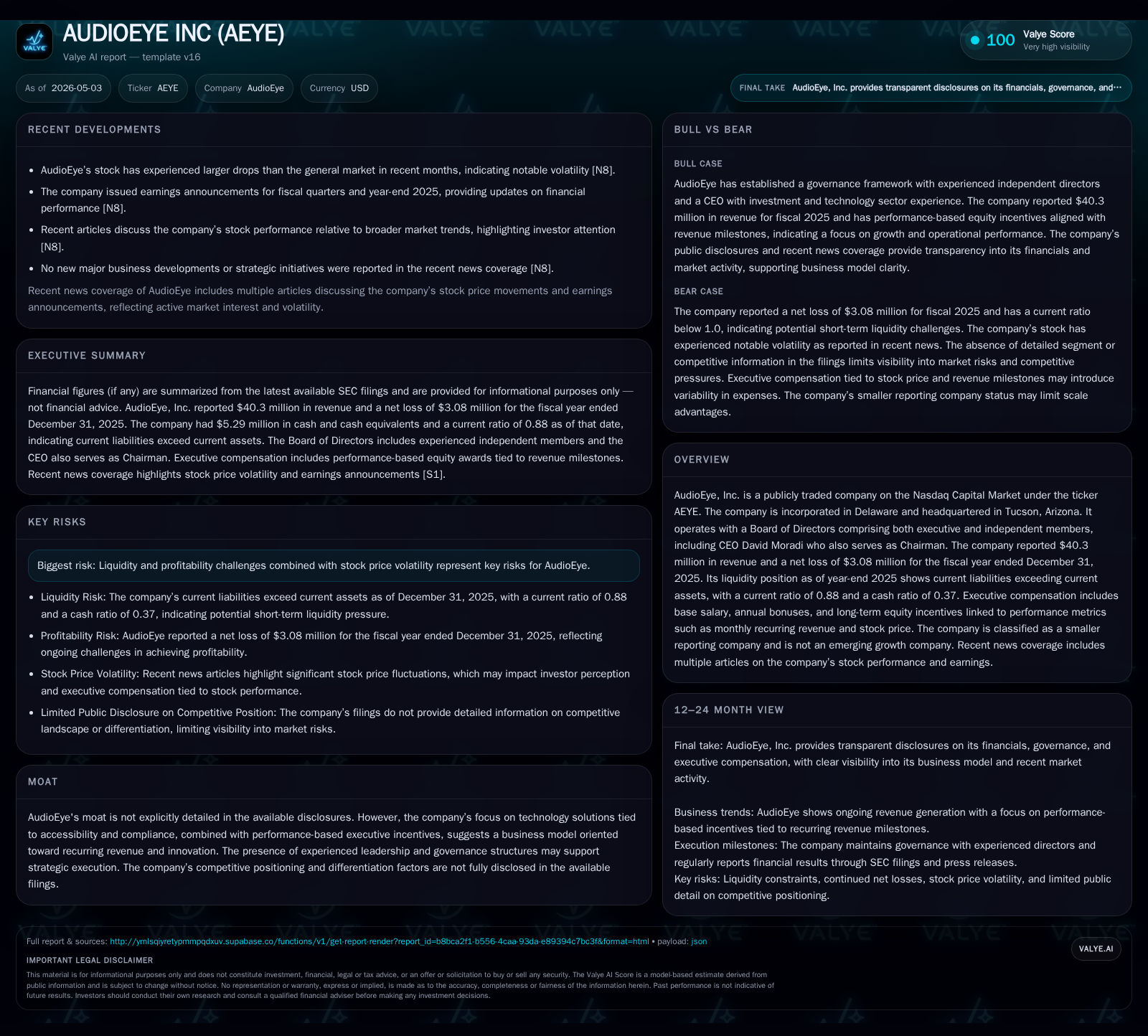

AudioEye Inc. (AEYE), a Delaware-based accessibility technology provider, disclosed preliminary unaudited Q1 2026 financial results indicating continued operational challenges. For fiscal year 2025, the company posted $40.3 million in revenue but sustained a net loss of $3.08 million, reflecting profitability pressures. The company’s liquidity remains constrained with a current ratio below 1.0 as of year-end 2025, highlighting reliance on managing working capital amidst competitive industry dynamics. Executive compensation is tied partly to monthly recurring revenue and stock performance, underscoring sensitivity to growth and share-price trajectories. Going forward, demand drivers revolve around regulatory compliance imperatives and increasing digital accessibility expectations, but risks include cash flow management, competitive pricing pressure, and customer adoption hurdles.

Recent Operating Update

AudioEye issued a press release on April 23, 2026 disclosing preliminary estimated unaudited financial results for the first quarter ended March 31, 2026 [S3]. This update serves as the latest near-term operational anchor ahead of the company's formal quarterly filings. While specific figures for Q1 were not detailed in the filing excerpt provided, this communication signals the company’s ongoing commitment to transparency in tracking its financial trajectory early in the fiscal year.

The most recent fully audited period—the fiscal year ended December 31, 2025—was disclosed in an amended Form 10-K filed April 30, 2026 [S1], providing a comprehensive view of AudioEye's financial and strategic posture. Additionally, the latest quarterly operating disclosure from November 4, 2025 outlines intermediate progress but lacks granularity beyond risk factors [S2].

Business Model

AudioEye develops and markets technology solutions focused on digital accessibility compliance. Its offerings enable organizations to meet legal requirements such as the Americans with Disabilities Act (ADA) by auditing websites, monitoring accessibility standards adherence, and offering remediation tools. This product suite is delivered predominantly through a SaaS subscription model.

Revenue stems largely from monthly recurring fees charged to customers seeking continuous accessibility oversight and compliance assurance. This structure supports predictability in revenue generation contingent on customer retention and expansion within accounts. Pricing power depends on delivering differentiated technology that reduces legal risk exposure while integrating seamlessly into client web infrastructures.

Executive compensation frameworks underscore this model’s emphasis on recurring revenue stability by incorporating metrics like Monthly Recurring Revenue (MRR) into incentive schemes [S1]. These incentives aim to align management's focus toward steady subscription growth and stock performance.

Industry Structure and Competitive Position

The digital accessibility technology space is shaped by intensifying regulatory scrutiny worldwide as governments enforce stricter compliance deadlines for online inclusivity. This regulatory push creates structural growth opportunities benefiting companies providing automated compliance tools.

However, the competitive landscape features both specialized accessibility vendors and broader SaaS incumbents expanding into compliance niches. Differentiation rests on technological sophistication—like AI-driven remediation capabilities—and seamless integration with diverse client environments.

AudioEye's governance includes experienced leadership such as CEO David Moradi who also serves as Chairman, which may enhance strategic execution against competitors [F1]. Yet the company operates with scale constraints compared to large-cap tech firms investing heavily in SaaS enterprise solutions.

Growth Drivers

Several key catalysts underpin AudioEye’s medium-term growth prospects:

- Regulatory Complexity: Accelerating government enforcement of digital accessibility standards globally compels enterprises to seek robust solutions.

- Enterprise Digital Inclusion Demand: Organizations increasingly prioritize inclusivity for reputational benefits beyond mere compliance.

- Recurring Revenue Expansion: Expanding footprint within existing customer bases via upselling additional services or increased coverage.

- Product Innovation: Enhancements in AI-based scanning and real-time remediation improve value proposition.

- Partnerships & Integrations: Collaborations embedding AudioEye technology into widely-used CMS platforms or broader compliance suites amplify distribution reach.

These drivers translate directly into measurable KPIs such as MRR growth rates, customer retention ratios, pipeline volume indicators, and product adoption metrics.

Risks / Watchpoints / Growth Constraints

AudioEye faces notable risks that could restrain growth or pressure financial stability:

- Liquidity Constraints: As of December 31, 2025, current liabilities exceed current assets yielding a current ratio of 0.88; net debt stood over $8 million [F1]. This tight liquidity posture may limit flexibility for investment or weathering downturns.

- Continued Losses: The fiscal year net loss of $3.08 million despite $40.3 million revenue evidences ongoing profitability challenges in scaling operations efficiently [F1].

- Competitive Pressure: Larger competitors with deeper pockets could exert pricing pressure or develop superior integrated offerings reducing AudioEye’s market share gains.

- Customer Adoption Risks: Market education for digital accessibility remains uneven; some enterprises may delay investments impacting revenue visibility.

- Regulatory Uncertainty: While generally favorable for demand, shifting legal landscapes can create unpredictability regarding compliance urgency or standards evolution.

Attention to these factors will be critical for assessing AudioEye’s resilience and execution capacity moving forward.

What to Watch Next

Key upcoming developments that will inform analysis of AudioEye's trajectory include:

- Detailed Q1 2026 earnings disclosure providing clarity on top-line trends, expense control efforts, cash flow dynamics, and profit/loss progression [S3].

- Progress updates on new product rollouts leveraging AI-powered automation enhancing competitive differentiation.

- Changes in customer base size or composition indicating expansion success or market penetration challenges.

- Potential adjustments in executive compensation tied to revised corporate goals reflective of evolving commercial conditions [S1].

- Monitoring competitor announcements regarding their own accessibility compliance offerings for comparative assessment.

These milestones will shine light on whether the company can shore up profitability while leveraging its growing addressable market effectively.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $5mm | |

| 2025-12-31 | ||

| Total debt | $13mm | |

| 2025-12-31 | ||

| Net debt | $8mm | |

| 2025-12-31 | ||

| Current assets | $13mm | |

| 2025-12-31 | ||

| Current liabilities | $14mm | |

| 2025-12-31 | ||

| Current ratio | 0.88x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

At fiscal year-end December 31, 2025:

The firm reported negative operating income indicative of ongoing investment phases or cost structure inefficiencies relative to scale achieved [F1].

Executive compensation is structured to incentivize growth in monthly recurring revenue alongside stock price appreciation signaling shareholder alignment intentions [S1].

Conclusion

AudioEye operates at the intersection of an expanding regulatory-driven market for digital accessibility solutions combined with SaaS subscription economics favoring recurring revenue visibility. The vital traction point will be converting regulatory tailwinds into meaningful sales growth sufficient to overcome persistent profitability deficits and limited balance sheet flexibility observed through end-2025 metrics.

Monitoring Q1 preliminary results alongside product innovation milestones will be essential in gauging whether improved execution can drive margin expansion while preserving competitive positioning amid an evolving technology landscape.

This analysis is based exclusively on publicly available SEC filings including recent quarterly reports (10-Q), annual amendments (10-K/A), event-driven reports (8-K), company press releases attached thereto, and complementary market context without any proprietary data or speculative forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments