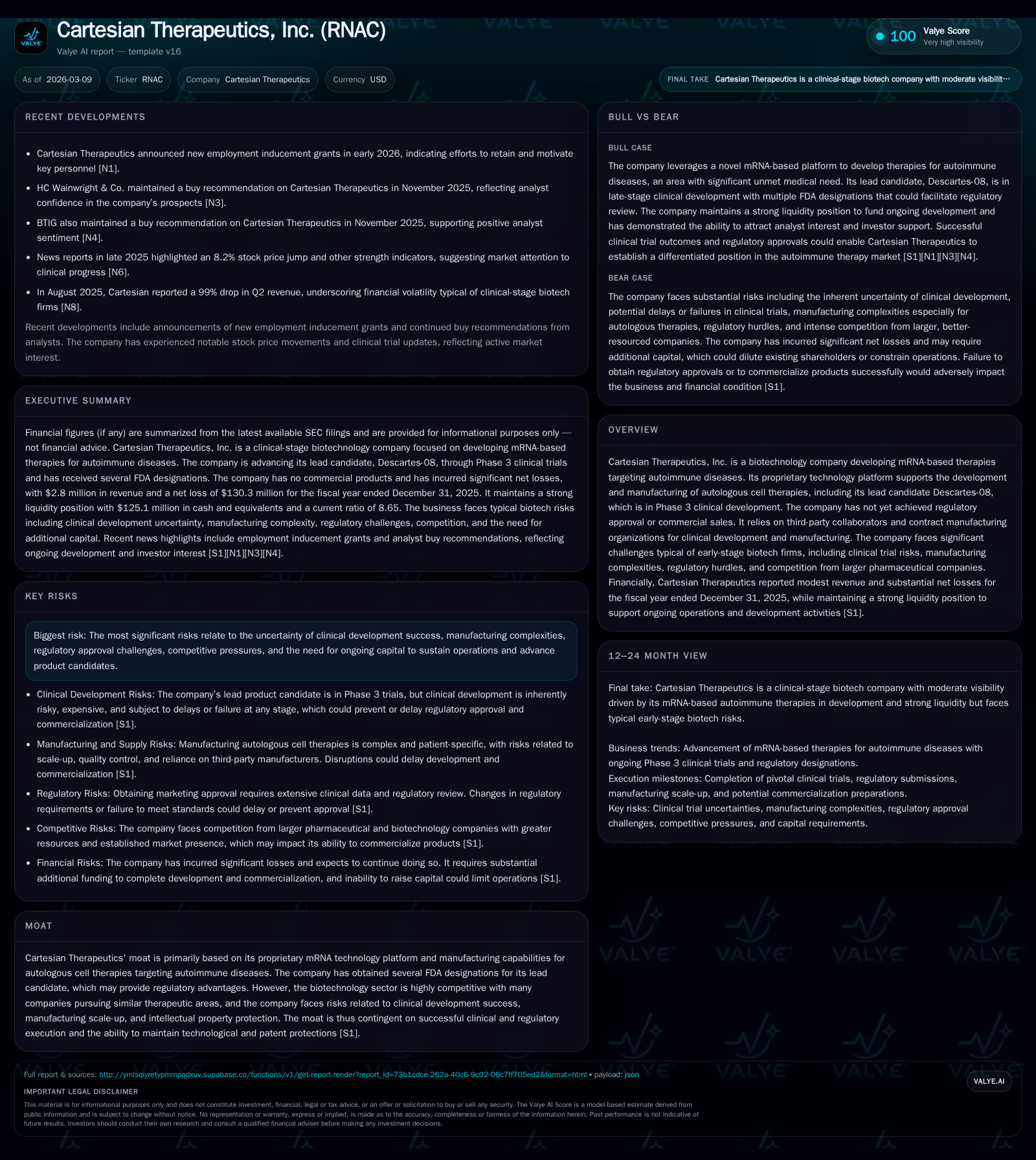

Cartesian Therapeutics Encounters Steep Revenue Decline and High Operating Losses While Advancing mRNA Autoimmune Therapy

The biotech firm’s lead candidate progresses in Phase 3 amid financial strains and operational challenges typical of early-stage drug developers.

Cartesian Therapeutics, Inc. has seen a dramatic revenue drop of nearly 93% to $2.8 million in 2025 from $38.9 million the prior year, driven by the nascent status of its mRNA-based autologous cell therapies for autoimmune diseases. The company posted a sharply increased operating loss of approximately $143 million, reflecting intensified clinical development costs and limited commercial sales. Its lead asset, Descartes-08, remains in Phase 3 trials, positioning the firm for potential regulatory milestones but also exposing it to substantial risks including manufacturing complexity and high capital demands. Despite heavy net losses and negative free cash flow exceeding $79 million, Cartesian maintains a strong liquidity buffer with over $125 million in cash and equivalents at year-end 2025.

Company Overview

Cartesian Therapeutics specializes in developing mRNA-based therapies targeting autoimmune disorders through proprietary autologous cell technologies. Its lead clinical-stage candidate, Descartes-08, is currently undergoing Phase 3 trials—the most advanced stage within its pipeline yet to achieve regulatory approval or commercialization [S1][F1]. Operating mostly through partnerships with contract manufacturers and collaborators due to the technical complexity of cell therapy production, Cartesian confronts the steep challenges typical for early-stage biotechs.

Historical Financial Performance

Cartesian's financial trajectory reveals the taxing nature of its developmental stage focus. Revenue plunged precipitously from approximately $38.9 million in FY2024 to just $2.8 million in FY2025—a near 93% decline—reflecting limited commercial product sales since no marketing approvals have been achieved [F1]. This steep drop likely corresponds with reduced milestone payments or licensing income as pipeline projects transition toward late-stage trials.

Concurrently, operating losses widened substantially to $143.4 million in FY2025 from $43.9 million a year earlier—an increase exceeding 226%—highlighting intensified R&D investment tied especially to Phase 3 costs for Descartes-08 and advanced clinical activities [F1]. Net losses also deepened markedly (down -68% YoY), underscoring a consistent burn that reflects typical biopharma model dynamics well before revenue sufficiency [F1].

Operating cash flow trends echo this spending pattern: an outflow of roughly $73.9 million in FY2025—more than doubling the prior year's deficit—illustrates increasing cash consumption during this critical trial period [F1]. Capital expenditures receded by about 40% but still fueled necessary manufacturing capacity expansions amounting to over $5 million [F1].

Despite these expenses, Cartesian ended FY2025 with a robust liquidity cushion exceeding $125 million and a current ratio of approximately 8.65, ensuring short-term operational funding flexibility absent new capital raises [F1][S12][S23]. There were no dividends or share repurchases reported, pointing to reinvestment priorities.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 3 | -130 | -74 | -143 | -92.8% | -68.3% |

| 2024 | 39 | -77 | -24 | -44 | +64.8% | |

| 2023 | -220 | -51 | -86 | -721.0% | ||

| 2022 | 35 | -32 | 15 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -79 | 103.2 |

| 2024 | -33 | 1138.3 |

| 2023 | -51 | 49.9 |

| 2022 | -33 | 37.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue dropped significantly mainly due to pipeline transition; growing OpInc losses reflect Phase 3 costs intensifying.

Future Growth Prospects

Cartesian's growth narrative is tightly coupled with the clinical success of Descartes-08 and its technological platform for mRNA-driven autologous therapies targeting autoimmune diseases [S1]. Achieving positive Phase 3 results leading to regulatory approvals would unlock commercial sales channels and potential milestone revenues from collaborators.

However, numerous constraints temper this outlook:

- Clinical success uncertainty: No precedent for completing pivotal trials or securing marketing authorizations for their proprietary approach adds binary risks [S1].

- Manufacturing scale-up: Autologous cell therapies pose complex manufacturing logistics often requiring bespoke process validation and cGMP scale expansion that can delay timelines [S1].

- Competitive landscape: Larger pharmaceutical companies with deeper pockets pursue similar autoimmune treatment modalities including mRNA technologies and biologics posing market entry challenges [S24].

- Intellectual property: Protection through patents is critical but vulnerable given evolving biotechnology patent law interpretations reducing enforceability certainty [S14][S15][S20].

- Regulatory environment: Even with FDA designations possibly expediting review phases, final approvals remain contingent on stringent safety/efficacy demonstrations under evolving health policies affecting pricing and reimbursement pathways [S6][S16][S26].

Forecasts / Milestones / Expectations

The company does not provide explicit forward guidance on revenue or readouts beyond confirming active Phase 3 development for Descartes-08 and ongoing investment in scale-up efforts [N1][S1]. Key value inflection points await:

- Announcement of pivotal trial results.

- Submission of regulatory filings (e.g., Biologics License Application).

- Establishment of commercial manufacturing capabilities.

Market observers should monitor clinical trial progress updates and regulatory communications for clarity on timing and feasibility of product launches (analysis).

Returns / Capital Allocation

Returns metrics are currently negative reflecting operating losses exceeding $143 million versus modest revenues [F1]. Approximate return on equity calculated as net loss divided by negative shareholders' equity (-$126 million) signals accounting distortions due to accumulated deficits rather than meaningful profitability insights [F1]. Actual earnings generation remains distant.

Capital deployment prioritizes sustaining research-intensive operations underscored by negative free cash flow near $79 million (operating cash flow minus capex) continuing into at least the next twelve months based on visibility into available liquidity [F1][S23]. Dividend distributions or share repurchase programs are absent given pressing funding needs associated with late-stage clinical work.

Future external fundraises or strategic partnerships will be instrumental to maintain development momentum amidst uncertain macroeconomic conditions affecting capital markets access [S12][S19].

Risk Factors Summary

The firm faces multifaceted risks common among early-phase biotech innovators:

- Clinical failure or safety issues delaying or derailing approval prospects.

- Manufacturing complexities scaling personalized cell therapy products commercially.

- Intense competition reducing market share regardless of approval success.

- Regulatory delays or adverse policy developments impacting pricing/reimbursement.

- Intellectual property challenges potentially undermining exclusivity periods.

- Dependency on third-party contractors introducing operational vulnerabilities.

- Need for continuous capital raising possibly diluting existing shareholders.[S1]

Conclusion

Cartesian Therapeutics stands at a precarious juncture balancing promising science with conventional biotech developmental risks. A successful Phase 3 outcome for Descartes-08 could materially transform the company's financial profile through enabling commercialization and scaling revenues from what currently amounts to a stark operating loss center with dwindling top-line figures.

Nevertheless, major obstacles span across scientific validation uncertainty, logistical manufacturing hurdles inherent in autologous therapies, complex intellectual property environments and stringent regulatory frameworks furthermore compounded by competitive pressures from industry incumbents advantaged by scale and diversification.

From a capital perspective Cartesian’s solid cash reserves support operations over the near-term though further financing will inevitably be required if programs extend without positive inflections.[F1][S12][N1]

This analysis is intended solely as an informational overview highlighting key facets of Cartesian Therapeutics’ business condition derived exclusively from publicly available disclosures; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments