INLIF Ltd’s Strategic Growth and Capital Dynamics in Injection Molding Automation

INLIF Ltd combines specialized injection molding automation with new energy sector exposure, navigating early-stage public market challenges and tax uncertainties.

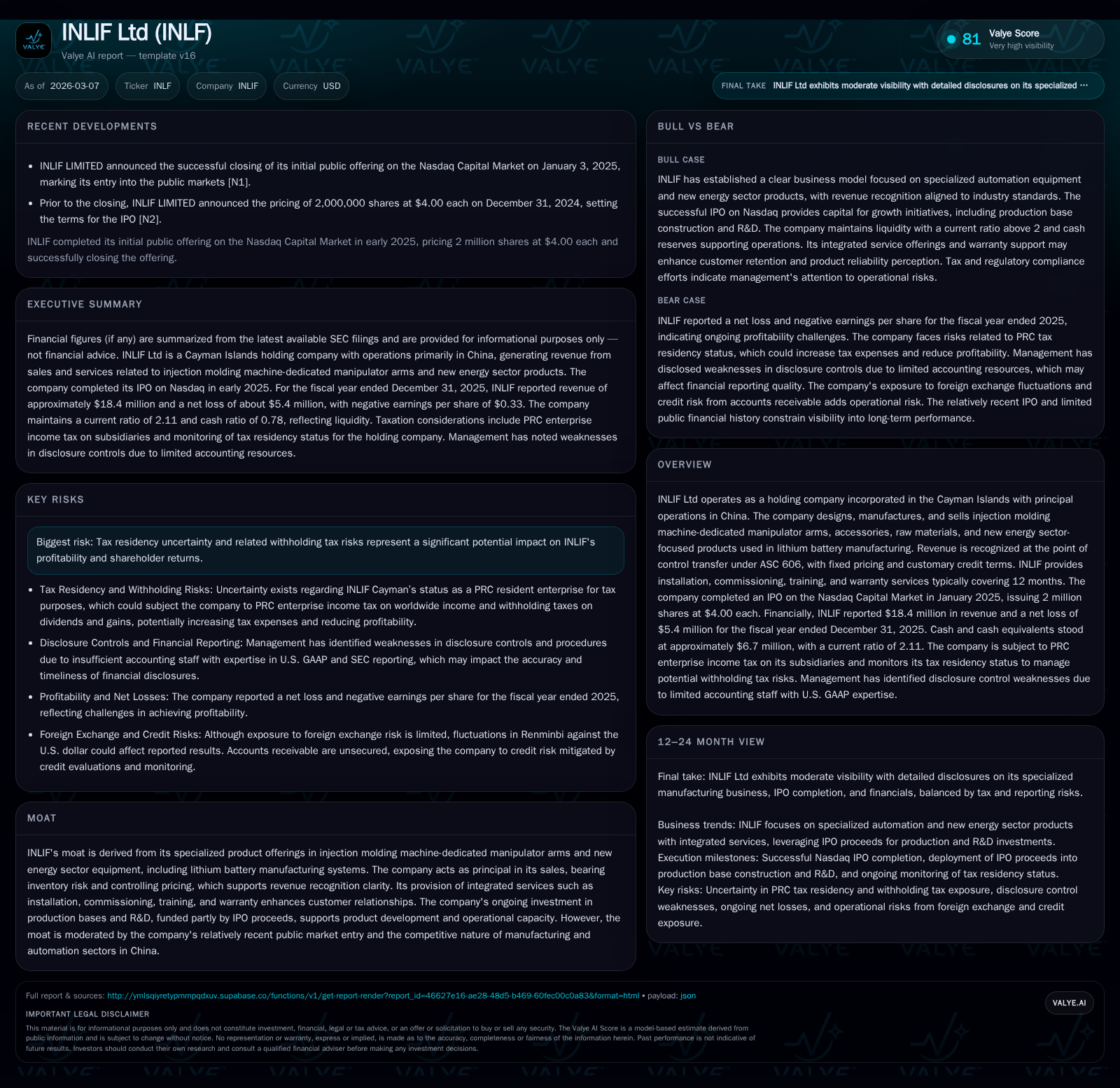

INLIF Ltd, a Cayman Islands holding company with operations centralized in China, focuses on developing and supplying dedicated manipulator arms for injection molding machines alongside lithium battery manufacturing equipment. Following a Nasdaq IPO in early 2025, the company posted revenue growth of 16.5% in FY2025 but experienced steep losses driven by expanded operating costs and investment activities. INLIF is deploying IPO proceeds towards expanding its production capacity and R&D, yet faces significant risks from potential PRC tax residency reclassification impacting shareholder returns. Going forward, the company’s ability to leverage new energy demand and improve operational efficiency will be key factors for sustaining growth and managing financial health.

From Startup to Nasdaq: Growth Momentum Behind INLIF’s Specialized Manufacturing

INLIF Ltd operates as a Cayman Islands-incorporated holding company with principal operations headquartered in China. Its core product suite centers on injection molding machine-dedicated manipulator arms—essential automation components that aid precision and efficiency within plastic manufacturing lines—and products tailored for the burgeoning new energy sector, notably lithium battery manufacturing equipment [S1]. These technologies collectively form a niche moat anchored on product specialization paired with integrated customer service offerings such as installation, training, and warranty support.

The company marked a significant milestone with its January 2025 IPO on the Nasdaq Capital Market, raising gross proceeds of approximately $8 million through the issuance of two million shares at $4 each, netting $7.4 million after underwriting discounts and expenses [S10][S20]. This capital infusion positioned INLIF for a scale-up phase aimed at expanding production infrastructure and augmenting research capabilities.

Reflecting early traction in market adoption, INLIF grew revenue by 16.5% to $18.4 million for fiscal year 2025 compared to $15.8 million in 2024 [F1]. This momentum underscores increasing customer acceptance within injection molding automation and emerging new energy applications.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 18 | -5 | -1890612 | -6 | +16.5% | -439.0% |

| 2024 | 16 | 2 | 1579382 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -2 | -33.8 |

| 2024 | 2 | 15.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue growth measured year-over-year; net income % change signals deepening losses.

Decoding INLIF’s Revenue Drivers and Operating Shifts Over 2024-2025

Detailed disclosures reveal that INLIF acts predominantly as principal in its contracts, thereby bearing inventory risk and setting fixed prices under ASC 606 revenue recognition rules [S13]. The company delivers not only equipment—manipulator arms and their accessories—but also associated installation, commissioning, training, and warranty services typically covering twelve months post-acceptance [S6][S8].

Despite achieving higher top-line revenue growth (+16.5%), operating income declined by over 550% year-over-year to nearly negative $5.8 million in FY2025 [F1]. The cause lies primarily in scaling inefficiency amid investment-related operating cost increases coupled with pressure on unit economics—the hallmark challenge when accelerating production base expansion under capacity constraints typical within Chinese automation hardware sectors.

Manoeuvring through these operational shifts exposes INLIF’s limited operating leverage so far; while fixed cost absorption remains inadequate given sales volume thresholds needed for profitability gains [S16][S21]. The complex pricing dynamics around customized manipulator arms versus standardized accessory sales also factor into margin contraction trends.

Operational Challenges Reflected in Deepening Losses and Cash Flow Trends

The financial trajectory portrays intensifying net losses—widening from a positive net income of roughly $1.6 million in FY2024 to a significant loss of $5.4 million in FY2025 (a swing exceeding -439%)—highlighting early public-stage cash burn attributable to rapid scale-up initiatives [F1]. This loss translates into an approximate -33.8% return on equity based on closing equity levels near $16.1 million [F1], underscoring current capital deployment strain.

Operating cash flow flipped from positive inflows of about $1.6 million to negative outflows exceeding $1.8 million (YoY decline near -220%), signaling operational cash consumption outpacing revenue-generated earnings before accounting for investment outlays [F1]. Capital expenditures surged over sixfold from roughly $26 thousand to $193 thousand—a clear indicator of infrastructure buildup including the announced construction of a digital intelligent equipment production base and an R&D center targeting automation technologies [S21]. The augmented fixed costs inherent to asset-led growth affect near-term free cash flow negatively.

This pattern typifies many emerging Chinese manufacturers transitioning from private startup phases into publicly accountable entities confronting transparency demands while investing heavily in long-cycle automation assets.

Strategic Capital Allocation: IPO Proceeds, R&D Investment, and Liquidity Position

INLIF’s strategic use of proceeds from its latest public offering involved directed deployment toward capital projects essential for long-term competitiveness: construction of a 5G digital intelligent equipment production facility accounting for approximately $696K spent as part of IPO allocation plans; an industrial robot R&D center; plus substantive material purchasing alongside personnel costs related to innovation efforts [S20][S21]. Through March 31, 2026, about half the net IPO funds were utilized confirming ongoing commitment to foundational growth investments.

Capital stewardship reflects a stable liquidity posture with cash equivalents standing at roughly $6.7 million amid current assets totaling about $18.2 million versus current liabilities near $8.6 million—delivering an adequate current ratio of approximately 2.11 that supports short-term obligation coverage without immediate distress signals [F1][S19].

While no dividend distributions or share repurchases have been reported following IPO—as expected given ongoing reinvestment needs—the company's successful completion of a sizeable PIPE financing round worth over $32 million further bolsters its capital structure breadth beyond initial equity issuance during early 2026 [S3], enhancing runway for innovation-led expansion.

Tax Residency Risks: The Potential Impact on Profitability and Investor Returns

One salient nondilutive challenge facing INLIF involves uncertainties tied to its tax residency status under PRC law due primarily to the Classification as a "resident enterprise" if deemed managed or operated substantially within mainland China despite Cayman incorporation [S1][S14]. This classification carries substantial consequences including exposure to full PRC enterprise income tax rates (25%) on worldwide income plus mandatory withholding tax on dividends remitted to foreign shareholders at rates generally set at 10%, potentially elevating up to 20% depending on treaty applicability.

Moreover, realized gains upon sale of shares by non-resident investors could similarly attract withholding levies if income sourced from within PRC jurisdiction is confirmed by authorities under ambiguous regulations regarding offshore companies controlled via de facto management bodies located inside China [S14].

This risk compounds ambiguities related to U.S.-specific PFIC status impacting U.S.-based holders—factors that could curtail net investor returns even if fundamental business progress remains unhampered.

Growth Horizons: Leveraging New Energy Equipment Demand versus Market Constraints

INLIF’s future growth vectors appear linked closely to sustained demand escalation within the new energy sector—primarily lithium battery manufacturing systems where evolving global electrification mandates favor advanced automated production solutions integrated via precision manipulators designed specifically for this application segment [S1][S8].

However, market penetration beyond existing Chinese customers hinges on overcoming entrenched competition among domestic manufacturers specializing in plastic injection molding automation plus navigating regulatory nuances impacting industrial exports.

Additionally, product differentiation through continuous R&D innovation funded partly by recent capital raises is imperative; any price sensitivity arising from macroeconomic or supply chain shocks could tighten operating margins further despite escalating unit volumes.

Watchpoints Ahead: Monitoring Operational Efficiency, Competitive Pressures, and Shareholder Value

Key operational metrics merit close observation going forward: improvement in unit economics reflecting scaling benefits; margin expansion driven by optimized pricing discipline oriented around value-added features of customized manipulator arms; rationalization of warranty provisions versus actual service claims; prudent credit risk management amid extended payment terms typical within this sector; all collectively forecasting whether positive operating leverage materializes or further dilution transpires due to fixed cost burdens [S13][S21].

Competitive landscape analysis should track rival integration efforts blending robotics with injection molding machinery amid China’s vigorous automation ecosystem growth supported by state policy incentives.

Shareholder value creation efforts post-IPO remain nascent with no dividends or buybacks declared so far but PIPE funding enhances both solvency cushion and capacity for discretionary financial maneuvers subject to evolving business results and governance resolutions passed during the January 2026 extraordinary general meeting involving share capital adjustments [S15][S18].

Bridging Innovation with Financial Health — An Investor’s Analytical Lens

In essence, INLIF Ltd stands at a critical inflection point balancing its technical moat rooted in niche manufacturing automation against marked financial headwinds characteristic of emerging-market public companies investing heavily toward scale-up stages supported by injection molding manipulator arm specialization synergized with new energy sector pursuits.

While the robust revenue ramp evidences growing market validation supported by comprehensive service packages reinforcing client engagement, operating losses alongside negative cash flow spotlight typical early-stage inefficiencies compounded further by aviation tax residency uncertainties complicating shareholder return profiles.

Careful tracking of execution success regarding operational leverage improvement combined with mitigating withholding tax impact will remain paramount going forward to bridge innovation promise into sustainable financial performance aligned with prudent capital stewardship exhibited thus far.

This report is prepared solely as informational content without any form of investment recommendation or advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments