Powerfleet’s Q3 2026 Earnings: Navigating Losses Amidst Leadership Shifts and Strategic Uncertainty

Powerfleet releases Q3 results showing revenue beats but sustained losses, alongside a new chairman appointment and revised outlook.

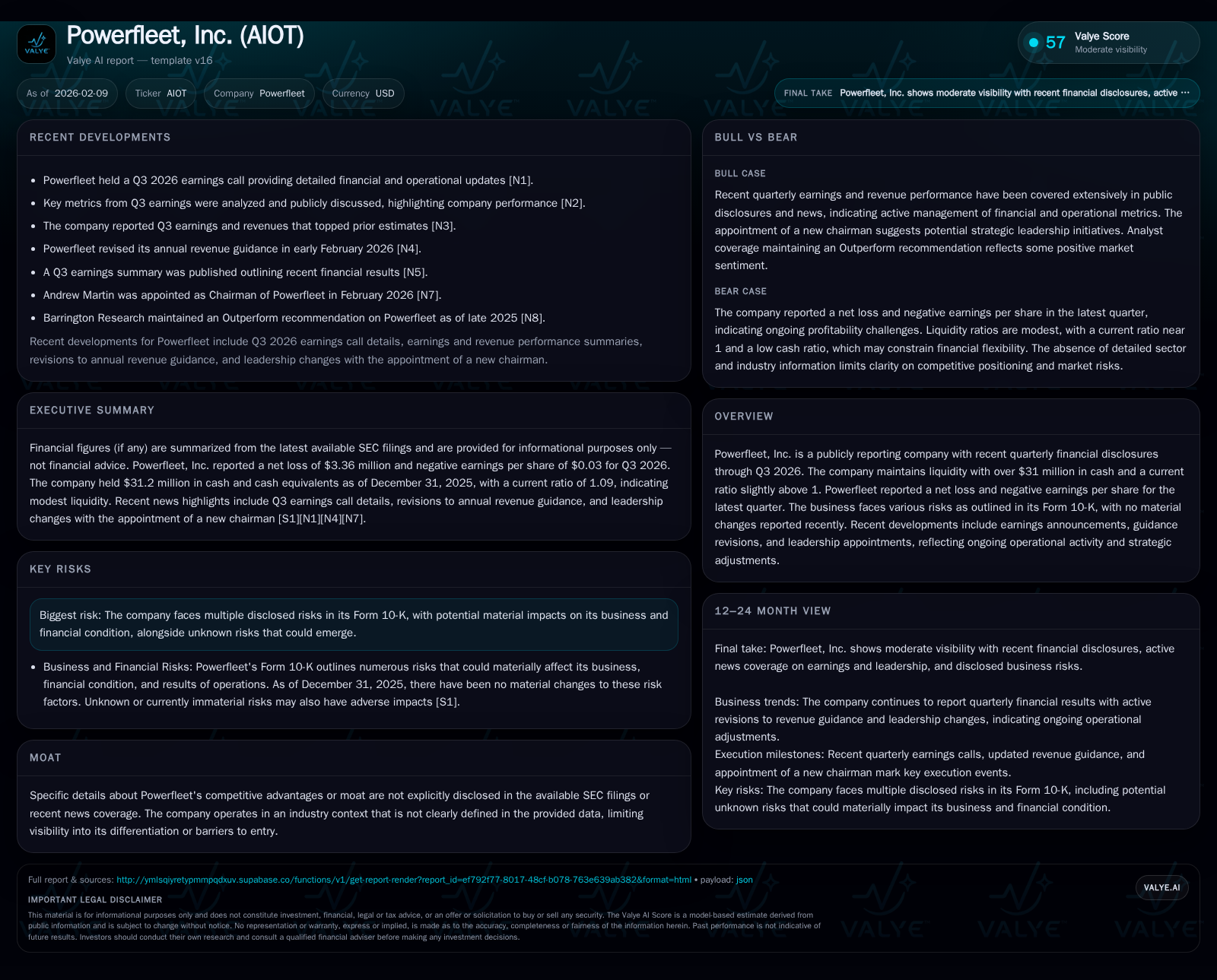

In Q3 2026, Powerfleet surprised markets by exceeding revenue expectations while continuing to post net losses, underscoring complex financial dynamics. The introduction of Andrew Martin as chairman signals potential shifts in governance amid operational challenges. Despite healthy liquidity buffers, risks outlined in regulatory filings persist without material change, casting a nuanced light on the company’s future trajectory. Revised guidance suggests cautious management sentiment as competitive positioning remains unclear within the emergent AIoT landscape.

Q3 2026: Beyond the Earnings Headlines

Powerfleet's Q3 2026 earnings call unfolded with a mix of optimism and caution. The company managed to beat revenue estimates, an encouraging signal at first glance [N1][N3][N5]. Yet beneath this headline lay the persistent reality of net losses that continued to weigh on investor sentiment. The interplay between revenue growth and profitability challenges framed much of the discourse during the report release and subsequent analysis.

The market’s reaction was measured; analysts acknowledged top-line beats but remained wary of structural cost pressures and operational inefficiencies reflected in the bottom line. This dichotomy—stronger-than-expected sales juxtaposed with sustained losses—sets the tone for interpreting Powerfleet's current standing.

Interpreting Revenue Beats Amidst Net Losses

Dissecting Powerfleet's income statement reveals a revenue uptick that contrasts with the ongoing net loss recorded at approximately $3.36 million for the latest quarter-ended period [F1][N2]. On surface metrics, higher revenues might imply improved market penetration or expanding client engagements. However, increasing expenses—possibly driven by R&D investments, sales expansion costs, or broader SG&A outlays—appear to offset these gains.

Such co-existence suggests that while demand for Powerfleet’s products or services grows, scaling costs or margin compression hinder conversion into profitability. The sustainability of this trend is uncertain; without clear evidence of operational leverage taking hold or cost base rationalization, these net losses could persist.

Financial Health Snapshot: Liquidity and Ratios Under the Microscope

From a liquidity perspective, Powerfleet maintains a reasonably comfortable position. With $31.2 million in cash and equivalents [F1], and current assets tallying roughly $175 million against current liabilities near $160 million, the company’s current ratio stands at about 1.09—a thin but positive margin above the critical threshold of one.

This liquidity buffer affords Powerfleet some runway to absorb ongoing losses or strategic investments without immediate solvency concerns. Nevertheless, a current ratio barely above unity signals limited flexibility if operational stresses intensify or if capital needs escalate unexpectedly.

Strategic Leadership: The Impact of Andrew Martin’s Chairmanship

A notable corporate development is Andrew Martin’s recent appointment as chairman [N8], marking a consequential addition to governance layers. While details remain sparse on his immediate strategic agenda, such leadership changes often presage shifts in board dynamics or renewed strategic focus.

Martin's chairmanship might catalyze refinements in execution priorities or instigate governance best practices aimed at shoring up investor confidence after continued financial headwinds. Observers will be keenly watching how his influence shapes forthcoming operational directions amid an evolving industry landscape.

Risks Revisited: Stability or Storm on Horizon?

Powerfleet’s latest Form 10-Q reiterates longstanding risk disclosures without material updates [S2]. This status quo approach indicates that core threats—spanning market volatility, technology evolution pace, competitive pressure, and financial risks—remain unchanged.

Importantly, the filing acknowledges known risks are not exhaustive; undisclosed or emerging factors could still perturb business outcomes materially. This open-ended caution underscores inherent uncertainty inherent in nuanced sectors like AIoT (Artificial Intelligence of Things), where rapid innovation cycles can abruptly reshape competitive positioning.

Guidance Revisions: Decoding Management’s Outlook

Post-Q3 results brought an adjustment in annual revenue guidance downward [N4], signaling management's moderated growth expectations under prevailing circumstances. Such revisions typically integrate internal assessments of customer pipelines, macroeconomic factors, and operational execution risks.

This tempered outlook might reflect a pragmatic recalibration aimed at aligning investor expectations with more conservative near-term performance prospects rather than aggressive expansion narratives.

Competitive Moat Mystery: What Lies Beneath the Surface?

Public disclosures provide scant explicit insight into Powerfleet's unique competitive advantages or barriers safeguarding market share in its domain [valye_report_excerpt.moat]. Absent clear moat articulation complicates understanding how the company differentiates itself within AIoT—a sector marked by intense innovation competition and scalability challenges.

Analysis suggests potential sources of moat might include proprietary technology integrations, customer service models tailored to fleet management solutions, or partnerships leveraging AI data analytics capabilities—but these remain speculative without confirmation.

The ambiguity around sustainable differentiation invites scrutiny over whether existing momentum can translate into durable competitive positioning against entrenched or emerging rivals.

Investor Implications: Pointers for the Prudent Buyer

Synthesizing available data points yields several considerations for investors examining Powerfleet at this juncture [N2][F1][S2]. The company demonstrates top-line growth capacity juxtaposed against ongoing losses—a duality that demands scrutiny over cost structure evolution and margin expansion potential.

Leadership transition introduces both hope for strategic revitalization and typical uncertainties attendant to change at the helm. Meanwhile, unchanged risk profiles advise vigilance around operational and external vulnerabilities intrinsic to both AIoT industry dynamics and general market conditions.

Liquidity metrics offer modest reassurance about short-term stability but also highlight tight financial leeway requiring careful cash flow management moving forward.

Ultimately, evaluating Powerfleet requires balancing optimism derived from recent revenue strength against realism about persistent challenges in profit conversion and opaque competitive moats within fast-moving technology sectors where disruption risk persists robustly.

Disclaimer: This analysis is informational in nature intended for internal reference only. It does not constitute investment advice or recommendation concerning Powerfleet, Inc., nor does it predict future performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments