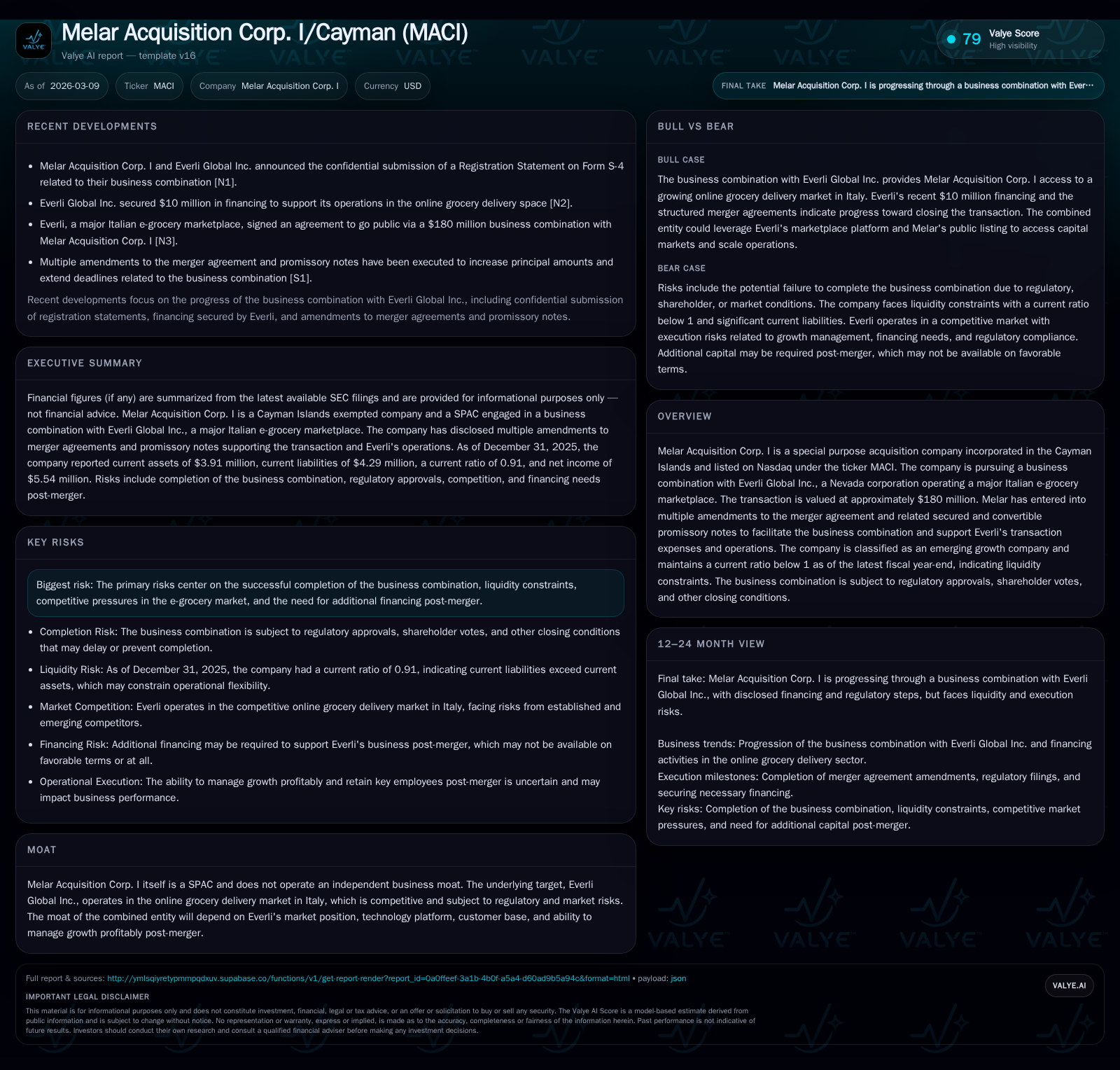

Melar Acquisition Corp. Advances Everli Merger While Managing Liquidity and Financing Risks

As a SPAC focused on merging with Italy's Everli e-grocery marketplace, Melar Acquisition Corp. faces critical execution and funding challenges.

Melar Acquisition Corp. I, a Cayman Islands-based special purpose acquisition company (SPAC) listed on Nasdaq as MACI, pursues a business combination with Everli Global Inc., a Nevada corporation operating a leading Italian online grocery platform. Having raised $160 million in its IPO, Melar has amended its merger agreement multiple times and provided secured, convertible promissory notes worth several million dollars to support Everli's transaction costs and operations pre-close. The company reports a sub-1 current ratio indicating liquidity constraints and negative operating cash flow alongside worsening operating losses, though net income improved year-over-year due to non-operating items. Completion of the merger hinges on regulatory approvals and shareholder votes; post-merger growth depends largely on Everli's market position in a competitive European e-grocery sector but may be capped by financing needs and execution risks.

Company Overview

Melar Acquisition Corp. I (Nasdaq: MACI) is a Cayman Islands exempted company structured as a special purpose acquisition company (SPAC). Its primary mission is effecting an initial business combination with one or more entities within a prescribed timeframe—24 months from its June 20, 2024 IPO closing, setting a hard deadline of June 20, 2026 for deal consummation [S1]. To date, Melar has no independent operating revenues or business activities beyond organizational and IPO-related tasks.

Historical Performance & Financial Position

Melar’s historical financial results reflect its nature as a blank-check vehicle: no operating revenues but operational costs incurred during search and negotiation phases create recurring operating losses. According to its latest annual report ending December 31, 2025 [F1]:

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 6 | -774258 | -1475992 | +31.6% |

| 2024 | 4 | -545234 | -367764 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -79.3 |

| 2024 | -76.2 |

Source: SEC companyfacts cache [F1].

Year-over-year deterioration in operating income (-301%) signals higher operational costs mainly from merger-related activity [F1]. Operating cash flow also worsened by approximately 42%, underscoring ongoing cash burn while pursuing the combination [F1]. The positive net income reported largely reflects one-time financial gains outside core operations rather than sustainable profit generation.

The current ratio below unity highlights liquidity constraints; current liabilities surpass current assets by roughly $386K at fiscal year-end [F1]. Moreover, net equity remains deeply negative at nearly -$7 million owing to accumulated losses and share-based obligations [F1]. This underscores the limited standalone financial buffer prior to completion of the business combination.

Business Combination Target & Industry Context

Melar’s announced target is Everli Global Inc., incorporated in Nevada but operationally centered on Italy’s e-grocery marketplace sector [S1]. The proposed business combination values Everli at approximately $180 million [S1], blending Melar’s trust-held IPO proceeds with additional promissory notes extended for transaction facilitation.

Everli operates as one of Italy’s leading online grocery delivery platforms—a sector marked by rapid consumer adoption but intense competition from global players and local supermarkets expanding digital services. Regulatory uncertainties around logistics and food safety add complexity [S1]. Post-merger success depends on integrating proprietary technology enabling efficient order fulfillment while scaling profitably within challenging unit economics common in last-mile delivery markets.

Capital Structure & Financing Amendments

To provide liquidity for Everli’s transactional and operational needs before closing, Melar entered into multiple secured promissory notes totaling up to $3.25 million as of late September 2025—an increase from an original $300K note issued May 30, 2025 [S5][S6][S7][S14]. These notes carry annual compounding interest rates of 17.5% alongside pledge agreements securing Everli equity stakes as collateral [S5][S16]. Additional convertible notes of $7.5 million with similar interest terms were also issued through affiliate entities tied to Melar’s sponsor group [S14][S26].

These amendments reflect incremental funding support for Everli ahead of closing alongside management's cautious risk mitigation given potential deal uncertainties.

Merger Process Milestones & Conditions

The Agreement and Plan of Merger was signed July 30, 2025 between Melar Acquisition Corp., its wholly owned subsidiary MAC I Merger Sub Inc., Everli Global Inc., Sponsor entities representing shareholders post-closing, and key equity holders including Escrowed Sellers [S13][S18].

Critical conditions include:

- Receipt of required regulatory approvals in Italy and U.S.

- Approval by Melar shareholders voting on proxy statements filed alongside Form S-4 registration statements after SEC review [S26].

- Completion deadline before Combination Period expiration on June 20, 2026 or liquidation/redemption procedures activate per trust account rules [S1].

- Procurement of at least $10 million in Bridge Financing by Everli prior to closing or risk termination per amended Merger Agreement extensions granted through October 21, 2025 [S14][S27].

Failure in any condition could delay or nullify the transaction triggering SPAC wind-down obligations.

Growth Prospects & Constraints Post-Merger

If completed successfully with Everli—a major player in Italy’s growing e-grocery domain—the combined entity faces both growth drivers such as expanding online grocery penetration accelerated by consumer shifts and operational leverage via proprietary technology; alongside constraints including intense competition from entrenched retailers launching digital initiatives and regulatory scrutiny potentially raising compliance costs.

Capital strategy post-close will be pivotal given likely additional financing rounds or strategic partnerships needed for expansion.

Capital Allocation & Shareholder Returns

As typical for SPACs prior to initial business combination completion:

- No dividends or share repurchases have been reported through early 2026 filings [S9][S10][S11][S12][F1].

- Capital outlays focus primarily on administrative costs related to searching for targets and fulfilling merger conditions including legal fees.

- The trust account established at IPO holds $160 million earmarked until deployment into the business combination or returned upon liquidation scenarios [S1].

- Sponsor-affiliated lenders hold promissory note instruments with conversion rights offering potential equity upside aligned with closing success [S14][S26].

ROE metrics are not meaningful given negative equity coupled with positive net income reflecting accounting nuances rather than operational profitability at this stage [F1]. Monitoring post-combination earnings quality will be critical for evaluating future capital deployment effectiveness.

Risks Summary

Material risks include:

- Failure to consummate within statutory time limits triggers SPAC dissolution exposing investors only to pro rata redemption values protected in Trust Accounts minus expenses [S1].

- Liquidity constraints evidenced by current ratio below unity restrict ability to self-fund mergers or absorb unexpected hurdles without costly external financing.

- Market skepticism around SPACs narrows viable acquisition targets causing bidding competition inflating deal pricing beyond intrinsic value limits.

- Post-merger challenges tied specifically to Everli’s European e-grocery market dynamics such as price competition paired with complex supply chain considerations constraining margin improvements.

- Evolving regulatory landscapes in U.S./Italy impacting cross-border governance post-close.

What To Watch Next (Analysis)

Investors should monitor:

- SEC clearance progress for registration statements enabling shareholder votes on the Business Combination.

- Final regulatory clearances from Italian authorities regarding food handling licenses or anti-trust reviews.

- Updates on bridge financing completion status including any alternative financing or increased sponsor exposure via convertible debt extensions.

- Shareholder voting outcomes determining approval despite founders’ voting power potentially diluting public consensus impacts stated earlier risks.

- Post-close metrics focusing on Everli’s growth trajectories such as user acquisition trends versus churn rates indicative of platform stickiness amid competition.

Conclusion

Melar Acquisition Corp sits at a critical juncture transitioning from blank check shell into an operational enterprise leveraging Italy’s burgeoning e-grocery market via Everli Global Inc. Proceeds from its successful IPO underpin transaction funding capability; however persistent liquidity challenges require ongoing secured note injections reflecting elevated credit risk premiums compounded by amendments easing deal conditions.

Execution hinges not only on investor approvals but also navigating complex cross-border operational hurdles inherent in last-mile fresh food delivery segments marked by thin margins and aggressive rivalry among established multi-national competitors pushing rapid innovation cycles.

Stakeholders should treat Melar as highly speculative pending transparent reporting on merger closure timelines plus demonstrable improvements in post-merger integration performance substantiating expected market share gains without disproportionate capital erosion.

This analysis abstains from investment recommendations or price forecasts. It synthesizes publicly available documentation up through March 9, 2026 without speculative extrapolations beyond authenticated data sources cited herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments