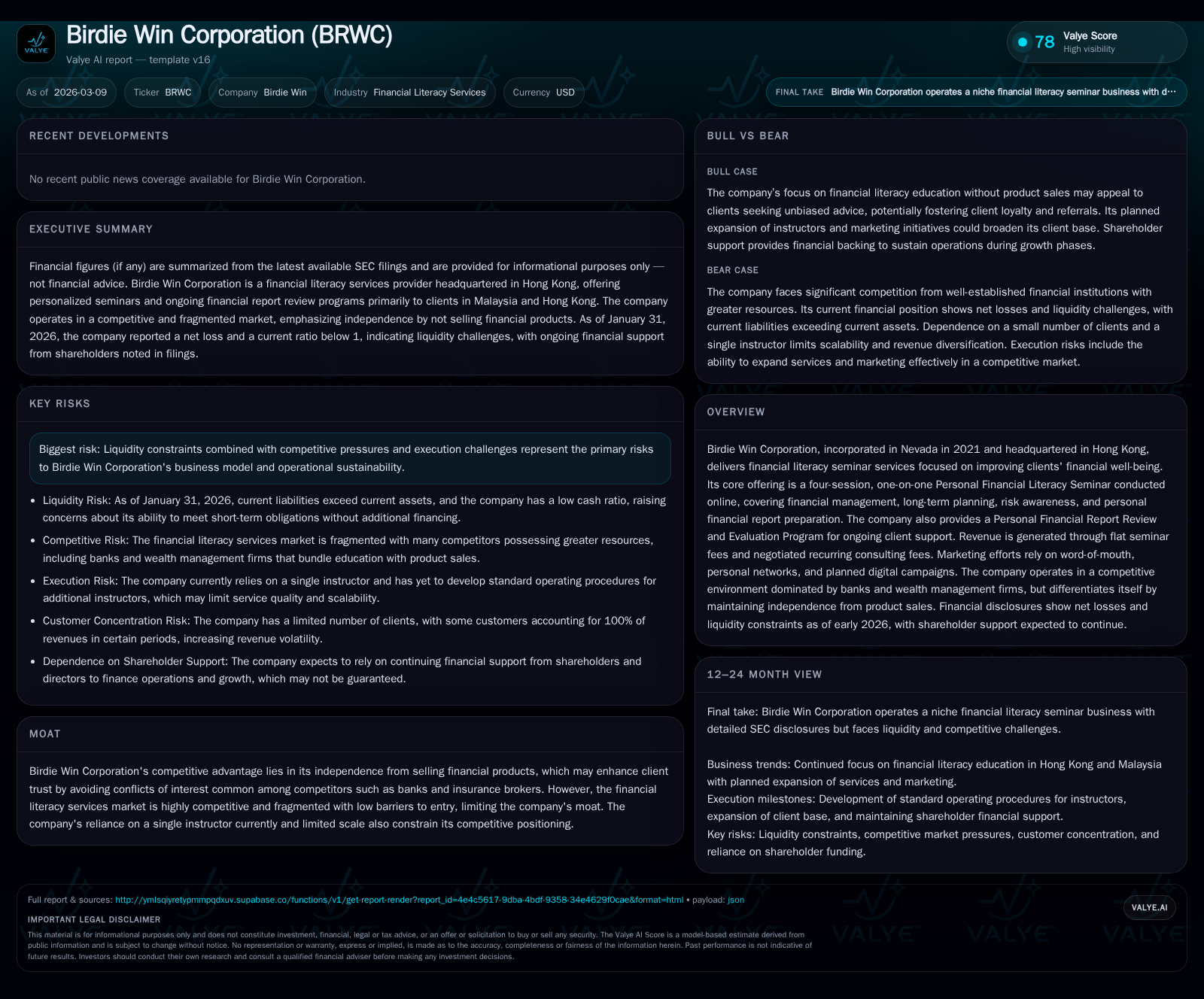

Birdie Win Corp Battles Losses and Tight Liquidity While Shaping Financial Literacy Services

Birdie Win Corporation is refining its independent financial literacy model amid persistent operating losses and constrained liquidity, navigating a competitive advisory market landscape.

Birdie Win Corp, established in 2021, provides personalized financial literacy seminars focusing on client education without selling financial products, aiming to build trust in a fragmented market. The company has consistently reported operating losses due to limited scale and reliance on a single instructor, with a modest improvement in cash flow signaling initial operational leverage. Liquidity remains strained as current liabilities outstrip current assets, underscoring the necessity of shareholder support for ongoing operations. Future growth hinges on expanding client acquisition beyond word-of-mouth and scaling service delivery, but execution risks related to competitive pressures and governance transitions loom large.

Historical Financial Performance and Drivers of Growth

Birdie Win Corporation's financial performance since its inception has been characterized by consistent operating losses stemming largely from limited scale and concentrated operational capacity on a single instructor model. Their annual reported operating income declined from a loss of approximately $26,050 in FY2022 to an improved loss of $17,299 in FY2025—a 28.2% year-over-year improvement evidencing gradual progress [F1]. Net income followed a parallel trajectory with losses narrowing similarly.

Operating cash flows indicate nascent operational leverage; FY2025 yielded a small positive cash inflow of $326 compared with substantial negative flows in prior years (-$3,155 in FY2024) [F1]. Capital expenditures remain minimal and steady at around $1,304 primarily reflecting intangible investments relevant to their digital seminar delivery rather than tangible assets.

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -17299 | 326 | -17299 | +28.2% | |

| 2024 | -24082 | -3155 | -24082 | -205.1% | |

| 2023 | -7893 | -19312 | -9981 | 1304 | +69.0% |

| 2022 | -25494 | -35203 | -26050 | 1304 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -120.4 | |

| 2024 | 8135.8 | |

| 2023 | -20616 | -136.4 |

| 2022 | -36507 | -186.4 |

Source: SEC companyfacts cache [F1].

The company's revenue is generated through online personal financial literacy seminars and consulting fees. The modest revenue base combined with high fixed overhead contributes to sustained losses despite incremental gains.

Examining Operating Loss Trends and Cash Flow Improvements

Birdie Win's ability to reduce operating loss by over a quarter from FY2024 to FY2025 signals beneficial cost controls or improved customer acquisition efficiencies [F1]. Notably, it achieved positive operating cash flow for the first time in FY2025—a key factor demonstrating emerging operational sustainability potential despite continued negative net income.

This improvement may stem from stabilization in marketing spend after initial ramp-up phases and optimization of seminar delivery processes. The company's financial literacy services command flat fees per seminar series which allows for some revenue predictability once client acquisition ramps. Nonetheless, gross margins are pressured by narrow course offerings and reliance on founder-level expertise.

Customer Base Dynamics and Geographic Segmentation

Birdie Win operates solely within the financial literacy service sector targeting individuals mainly across Hong Kong and Malaysia [S3][S4][S6][S8]. Segment reporting confirms a single business unit—financial services—with geographic revenues entirely sourced from these two markets.

Customer concentration is pronounced: during recent periods one or two clients accounted for all revenues. For example, in the six months ended January 31, 2026, two customers accounted for 100% of revenues [S6][S17]. This concentration elevates revenue volatility risk given dependency on few accounts.

While this concentration might reflect early-stage operations or bespoke service characteristics requiring tailored delivery models, it leaves Birdie Win vulnerable if these key relationships do not extend or expand.

Liquidity Status and Capital Structure Challenges

Liquidity constraints are central challenges for Birdie Win. As of January 31, 2026, current assets stood at $16,046 against current liabilities totaling $18,200 producing a current ratio of approximately 0.88—below typical thresholds considered comfortable for operational liquidity [F1]. Cash balances are critically low near $722 at period end.

The company acknowledges ongoing reliance on shareholder financial support to fund operations beyond organic cash generation [S7][S12][S18]. Without fresh equity infusions or debt financing under sustainable terms, working capital shortages could disrupt service delivery or limit growth investments.

Future Growth Opportunities Within Financial Literacy Services

Birdie Win differentiates itself strategically by maintaining advisory independence from financial product sales — a touted moat that enhances client trust by mitigating conflicts found commonly among banks or wealth managers .

Planned digital campaigns aim to amplify customer acquisition beyond traditional word-of-mouth referrals . However, scalability depends critically on increasing instructor headcount or leveraging technology platforms efficiently given current bottlenecks.

Expanded recurring consulting contracts represent another growth vector alongside potential development of complementary products emphasizing personal financial planning continuity.

Risks Surrounding Market Competition and Execution

The financial literacy market remains highly fragmented with low barriers to entry allowing competitors ranging from established banks to boutique advisors [S1]. Birdie Win’s limited scale compounded with founder-dependent instruction creates execution risks including service disruption potential tied to leadership turnover observed since mid-2023 [S1].

Competitive disadvantages include smaller marketing budget footprints relative to incumbents who bundle literacy with product sales offering seamless wealth solutions.

Moreover, tight liquidity poses existential risk should operational ramp-up timelines stretch without adequate funding.

Capital Allocation Decisions: Dividends, Buybacks, and Retained Earnings

Due to persistent net losses totaling nearly $17K annually most recently and negligible free cash flow after accounting for capex (-$978) [F1], Birdie Win has no scope for dividends or share repurchases. Return on equity remains deeply negative near -120%, reflecting sustained capital erosion rather than profit generation [F1].

Equity levels show fluctuation indicative of recapitalization efforts possibly linked with issuance for services rendered as new directors were compensated common stock totaling $24K for consultancy arrangements initiated in early 2025 [S14][S18].

Absent meaningful profits or positive free cash flow generation trajectories capital allocation emphasis will remain firmly anchored on balance sheet preservation via fresh equity injections or shareholder advances.

Key Milestones to Monitor in Birdie Win's Operational Trajectory

Critical indicators will include diversification of the customer base away from concentrated individual clients towards broader clientele segments enhancing predictable revenue streams. Scaling capacity through hiring additional certified instructors or digitizing content can resolve narrow delivery constraints.

Liquidity improvement metrics such as raising working capital above current liabilities will signal financial stability progress critical before substantive marketing expansion deployment.

Monitoring any further leadership changes post-January 2026 will illuminate governance consistency impacting investor confidence and execution reliability.

Management guidance remains absent; thus close attention must be paid to quarterly filings for updates on these fronts alongside observable uptake in marketing initiatives effectiveness.

This analysis relies strictly on company-reported data as filed with the Securities Exchange Commission up through March 9th, 2026 [F1][S#] and incorporates qualitative excerpts from proprietary research materials. No forward-looking investment advice is offered or implied.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments