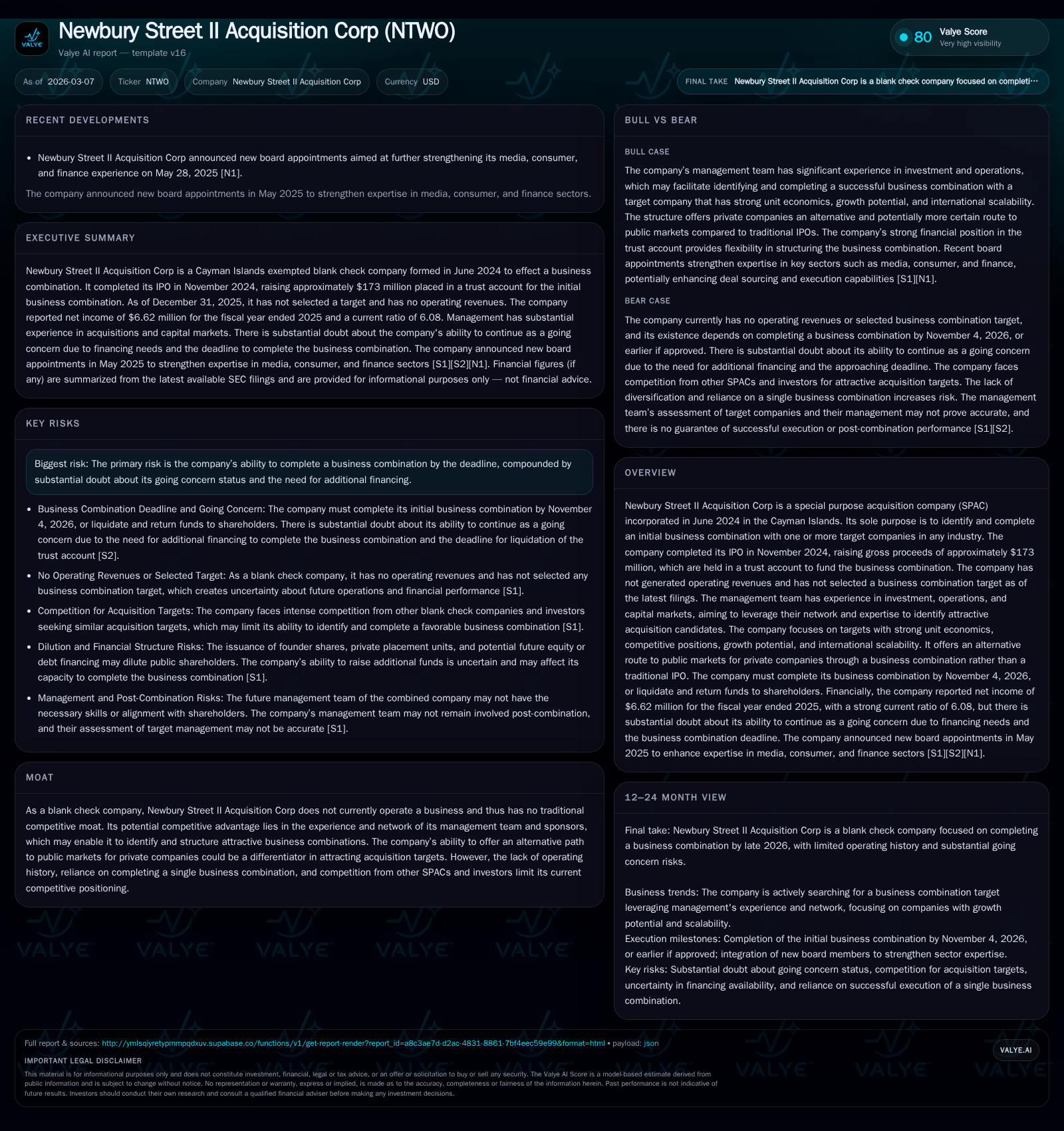

Newbury Street II Acquisition Corp’s Strategic Window to Fulfill SPAC Potential

Newbury Street II Acquisition Corp is at a critical juncture, balancing its trust-held capital and experienced management as it approaches the deadline to consummate a business combination.

Incorporated in mid-2024 as a Cayman Islands-based SPAC, Newbury Street II Acquisition Corp raised approximately $173 million via its November 2024 IPO, currently maintaining over $181 million in trust. Without operating revenues or a finalized acquisition target, the company faces intense timing pressure with a November 2026 deadline to complete a business combination or liquidate. Its management team's capital markets acumen and broad deal-sourcing network underpin its strategy to identify scalable, high-unit-economics targets across industries. However, looming going concern doubts underscore financing risks and shareholder redemption complexities that will define its near-term outlook.

Establishing Foundation: Historical Progress Since IPO

Newbury Street II Acquisition Corp (NTWO) launched as an exempted Cayman Islands special purpose acquisition company (SPAC) in June 2024. It raised gross proceeds of approximately $172.5 million through the issuance of 17.25 million Public Units priced at $10 each during its November 2024 IPO. Additional Private Placement Units contributed about $6.48 million in gross proceeds from sponsors including the CEO-managed Sponsor entity [S1]. The aggregate funds—totaling roughly $173 million—were deposited into a SEC-regulated trust account held by Continental acting as trustee [S1][S11].

Operating activities until fiscal year-end 2025 have been limited exclusively to organizational efforts, IPO costs, and ongoing searches for suitable business combinations. As expected for a blank check entity without operational revenue streams, NTWO reported an operating loss expansion from -$175K in FY2024 to -$688K in FY2025 [F1]. Notably, net income improved markedly from approximately $1 million to over $6.6 million reflecting predominantly non-cash gains or accounting treatments inherent in SPAC structures [F1]. Operating cash flow remained negative but relatively contained at -$464K by end FY2025 [F1]. These dynamics highlight how financial results principally track financing events rather than core operations—a pattern typical among pre-business combination SPACs.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 7 | -464695 | -688452 | +535.3% |

| 2024 | 1 | -298395 | -175611 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -125.2 |

| 2024 | -22.4 |

Source: SEC companyfacts cache [F1].

Financials reflect zero operating revenues consistent with NTWO's blank check profile [F1].

Operational Realities of a Cayman Islands SPAC Structure

NTWO's incorporation as a Cayman Islands exempted company introduces distinct structural features impacting governance and investor protections. Offshore setup offers legal flexibility while maintaining public reporting obligations under U.S. securities laws [S1]. Crucially, all IPO net proceeds are segregated into a trust account under applicable regulations designed to shield investor capital pending consummation of an initial Business Combination [S1][S11][S14]. This "trust account safeguard" limits misuse of funds and assures shareholders that redemption rights can be meaningfully exercised under SEC tender offer rules.

From an investor’s perspective, the structure imposes inherent limitations such as no business diversification prior to deal closure—a single target acquisition must be identified within the two-year "Combination Period" culminating November 4, 2026 [S1][S2]. Security holders enjoy broad redemption rights exercisable regardless of their voting stance on the combination proposal [S7]. These include delivery of shares either physically or electronically per DWAC system requirements ahead of the tender offer expiration [S22][S24], introducing operational cadence that demands shareholder attentiveness.

The limited liability characteristic embedded in the Cayman jurisdiction further delineates fiduciary boundaries between management/sponsors and public shareholders—regulatory compliance remains paramount but enforcement dynamics differ modestly from domestic listings [S18]. Overall governance reflects an intersect between mitigating risks typical of blank check vehicles while offering streamlined path-to-public options for private targets.

Management Expertise and Deal Sourcing Strategy

NTWO’s leadership helms seasoned veterans with deep roots in investment banking, operational management, mergers & acquisitions execution, and capital markets navigation [S4][S9][S14]. Chairman Anthony James Vinciquerra alongside CEO Thomas Bushey (who also manages the Sponsor LLC) bring multi-billion-dollar company-building experience allowing them to apply pragmatic rigor in target evaluation.

Their sourcing strategy leverages an extensive ecosystem—including family offices, hedge funds, private equity firms alongside legal/accounting specialists—to access proprietary pipelines often obscured from broader market competition [S14]. This network-oriented sourcing is pivotal given the competitive capital environment faced by SPACs post-2020 surge.

Crucially, acquisition criteria emphasize structural attributes capable of creating "win-win" transactions with strong unit economics—targets are expected to possess defensible competitive advantages plus versatile growth levers enabling scalable expansion beyond core domestic markets [S14][S21]. Supplementary elements include partnering with incentivized management teams holding meaningful equity stakes post-transaction aligning interests organically.

This dual emphasis on capital markets acumen combined with hands-on integration capability sets NTWO apart within blank check peers by aiming not just for deal closure but for constructive value creation through thoughtful post-merger governance.

Capital Structure, Liquidity Position, and Redemption Mechanics

As of December 31, 2025, NTWO maintains approximately $181.8 million held within its Trust Account net before taxes payable—this cash forms the principal resource contemplated for deployment toward the initial Business Combination or shareholder redemptions [F1][S3][S7][S11]. Outside the Trust Account lies modest working capital (~$772K), funding administrative expenses excluding target bids per required accounting practice.

Capital stock comprises Founder Shares held primarily by Sponsor entities alongside Public Shares distributed in the IPO. Warrants are structured such that each whole warrant grants purchase rights at $11.50 per Class A Ordinary Share exercisable post-combination but provide no direct redemption rights themselves [S1][S7]. Importantly, tender offer rules regulate redemption timing: upon deal announcement shareholders may elect redemption for cash approximating the Trust Account liquidation value per share (about $10.54 at YE2025) [S7][S22][S24].

To mitigate small group enfranchisement blocking combinations through excessive redemptions, redemption restrictions limit any single shareholder’s ability to redeem more than 15% of total Public Shares without board consent; however voting rights remain unrestricted irrespective of redemption actions [S23]. These rules inform strategic calculations around deal pricing and liquidity forecasts since outsized redemptions impose cash strain or drive incremental equity/dilution issuance by NTWO or partners.

The flexibility afforded by executing combinations via cash alone or combined with debt/equity instruments equips NTWO’s Board with tools to tailor transactions financially efficient while preserving optionality regarding pro forma capitalization structures—a vector essential given evolving market conditions potentially influencing valuations or capital access costs near deadline [S9][S12][S17].

Key Risks: Deadline Pressures and Going Concern Doubts

The ticking clock toward November 4, 2026—the final day of NTWO's Combination Period—represents its paramount strategic constraint. Failure to consummate an initial Business Combination by then obliges liquidation protocols mandating return of trust funds less dissolution costs thereby extinguishing ordinary shareholder interests except warrants which expire worthless [S28].

Management candidly discloses substantial doubt about continuing as a going concern citing possible additional financing requirements related both to transaction negotiations and potential unanticipated expenditures [S2]. While liquidity within the trust account supports near-term obligations comfortably today,[...] escalating redemption requests or prolonged target evaluation negotiations may precipitate capital constraints necessitating external solutions including equity or debt raises at potentially dilutive terms [S2][S5][S6][S18].

Competition within the SPAC space adds pressure not only on valuation terms but on deal flow quality as multiple blank-check entities chase overlapping industry verticals / growth themes raising hurdles for NTWO’s management team to secure exclusive pipeline deals meeting all stringent criteria timely.[...]

This risk tableau demands vigilant calendar management plus early milestone disclosures since delays could invoke forced reevaluations impacting market sentiment around deal feasibility even pre-announcement without explicit investment speculation.

Growth Prospects Anchored on Target Selection Criteria

Absent operating history devoid of revenues or production lines—NTWO’s growth potential hinges entirely on successful business combination(s) embodying their articulated selection matrix: prospective acquisitions must manifest clear-cut unit economics enabling sustainable profitability; present defensible market positioning conducive to long duration moats; articulate growth avenues domestically paired with intrinsic scalability beyond U.S borders; moreover benefiting from management teams aligned via meaningful equity stakes promoting incentive compatibility post-combination[S4][S14][S21].

Target attractiveness is enhanced by access to public currency via listing which serves as collateral enabling accretive inorganic expansion projects along with improved capital cost efficiency vs private peers[S14]. This intrinsic optionality situates NTWO favorably vis-a-vis traditional IPO pathways where underwriting uncertainties expose issuers to timing risk plus elevated transactional fees.

The ability of NTWO’s executives both to identify “structural attributes” unlocking deal complexity alongside fostering value-enhancing integrations provides another axis intended to magnify returns bridging raw acquisition opportunity toward lasting franchise building rather than one-off financial arbitrage[S14].

What Investors Should Monitor Ahead of the Combination Period Deadline

Given absent firm guidance on specific targets or timelines investors watching NTWO should concentrate attention on four key areas: (i) any announcements signaling definitive merger agreements or exclusivity deals marking completion progress; (ii) volumes and patterns in shareholder redemption elections which directly affect available cash pro forma transaction; (iii) insider purchasing activity potentially via Rule 10b5-1 plans indicating confidence / positioning intentions; and (iv) emergence of third-party financings whether debt or equity linked filed disclosures implying either anticipated shortfalls or opportunistic capital raises[S10].[...]

Notable deviations such as prolongation beyond commonly observed diligence windows could foreshadow difficulty completing transaction timely while excessive early redemptions might undermine planned deal pricing support necessitating sponsor intervention.[...] Though insiders retain discretion whether or not they initiate purchases given blackout periods plus material nonpublic info constraints limiting manipulative trading risk.[S10]

In this fluid scenario vigilance around filings including proxy statements / tender offers following announcements will sharpen visibility into evolving economic incentives shaping final deal probability scenarios.

Concluding Assessment: Balancing Flexibility with Execution Risk

Newbury Street II Acquisition Corp stands well-capitalized relative to peers entering similar Combination Periods—with trust holdings north of $181 million lending financial ballast against usual blank check volatility[F1][S1][S4]. Strong management pedigree blending hands-on entrepreneurial operational success plus investment banking expertise underpins structured deal sourcing rooted in practical valuation discipline complemented by niche transaction creativity.[S4][S5]

Nonetheless this intrinsic strength contends with stark timeline imperatives exacerbated by sector-wide financing frictions imparting substantial doubt regarding going concern continuity absent consummation.[S2] The window remaining narrows meaningfully requiring rapid execution whilst preserving adequate liquidity for redemptions amid complex shareholder dynamics governed by tender offer rules balancing corporate control against investor protection.[S7][S8]

Capital allocation decisions remain straightforward given absence of dividends or buybacks common at this stage focusing instead exclusively on deploying available capital toward accretive combinations maximizing pro forma market positioning[F1],[S3],[S19],[S20],[S21],[S28]. Vigilant monitoring coupled with measured mitigation strategies addressing redemption flow sensitivity alongside flexible financing alternatives will be critical determinants molding ultimate outcome pathways.

Ultimately NTWO epitomizes contemporary blank-check vehicles balancing structural safeguards against inherent execution uncertainty — rendering comprehensive appraisal grounded foremost not in optimistic forecasting but disciplined observation around forthcoming milestone realizations essential for stakeholders navigating this convergence point between promise and risk.

Disclaimer: This report is informational only and does not constitute investment advice or recommendations regarding Newbury Street II Acquisition Corp securities or any other investments. It is based solely on publicly available information provided by regulatory filings and does not incorporate non-public data nor forward-looking projections beyond documented disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments