Ategrity Specialty Insurance: Leveraging Tech-Driven Underwriting to Capture E&S SMB Growth

ASIC’s technology-driven underwriting and broker partnerships enable scalable, consistent risk selection and profitability in the fragmented E&S SMB insurance market.

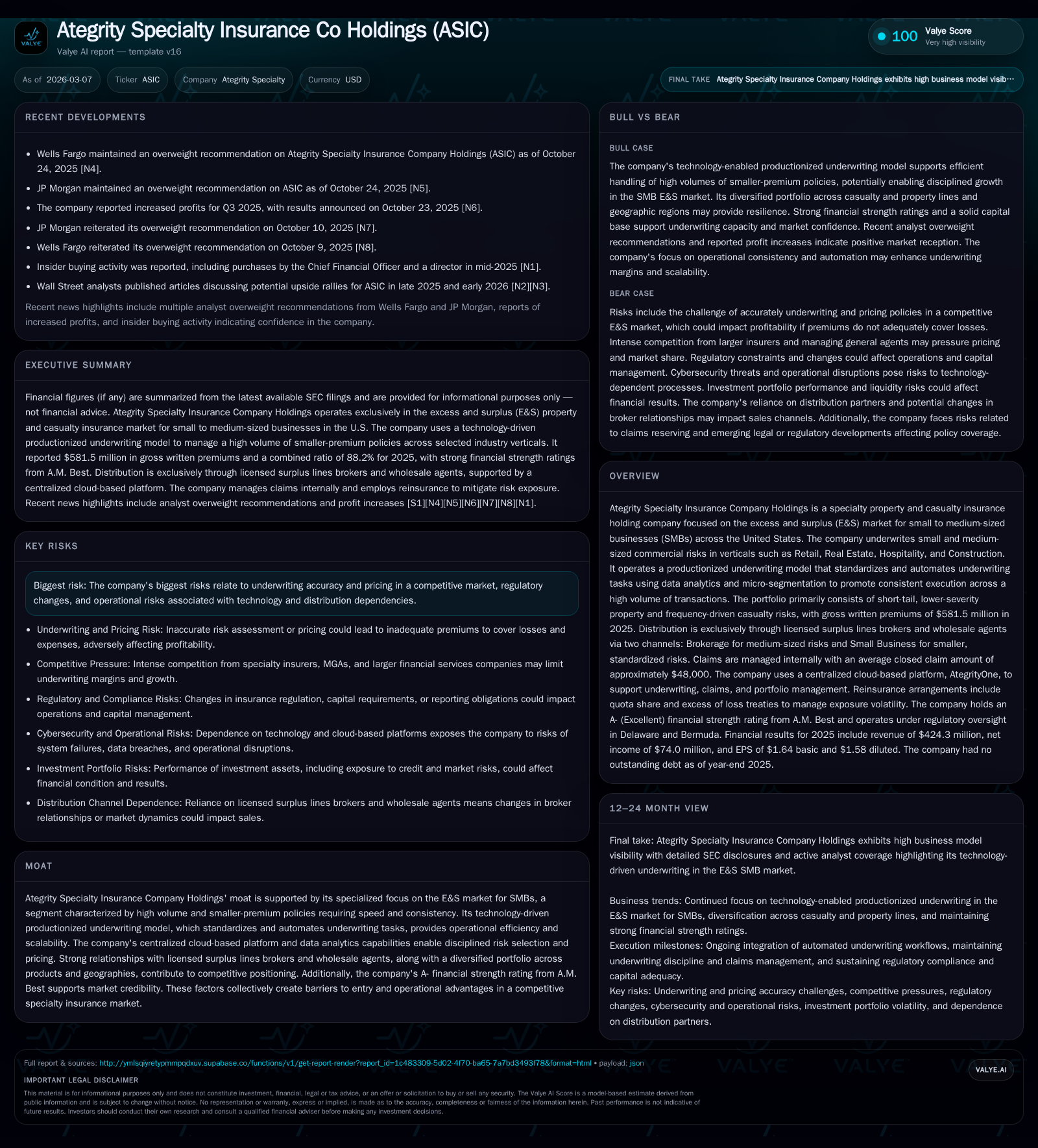

Ategrity Specialty Insurance Company Holdings (ASIC) serves the excess and surplus (E&S) insurance segment focused on small and medium-sized businesses (SMBs). Its productionized underwriting model automates and standardizes a high volume of lower-severity, short-tail property and casualty policies, enabling operational efficiency and disciplined risk pricing. In 2025, ASIC reported $581.5 million of gross written premiums with an 88.2% combined ratio, reflecting solid underwriting discipline. The firm’s competitive advantage is anchored in technology-enabled segmentation and a centralized governance framework supporting data-driven pricing, distributed exclusively through licensed surplus lines brokers. Key risks stem from regulatory changes, inflationary cost pressures, and the challenges of maintaining underwriting accuracy across numerous micro-segments.

Historical Growth Momentum: From Scale to Efficiency

Ategrity Specialty Insurance Co Holdings (ASIC) has established itself as a focused player within the excess & surplus (E&S) insurance market catering to the small-to-medium business (SMB) segment across the United States. This market niche is characterized by high policy volumes with smaller premiums, demanding efficient underwriting processes that balance speed with profitability.

Financially, ASIC reported gross written premiums of $581.5 million in 2025 [F1][S1]. The company’s revenue stood at approximately $424 million for the same period, generating a net income of $74 million [F1]. Stockholders' equity increased to about $614 million by year-end 2025, underpinning a return on equity around 12%—a respectable figure indicating effective capital use [F1]. Importantly, ASIC's combined ratio was recorded at an industry-competitive 88.2%, underscoring its capacity for disciplined underwriting practices in a segment often challenged by loss volatility [S1].

This growth reflects ASIC's ability to capitalize on its productionized underwriting framework that enables scaling while maintaining execution consistency across thousands of transactions annually. The model supports operational efficiency and promotes profitability despite the underlying smaller premium sizes typical of SMB clients.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Table: Ategrity Specialty Insurance Holdings Historical Financial Performance [F1][S1]

Productionized Underwriting: Technology as a Growth Accelerator

Central to ASIC’s moat is its differentiated productionized underwriting methodology, designed specifically for the intricacies of E&S SMB risk portfolios. The company applies micro-segmentation techniques that classify risks not only by traditional factors but also through discrete operational characteristics, geography, and exposure metrics. This granular approach allows nuanced risk selection and pricing calibrated to subtle differences in exposures [S17].

The process benefits from automation of key underwriting tasks—submission intake, classification, pricing calculation, documentation—assembled into a centralized cloud-based platform ensuring uniform application of guidelines across all underwriters [S17]. This structure reduces variance in decision-making, limits human error in high-volume flows, and fosters rapid policy issuance.

ASIC’s portfolio remains heavily weighted towards frequency-driven casualty lines (67% of GWP), which benefit most directly from reliable predictive modeling of claim frequencies rather than severity spikes. Conversely, property insurance (33%) is composed primarily of short-tail coverage for risks with limited catastrophe exposure—fitting given ASIC’s preference for stable loss profiles amenable to systematic rating techniques.

On distribution, reliance on licensed surplus lines brokers exclusively positions ASIC well within established wholesale channels valued by E&S clients seeking specialized coverage unavailable in admitted markets [S17]. The dual-channel approach bifurcates between intermediary-managed brokerage for medium-sized commercial risks versus a streamlined small business channel powered by data-driven quoting technology.

Market Environment and Future Headwinds

Despite operational strengths, ASIC confronts challenges endemic to the E&S landscape heightened by macroeconomic uncertainties. Inflationary pressures bear heavily on claims costs since underlying repair or replacement expenses reflect rising commodity prices—a factor exacerbated by recent trade tariff volatility noted in filings [S2][S19][S21]. These input cost escalations pose risks to future combined ratios if premium rates cannot be adjusted swiftly due to regulatory constraints or competitive dynamics.

Regulatory complexity compounds these difficulties; ASIC operates under multi-state supervision where surplus line eligibility criteria, premium tax regimes, and filing requirements differ materially causing administrative burdens [S6]. Regulatory developments around data privacy laws like CCPA/CPRA increase compliance costs and expose insurers to litigation risk over information security mishaps [S9][S12]. Failure to maintain strict broker compliance with surplus lines mandates could jeopardize distribution continuity.

Competition remains intense as well. Larger insurers with broader capital resources and MGAs equipped with advanced technology platforms contest aggressively for SMB segments [S26]. While ASIC leverages technology effectively today, ongoing innovation investments are critical lest it cede ground to incumbents who harness AI-enhanced analytics or faster digital onboarding capabilities.

Financial Returns and Capital Deployment Strategy

ASIC’s capitalization strategy reflects cautious stewardship aligning liquidity maintenance with measured growth funding needs. As of December 31, 2025, the company reports no outstanding debt obligations enhancing financial flexibility [S27]. Free cash flow generation was robust at approximately $140.7 million during fiscal year 2025 [F1], supporting internal funding of underwriting reserves and technology investments without reliance on external capital markets.

While ASIC does not currently pay cash dividends nor exhibit meaningful share repurchase activity per latest disclosures, a share repurchase program was authorized by the board in early 2026 offering optionality for future capital returns should conditions warrant [S8][S14]. Regulatory constraints related to statutory surplus levels govern upstreaming distributions from insurance subsidiaries ensuring solvency compliance.

The steady ROE around 12% is emblematic of balanced earnings retention combined with prudent leverage avoidance—a typical profile for specialty insurers focused on profitable underwriting rather than growth through financial engineering.

Pricing Discipline, Competitive Landscape, and Operational Risks

Pricing precision constitutes a critical vulnerability for ASIC given the fixed-premium nature of policies issued prior to full certainty regarding claim costs [S1]. Establishing adequate yet competitive rates requires extensive data collection followed by actuarial validation incorporating emerging trends in loss frequency/severity along with inflation forecasting.

Failure to accurately estimate such parameters can lead either to margin erosion when claims exceed expectations or top-line contraction if rates are set prohibitively high reducing sales volume [S1][S10]. Embedded actuarial uncertainties are heightened by potential judicial reinterpretations affecting coverage scope or endorsements nullifying anticipated exclusions [S15].

Operationally, heavy reliance on proprietary technology platforms introduces cybersecurity risks along with third-party vendor dependencies that could impair underwriting throughput or claims processing during system outages or breaches [S22][S23]. Ongoing compliance with escalating privacy regulations necessitates continuous IT investment plus heightened monitoring increasing expense ratios potentially compressing profits.

Furthermore, broker relationship continuity is pivotal; disruptions emanating from commission cost increases or consolidation among intermediaries could erode distribution effectiveness damaging revenue streams [S15][N1]. Insider buying activity noted recently signals some confidence among insiders but also underscores sensitivity around corporate developments subject to market perception shifts [N1].

Watchpoints for Investors: Drivers of Future Performance

Looking forward analytically without explicit guidance disclosed recently [N1][S3], key indicators to monitor include:

- Momentum in gross written premium growth beyond the existing scale barrier represented by $581.5 million in 2025,

- Stability or improvement in combined ratios amidst inflationary claims environments,

- Adaptive responses to evolving regulatory regimes governing pricing flexibility and data security,

- Enhancement of technological capabilities potentially incorporating AI-driven analytics boosting underwriting speed/accuracy beyond current productionized methods,

- Capital deployment choices balancing organic reinvestment against shareholder return initiatives such as buybacks.

These metrics collectively will shape ASIC’s trajectory as it matures from an emerging growth insurer into an established E&S SME market leader capable of sustainable profit delivery across economic cycles.

This report synthesized publicly filed financials and disclosures alongside firm-specific operational commentary suitable for valuation analysts focusing on E&S specialty insurance businesses without issuing investment advice or price projections.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments