Bridgford Foods’ Struggle with Inflation and Commodity Volatility Undermines Profitability

Despite top-line growth driven by price hikes, Bridgford’s profitability and cash flows have deteriorated amid commodity cost swings and liquidity pressures.

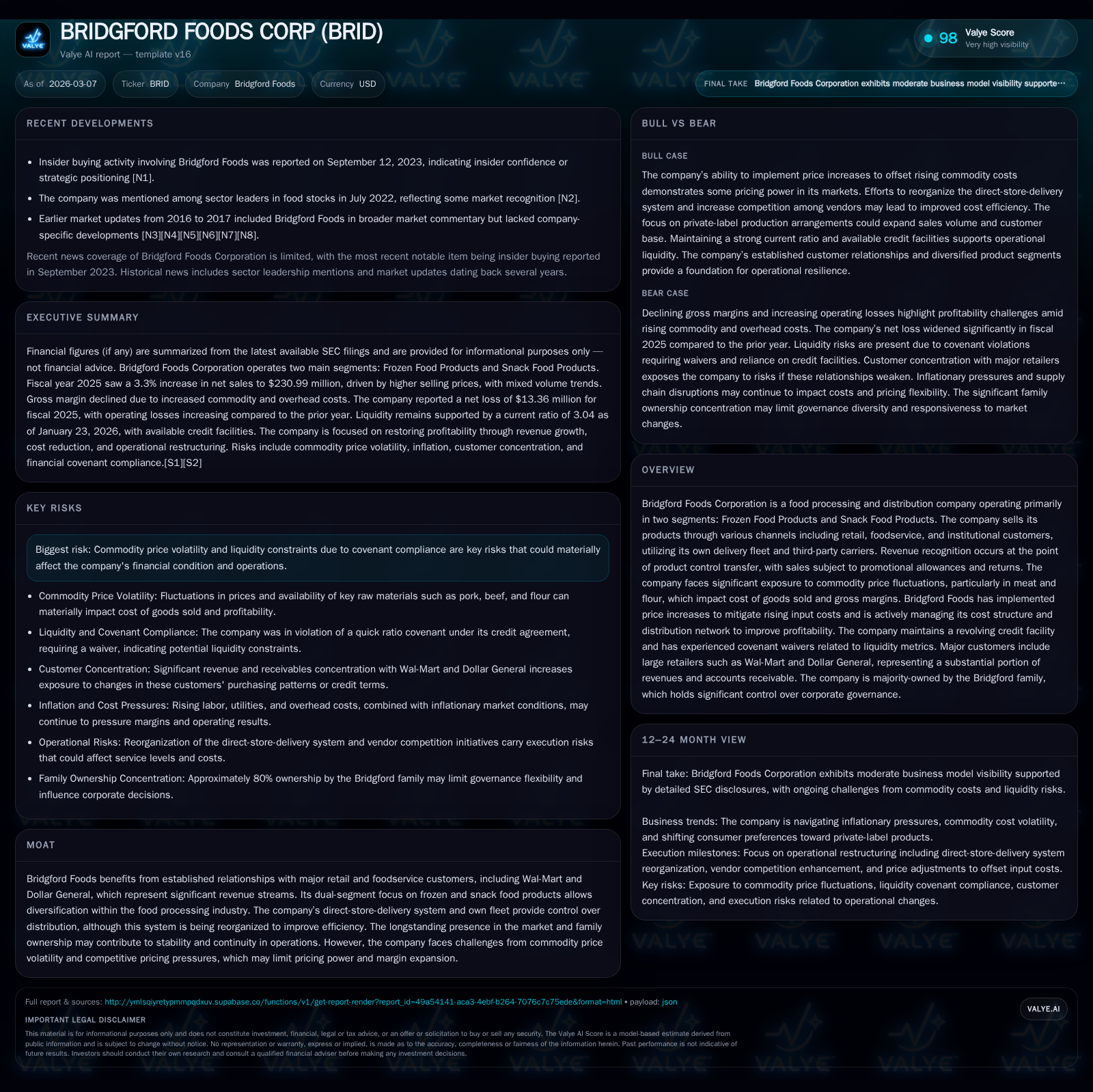

Bridgford Foods Corp has delivered revenue gains fueled primarily by selling price increases, yet these gains mask persistent margin erosion largely due to volatile commodity costs in meat and flour. Operating and net losses deepened significantly in FY2025, while operating cash flow swung sharply negative, reflecting strains from inflation and supply chain challenges. The company faces liquidity pressures with covenant waivers indicating tight financial flexibility, even as it pursues operational adjustments including distribution reorganization and cost controls to stabilize margins. Monitoring Bridgford’s ability to pass through input cost inflation without volume erosion alongside covenant compliance remains paramount.

Historical Financial Trajectory: Growth Amid Emerging Headwinds

Bridgford Foods Corp showed modest revenue growth in FY2025 of approximately 3.3% ($7.3 million increase) reaching $231 million in total net sales [S1][F1]. This top-line expansion was mainly driven by a 3.7% rise in the average selling price per pound across its product portfolio, predominantly aimed at offsetting escalating input costs amid inflationary environments [S1]. However, this revenue improvement masked underlying softness in volumes (-0.5%) and increased promotional allowances which partially offset gains.

Operating income deteriorated sharply by nearly 200%, from a loss of $6.27 million in FY2024 to a loss of $18.75 million in FY2025 [F1], accompanied by a net loss deepening to $13.36 million [F1]. Such magnitude of profit contraction highlights severe margin compression stemming from cost escalations exceeding pricing leverage.

Operating cash flow further underscored profitability stress with negative $5.69 million for FY2025 compared to negative $497k prior year [F1], while capital expenditure investment remained consistent at about $3.6 million [F1], reflecting ongoing production capacity maintenance or upgrade efforts.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -13 | -6 | -19 | 4 | -295.1% |

| 2024 | -3 | 0 | -6 | 4 | -197.3% |

| 2023 | 3 | 4 | 5 | 3 | -92.3% |

| 2022 | 45 | -8 | 65 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -9 | -11.6 |

| 2024 | -4 | -2.6 |

| 2023 | 1 | 2.7 |

| 2022 | -12 | 35.7 |

Source: SEC companyfacts cache [F1].

Revenue growth contrasts starkly with operating losses exacerbated by rising SG&A expenses and cost of goods sold inflation [S1][F1]. The mismatch underscores Bridgford's struggle to navigate transitioning to higher cost inputs while contending with consumer price sensitivity.

Commodity Price Volatility: The Core Margin Pressure

Commodity exposure at Bridgford centers predominantly on pork, beef, and flour — fundamental ingredients for its frozen and snack food products [S2]. These commodities have experienced substantial price fluctuations influenced by global political tensions including conflicts affecting grain supplies (Ukraine-Russia) as well as trade policies such as increased tariffs under recent U.S administration measures [S2].

The company's processing model entails inherent lagged commodity pass-throughs where input cost spikes precede product pricing revisions due to contract terms and market acceptance risks [S2]. During periods of sharply rising raw material costs, this delay compresses gross margins until price adjustments take effect or volumes erode.

Though Bridgford implemented multiple price hikes averaging about +3-4% per pound across segments [S1], these increases have not fully matched the pace or amplitude of input inflation especially given competitive pressures from major retail customers limiting passing the full burden onto consumers [S2][S15]. Persistently high commodity prices contributed materially to the widened operating loss despite the revenue buffer noted earlier.

Segment Spotlight: Divergent Trends in Frozen and Snack Foods

The two reportable segments reflect contrasting performance dynamics reflecting end-market behaviors:

Frozen Food Products: Net sales decreased marginally by approximately $0.36 million (-0.6%) largely due to a 2.7% decline in unit volume that offset a modest 2.2% rise in average selling prices per pound [S1]. Retail sales grew slightly (1.8%), evidencing consumer shift towards at-home consumption while institutional foodservice demand fell (-2.1%), tracking broader industry trends amid economic uncertainty affecting dining out patterns [S1]. Additionally, operational disruptions due to temporary production halts for equipment maintenance also weighed on output volumes.

Snack Food Products: Exhibited more resilience with net sales increasing $7.7 million (4.7%) assisted by combined effects of a slight volume lift (0.3%) along with stronger pricing (+4.2%) per pound [S1]. This segment benefits from dominance in the direct-store-delivery channel popular among retail outlets favoring convenience formats [S5].

The segmentation outcomes display how underlying consumption preferences—retail vs institutional—and channel-specific logistics such as direct-store-delivery versus warehouse distribution influence Bridgford’s revenue mix and operational focus.

Distribution and Pricing Strategy Adjustments

Bridgford operates an extensive direct-store-delivery network particularly vital for snack food products enabling better shelf management and fresher stock rotation under customer control [S1]. However, evolving volume dynamics have prompted the company to initiate a reorganization of its delivery routes supported by rationalization of storage units and vehicle fleets aiming at improved cost efficiencies without compromising customer service levels [S1].

Pricing strategies have leaned heavily on incremental rate hikes averaging ~3-4% across portfolios during recent fiscal years intended to mitigate soaring commodity input costs [S13]. Yet, increasing promotional allowances – effectively discounts or incentives granted post-sale – persist as crucial tools to maintain competitive positioning exacerbating margin headwinds when combined with volatile input costs [S21]. This delicate balance between enabling sell-through velocity via promotions against preserving realized pricing represents ongoing operational pressure.

Capital Structure, Liquidity Challenges, and Covenant Risks

Bridgford’s financial leverage centers around equipment financing loans complemented by an amended revolving credit facility permitting borrowings up to $7.5 million until July 2026 at floating interest rates tied primarily to SOFR plus spreads (~6.77% reported at Oct ’25) [S3][S10][F1]. As of October ’25 balance sheet date, the company had drawn $2 million on the revolver alongside equipment notes totaling approximately $1.79 million; aggregate debt stood near $3.79 million weighted toward current maturities [$3.12 million] due within FY2026 raising short-term refinancing risk concerns [S3][S6][F1].

Crucially, Bridgford breached the quick ratio covenant (minimum required ratio of 1.25x) for the quarter ending October ’25 but secured a waiver from Wells Fargo in December ’25 highlighting immediate liquidity constraints under existing credit arrangements [S6][S11]. The total liabilities-to-tangible-net-worth ratio covenant stood at max 2:1; management remained compliant here but risks persist given operating losses prompting ongoing cash burn.

Working capital assets approximated $62 million against liabilities nearing $20 million reflective of strong current ratio (~3x), yet concentrated accounts receivable exposure exists with around one-third of revenues tied to Wal-Mart and another substantial portion linked to Dollar General raising counterparty concentration risk factors influencing collection cycles [S8][S9][F1].[S4]

The absence of dividends for several years coupled with negligible share repurchases underscores capital preservation priority given weakened free cash flow generation—a gap roughly estimated near negative $9 million when contrasting operating cash flows against capex outlays for FY2025 [F1].

Outlook: Operational Priorities and Risk Management

Looking ahead, Bridgford confronts persistent hurdles anchored principally on managing commodity price swings compounded by inflationary labor and freight costs amid tightening consumer discretionary spending that encourages retailer private label alternatives reducing pricing power [S14]. Key operational priorities encompass refining route-to-market efficiency via delivery network restructuring while maintaining quality service standards essential to major retail partners.

Regulatory compliance risks linked with food safety inspection regimes remain ever-present given USDA oversight particularly over ready-to-eat meat products vulnerable to pathogens impacting brand trustworthiness if lapses occur [S14]. Climate change related disruptions including extreme weather may further affect agricultural raw material availability or pricing trajectories adding unpredictability.

Mitigating strategies involve disciplined promotional spend calibration aligned against measured price increases balancing volume retention potential alongside exploring supplier renegotiations through bidding competition processes currently underway [S13]. Capital deployment will need stringent prioritization focused on sustaining core production capabilities without expanding leverage burdens amid volatile earnings.

Key Metrics: What to Watch Next for Bridgford Foods

Monitoring Bridgford’s trajectory warrants close attention to several nuanced indicators:

- Quarterly sales performance disaggregated by frozen vs snack segments reflecting volume vs price drivers;

- Gross margin evolution juxtaposed against contemporaneous commodity pork, beef & flour market indices observing timing gaps in pass-through;

- Promotional allowance trends as proportion of net revenues signaling discounting intensity impacting net realized prices;

- Receivables aging profile particularly regarding large customers Walmart & Dollar General defining liquidity risk posture;

- Compliance developments around Wells Fargo loan covenants particularly quick ratio restorations or further waivers indicating refinancing flexibility;

- Free cash flow progression critically assessing operating cash conversion given recent negative swings;

- Efficiency gains or setbacks arising from direct-store-delivery route consolidation visible via SG&A expense trends relative to sales.

These measurements will illuminate whether Bridgford can stabilize profitability through calibrated operational adjustments within its capital constraints or if fundamental business model pressures will persist.

This analysis is based exclusively on publicly available SEC filings and company-reported data as referenced; it does not contain investment advice but aims to provide comprehensive insight into Bridgford Foods Corporation’s financial profile and operational context as of early 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments