Albany International’s 2025 Operating Loss Marks Strategic Shift Despite Solid Cash Flow and Margin Resilience

Growth pressures in aerospace composites and paper machine clothing contrast with ongoing strategic realignments and strong capital returns.

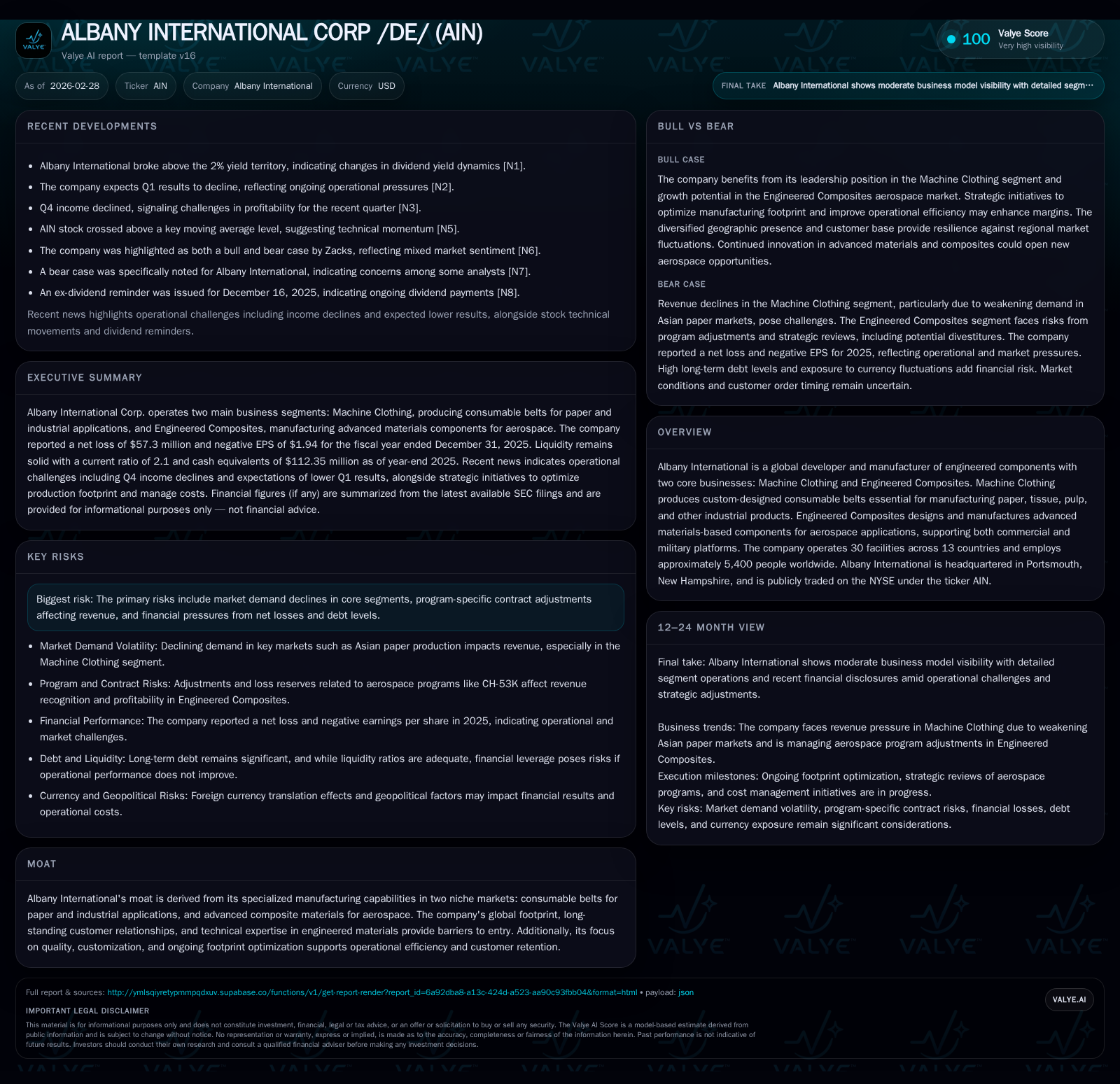

Albany International Corp. reported a net loss of $57.3 million and operating income of negative $36.1 million for fiscal year 2025, reflecting contract adjustments primarily within its Engineered Composites segment. Despite softness in the Machine Clothing business, especially in Asian markets, the company posted robust operating cash flow of $152 million and executed significant share repurchases totaling $186 million. Strategic initiatives include a review of the Structures assembly business aimed at focusing on higher-return areas. Key 2026 considerations include divestiture outcomes and aerospace program developments.

Company Overview and Market Position

Albany International Corp., headquartered in Portsmouth, New Hampshire, operates two core business segments: Machine Clothing (MC) and Engineered Composites (AEC). MC produces custom-designed consumable belts essential for manufacturing paper, tissue, pulp, and other industrial products globally, with recent demand softness notably in Asian markets. The AEC segment designs and manufactures advanced materials-based components for aerospace applications including commercial aircraft and military platforms [S1][S5].

The company’s competitive moat derives from proprietary manufacturing capabilities, a global footprint spanning 30 facilities across 13 countries, long-standing customer relationships, and technical expertise enhancing product quality and customization.

Historical Performance

Albany’s financials reveal a turning point during FY2025 marked by significant operational challenges. While revenue data beyond FY2019 are not fully available [F1], quarterly disclosures indicate volatility tied to segment-specific headwinds.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -57 | 152 | -36 | 70 | -165.4% |

| 2024 | 88 | 218 | 131 | 80 | -21.1% |

| 2023 | 111 | 148 | 168 | 84 | +16.0% |

| 2022 | 96 | 128 | 181 | 94 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 32 | 186 | 83 |

| 2024 | 32 | 14 | 138 |

| 2023 | 31 | 0 | 64 |

| 2022 | 26 | 85 | 35 |

Source: SEC companyfacts cache [F1].

Operating income fell by over 127% year-over-year to negative $36 million primarily due to pre-tax loss reserves linked to contract issues on the CH-53K military helicopter program within AEC [S29]. This followed several years of healthy profitability peaking above $180 million operating income in FY2022.

Net income reversed from positive $87.6 million in FY2024 to a loss exceeding $57 million in FY2025—a swing driven by one-time program charges coupled with softer demand dynamics affecting MC's Asia operations [S25][S28].

Despite earnings contraction, Albany maintained liquidity with cash balances near $112 million at year-end alongside over $440 million in long-term debt, yielding a current ratio around 2.1x [F1].

Segment Analysis

Machine Clothing

Revenue pressures stemmed primarily from overcapacity and declining consumption trends in Asian paper markets [S23]. Western markets remained stable with strength notably in tissue applications globally; however, these regional headwinds prompted active production footprint adjustments aimed at cost optimization.

Adjusted EBITDA margins contracted slightly but remained resilient owing to operational discipline amid volume softness [S25]. The segment continues emphasizing differentiated service models and high product quality to mitigate commoditization risks.

Engineered Composites

AEC experienced mixed results: while certain aerospace programs like LEAP engine components showed revenue growth late in the year, substantial setbacks arose from contract loss provisions on the CH-53K helicopter structures assembly [S23][S29]. These losses heavily impacted segment profitability during Q3–Q4 FY2025.

Management initiated a strategic review including potential divestiture of all or parts of the Salt Lake City production site housing this operation [S25]. Other programs under AEC continue progressing positively with innovations such as advanced fiber braiding targeting Commercial Aerospace and Defense sectors.

Outlook & Milestones

The company withdrew full-year guidance due to uncertainties around CH-53K adjustments and divestiture processes [S24][S27]. Management expressed confidence that focusing on higher-return aerospace composites opportunities alongside incremental gains within Machine Clothing will drive gradual improvement.

Key milestones to monitor include:

- Completion and timing of the Structures business review,

- Contract awards or expansions related to advanced composite technologies,

- Stabilization signals from Asian paper markets impacting MC demand,

- Capital expenditure pacing aligned with technological investments.

Capital Allocation & Returns

Albany pursued an active capital return strategy despite earnings volatility:

- Share repurchases totaled approximately $186 million in FY2025 versus under $15–85 million range historically [F1][S25].

- Dividends remained consistent near $32–33 million annually.

- Operating cash flow stood robust at $152 million supporting free cash flow around $83 million after nearly $70 million capex [F1][S15][S28].

- Capital spending was reduced modestly reflecting strategic realignment rather than expansionist posture.

Return on equity turned negative at approximately -7.9% for FY2025 following losses but had been positive during prior profitable years [F1]. Liquidity remains sufficient to support ongoing innovation investments and potential de-leveraging.

Risks & Industry Dynamics

Key risks include:

- Continued soft demand/pricing pressures in Asian paper markets affecting MC revenues,

- Contract-specific losses such as CH-53K exposing earnings volatility inherent in complex aerospace manufacturing,

- Currency fluctuations given global operations,

- Execution risks surrounding strategic divestitures impacting future financials and focus.

Industry factors involve cyclical paper consumption influenced by digital substitution trends and aerospace sector health dependent on defense budgets and commercial aviation recovery post-pandemic disruptions.

Conclusion & Monitoring Focus

Entering FY2026, Albany faces transformational challenges triggered by program-specific difficulties offset by solid operational cash flows and disciplined capital allocation.

Future success depends on effective execution of structural resets—especially within Engineered Composites—while leveraging proprietary technology advantages across both segments supported by focused R&D investments.

Investors should watch for:

- Updates on Structures business divestiture,

- Aerospace backlog developments,

- Pricing/demand trends across MC’s geographic footprint,

- Quarterly margin trends reflecting cost efficiencies amid macro uncertainties.

Albany’s navigation through these complex dynamics will shape its medium-term competitive positioning balancing growth ambitions with operational resilience.

This analysis uses publicly available information up through February 27, 2026, including SEC filings and recent news reports without extrapolating beyond provided data [F1]–[N7].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments