Grab Holdings Navigates Toward Profitability on Southeast Asia's Digital Frontier

Grab Holdings Ltd achieved its first full-year net profit in 2025, driven by multi-segment growth and strategic efficiencies across Southeast Asia.

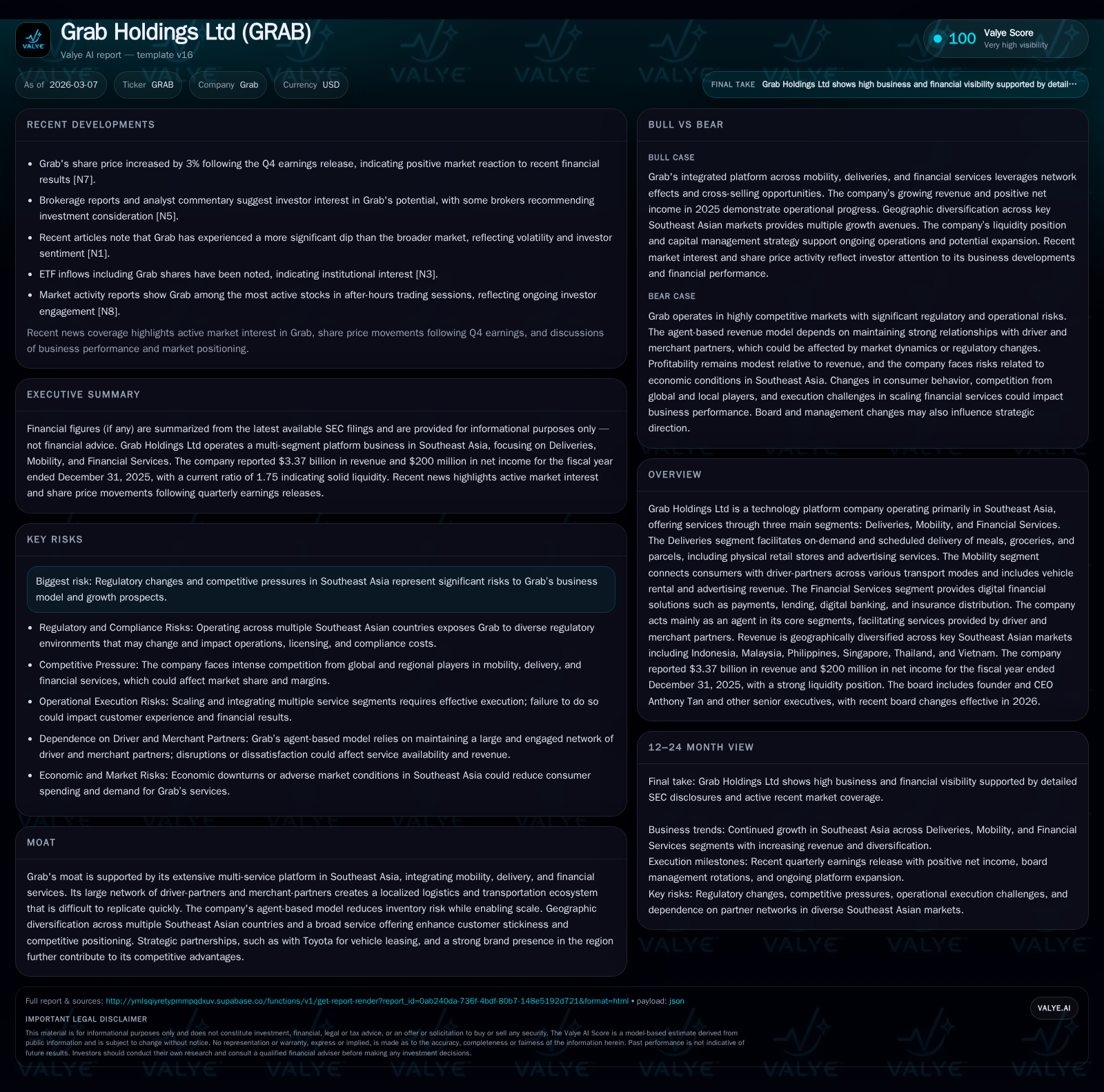

After years of losses, Grab Holdings Ltd reported a significant financial turnaround in 2025 with revenues increasing by approximately 20.5% year-over-year to $3.37 billion and net income swinging positive to $200 million from a prior loss. This improvement was supported by scaling its deliveries, mobility, and financial services segments through an agent-based platform model that leverages extensive partnerships in key Southeast Asian markets. Looking forward, growth hinges on further digital financial services penetration and regional expansion but remains subject to regulatory and competitive risks. The company maintains robust liquidity, improved capital structure, and has initiated a new $500 million share repurchase program as part of its capital allocation strategy.

Financial Turnaround and Historical Growth Drivers

Grab Holdings Ltd demonstrated a remarkable recovery trajectory culminating in its first reported full-year net profit in fiscal year 2025. According to the latest SEC filing, the company registered revenues of approximately $3.37 billion, a 20.5% increase from the $2.80 billion recorded in 2024, supported by robust demand across their core segments of Deliveries, Mobility, and Financial Services [F1], [N3]. Net income swung dramatically from a loss of $158 million in 2024 to a positive $200 million in 2025, representing an impressive +226.6% year-over-year change.

This profitability leap reflects operational leverage derived from expanding take rates within delivery and mobility verticals alongside improved unit economics attributable to higher service completion rates and cost efficiencies as the platform scaled. Strategic pricing adjustments coupled with enhanced marketing effectiveness contributed to this margin progression, as noted in recent earnings commentary [N3]. The company's agent-based model allows it to capture fees primarily rather than bearing direct inventory or asset ownership risk, significantly improving profit conversion on incremental revenue.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 3.4 | 200 | +20.5% | +226.6% |

| 2024 | 2.8 | -158 | +18.6% | +67.4% |

| 2023 | 2.4 | -485 | +64.6% | +72.1% |

| 2022 | 1.4 | -1740 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 3.0 |

| 2024 | -2.5 |

| 2023 | -7.5 |

| 2022 | -26.1 |

Source: SEC companyfacts cache [F1].

Business Model Nuances Across Deliveries, Mobility, and Financial Services

Grab operates an integrated platform across three primary segments:

- Deliveries: Facilitate meals, groceries, parcels via partnerships with merchant-partners; includes advertising services targeting merchants; employs both agent and principal revenue recognition models depending on market role [S4], [S15].

- Mobility: Connects consumers with driver-partners using various modes including taxis, private cars, motorcycles; includes vehicle rentals under leasing agreements notably with Toyota enhancing operating leverage; advertising also contributes revenue streams such as mobile billboards within vehicles [S15], [S20].

- Financial Services: Encompasses digital payments processing fees charged on transaction volumes; interest income from loans extended digitally to consumers, drivers, merchants; digital banking assets; insurance distribution tied back into the ecosystem; advertising complements monetization here as well [S4], [S16].

The company predominantly recognizes delivery and transportation services revenue on a net basis where it acts as an agent connecting service providers (drivers/merchants) with consumers—limiting exposure to inventory or fulfillment risk while optimizing scalability. However, in select markets where Grab controls last-mile delivery directly through subcontracted drivers or couriers, it recognizes gross revenue as principal alongside corresponding cost of goods sold for subcontracted services paid out [S4], [S15].

This hybrid model leverages Grab's extensive logistics ecosystem deeply embedded locally across Southeast Asia—a moat hard for competitors to replicate quickly—anchored by strong partner networks bolstered via strategic collaborations like that with Toyota for vehicle leasing schemes granting flexible access to driver-partners without heavy capex on Grab's balance sheet.

Looking Ahead: Growth Opportunities and Southeast Asia Market Dynamics

Future growth catalysts hinge principally on geographic expansion deeper into Southeast Asia’s high-growth urban centers alongside increased penetration of digital financial services products including lending portfolios expanding loan books underpinned by rigorous credit risk frameworks detailed internally [S9], [S11]. Expansion into insurance distribution and receivables factoring present further avenues for incremental revenue capture within their ecosystem.

Advertising monetization remains nascent but promising as merchant-partners seek amplified visibility via promoted listings spanning physical store operations intertwined with digital touchpoints integrated into Grab’s platform interfaces.

However, significant headwinds persist due to regulatory complexities—Indonesia scrutiny around partnership fairness between large platforms like Grab and small/micro enterprises continues via investigations led by the Business Competition Supervisory Commission over pricing and contractual terms; similarly ongoing cartel allegations regarding fintech P2P interest rates introduce legal uncertainties requiring close management engagement [S9]. Competitive intensity remains elevated as global ride-hailing peers contest market share aggressively leveraging similar aggregation network models particularly in mobility sectors while deepening financial products offerings ([N5]).

Economic conditions such as currency volatility impacting reported results via foreign exchange translations also require careful hedging and monitoring given crossover of operational currencies versus USD reporting base conditions noted internally at the group level [S21].

Monitoring Key Milestones and Analyst Sentiment into 2026

Key upcoming events include the March Extraordinary General Meeting slated for March 24th, focusing partly on governance evolution including director rotations important for continuity amid rapid scaling efforts ([S2]). Investor attention centers on Q1/Q2 earnings releases anticipated early-to-mid-2026 which will serve as critical readouts for sustaining momentum off the profitable FY25 foundation detailed at full-year announcement ([N3]).

Share price showed resilience climbing ~3% following Q4 results reflecting cautious optimism despite volatile sector dynamics ([N1]). ETF inflows spotlighted GRAB among favored Southeast Asian tech stocks underscoring retail institutional interest ([N6]). Analysts remain watchful regarding margin sustainability amid competitive pressures though consensus sentiment registers incremental upgrades given structural progress ([N8]).

Prudent investors will observe leading indicators including delivery volume growth rates deceleration or acceleration patterns within financial services loan book expansions plus regulatory update cadence around Indonesian proceedings governing partnerships to gauge potential directional shifts.

Capital Allocation Strategy: Cash Flows, Shareholder Returns, and Balance Sheet Health

Grab exited FY25 with substantial liquidity positioning — cash & equivalents totaled roughly $3.43 billion supported by strong current assets of $8.08 billion versus current liabilities of $4.63 billion yielding a comfortable current ratio near 1.75 indicative of healthy short-term liquidity buffers able to sustain operating cycles reliably without stress ([F1]).

ROE improved modestly reaching circa 3% for FY25 driven by net profitability gains measured against equity base totaling about $6.76 billion aligning with evolutionary stage from historically loss-making operational phases ([F1]). Operational cash flows have begun trending positively although explicit figures remain embedded within filings without granular quarterly disclosure yet ([S10]).

Board authorization of a new $500 million share repurchase program reinforces commitment toward prudent capital redeployment focused on enhancing shareholder returns absent dividends thus far since inception given reinvestment priorities within growth initiatives ([S7], [S8]). This program allows dynamic execution aligned flexibly with market conditions leveraging open market purchases or block trades.

Debt profile includes convertible notes totaling $1.5 billion maturing in mid-2030 plus manageable bank loan balances supported by modest interest rate exposures indexed variably ensuring optimized debt servicing aligned with financial strategy execution ([S10], [S19]).

Navigating Regulatory and Competitive Risks in the Region

The regulatory environment represents one of the most material uncertainties surrounding Grab’s business prospects. Indonesia’s authorities scrutinize marketplace fairness dynamics especially relating to partnerships with micro-enterprises under current laws enforced actively through investigations against Grab's delivery subsegments along with allegations concerning peer-to-peer lending rate cartels impacting fintech subsidiaries ([S9]). These ongoing probes inject litigation risks requiring dedicated legal-resources focus.

Competition is intensified by Uber-like multi-service platforms attempting regional scale advantages threatening margin compression especially within mobility vertical where price wars routinely erupt ([N5]). Data privacy regulations coupled with compliance complexity across several jurisdictions amplify operational overheads necessitating continuous technological security upfront investments ([S9], [S11]).

Grab’s proactive strategies emphasizing compliance integration combined with engagement programs aimed at government stakeholders help mitigate but not eliminate these risks inherently tied to expansion into emerging regulatory regimes characteristic of Southeast Asia’s evolving digital economy landscape.

Management Team Updates and Governance Influences

Governance changes came into focus recently ahead of March EGM wherein board member Cheryl Goh stepped down while COO Alex Hungate transitions onto the board replacing CFO Peter Oey effective May 1st according to corporate disclosures outlining planned annual rotation practices underpinning leadership agility yet preserving strategic continuity amid executional scaling demands ([S1], [S2]).

Executive leadership features seasoned founders including Anthony Tan spearheading corporate vision balanced by professional operators managing day-to-day operations across mobility/deliveries/financial segments fostering agility incorporating cybersecurity governance oversight central to safeguarding consumer trust at scale typical across high-stakes fintech/tech platforms ([S1]). Quarterly updates provided regularly maintain transparency relating to cybersecurity posture complemented by audit committee reviews evidencing robust risk management frameworks underpinning digital platform integrity essential for brand reputation anchoring regional moat.

Disclaimer: This analysis is presented for informational purposes only based exclusively on provided evidentiary sources without investment recommendations or price targets. All financial metrics are cited from official filings or referenced news articles as indicated.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments