Xiao-I Corp Adjusts ADS Ratio as It Seeks Market Stability Amid Regulatory and Supplier Concentration

The company announced a one-for-twenty reverse ADS split to address Nasdaq compliance and market liquidity challenges.

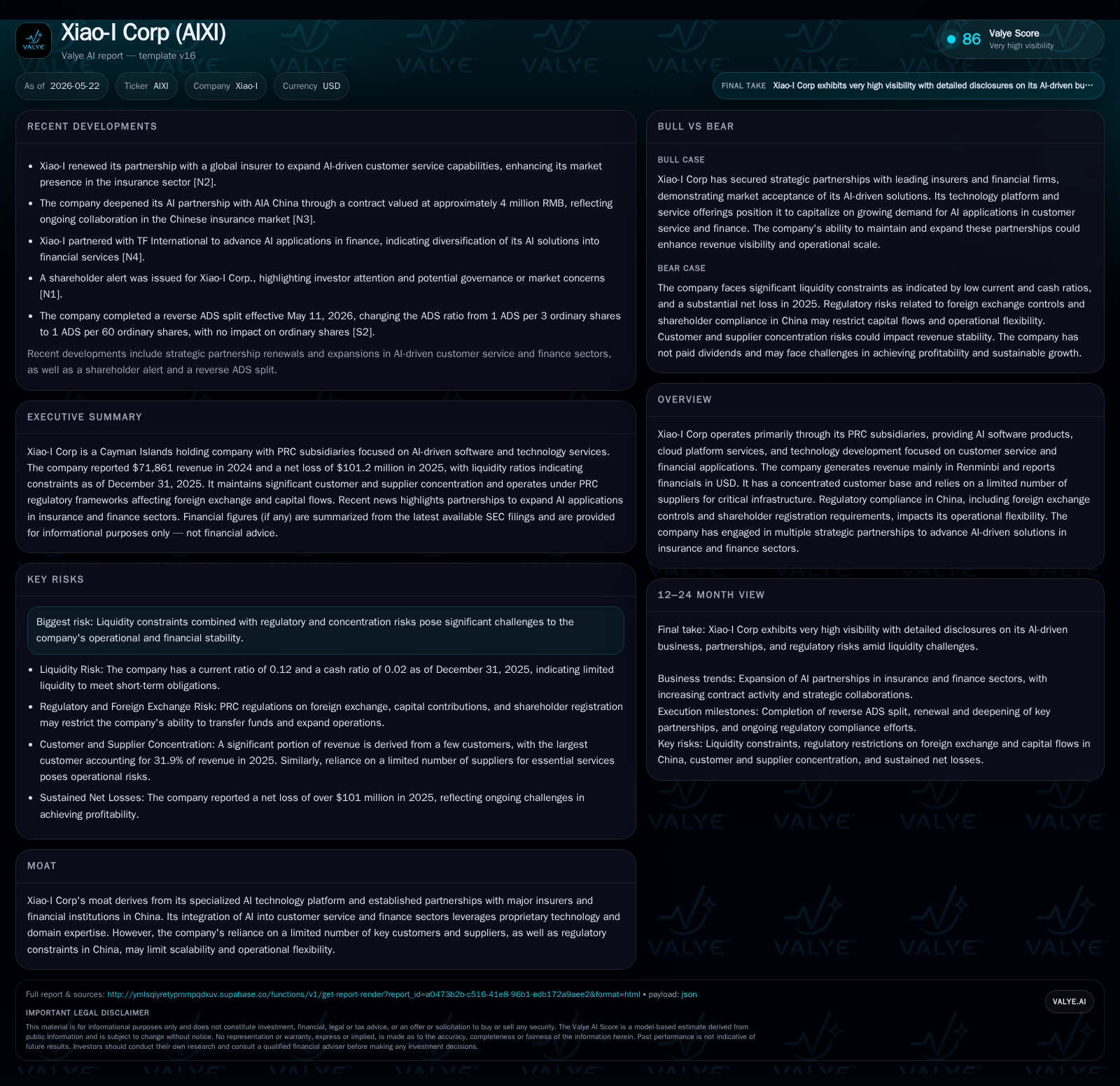

Xiao-I Corporation disclosed a significant ADS ratio change in its May 7, 2026 filing, executing a one-for-twenty reverse ADS split to enhance trading stability and compliance with Nasdaq listing standards. This move occurs against a backdrop of concentrated customer and supplier relationships, heavy regulatory constraints in China, and strained liquidity. The firm's AI-centric business model targeting customer service and financial sectors benefits from niche technology advantages but is limited by supplier concentration and foreign exchange controls. Going forward, investor focus should remain on stock price post-split behavior, operational progress through partnerships, and managing liquidity risks inherent in its capital structure.

Latest Operational Development: Reverse ADS Split Explained

On May 7, 2026, Xiao-I Corporation filed a Form 6-K disclosing a substantial adjustment in its American Depositary Shares (ADS) ratio. The company planned to execute a reverse split equivalent to one ADS representing sixty ordinary shares instead of the prior one ADS for three ordinary shares—a twentyfold reduction in outstanding ADS count effectively. This change took effect on May 11, 2026.

Critically, this adjustment does not alter the number of underlying ordinary shares nor results in cancellation or issuance of new underlying shares. Instead, it solely adjusts the ADS representation ratio. For investors, this means each ADS post-split corresponds to a larger equity block. The primary motive cited is restoring compliance with Nasdaq's Minimum Bid Price Rule by increasing the per-ADS trading price to maintain continued listing eligibility. The company cautioned that while mechanical pricing adjustments are expected proportionally with the split, actual market price movement may vary post-implementation [S2]

This reverse split indicates pressure on Xiao-I’s market valuation metrics and attempts at stabilizing shareholder value perceptions during trading volatility or diminished liquidity. Such moves align with typical corrective actions taken by firms facing sustained low-price trading flags on U.S. exchanges.

Core Business Model: AI Solutions in Customer Service and Finance

Xiao-I principally generates revenue through specialized artificial intelligence software products delivered via its subsidiaries in Mainland China. The business centers on cloud-based platform services coupled with technology development tailored mainly for client service automation and financial sector applications.

Revenues are denominated mainly in Renminbi (RMB) while financial statements are reported in U.S. dollars under U.S. GAAP standards. The product suite encompasses intelligent customer interaction solutions such as chatbots integrated into insurance claims processing platforms and financial transaction support systems.

AI-driven automation forms the strategic backbone allowing cost-effective enhancement of client service capacities among insurers and banks who constitute the firm’s target clientele. Xiao-I leverages domain expertise embedded within proprietary AI algorithms optimized for Chinese language processing and sector-specific workflows.

Revenue drivers include contract renewals tied to software licenses, volume-based service usage fees on its cloud platform, and ongoing maintenance & support (M&S). Pricing schemes reflect combinations of fixed contract components plus variable elements linked to user or transaction scale within cloud-hosted deployments.

Key Customers, Supplier Dependencies, and Regulatory Constraints

Xiao-I faces notable structural dependencies impacting operational scalability and risk profile:

Customer Concentration

The firm has a heavily concentrated customer base; the top five customers represented approximately two-thirds of revenue recently [S22]. This concentration introduces potential volatility risks if major clients reduce scope or delay payments

Supplier Dependence

Supply chain reliance is critical particularly for cloud infrastructure providers supporting Xiao-I’s AI platforms. In aggregate, three main suppliers account for over half of total purchases—providing data center hosting, networking hardware, and cloud computing resources essential for delivering scalable AI solutions [S1][S22]. Such concentration risks could expose Xiao-I to capacity shortages or pricing pressures if vendor terms tighten or disruptions occur.

Regulatory Environment

Operating fully within PRC jurisdiction subjects Xiao-I's subsidiaries to an intricate web of regulations affecting currency conversions, capital transfers, dividend distributions, and tax regimes.

PRC foreign exchange controls impose formal approval requirements through SAFE (State Administration of Foreign Exchange) for converting RMB into foreign currencies primarily related to direct equity investments or repatriations [S1]. These constraints limit funds flowing freely between the offshore holding company (parent entity) and PRC operating units

Dividend payments are restricted; subsidiaries cannot pay dividends beyond accumulated profits after statutory reserve fund allocations have been met. Historically Xiaomi has not declared dividends nor plans near-term payouts under existing financial constraints [S1].

Such regulatory limits curtail corporate agility by restricting liquidity movements needed for working capital or investment expansion.

Competitive Context: Technology Moat versus Concentration Risks

Xiao-I carves out a defensive niche based on proprietary AI technologies aligned purposefully with insurance claims automation and Chinese-language customer support application domains. This specialization comprises advanced natural language processing engines along with customized integration frameworks designed to reduce client switching costs.

Its moat is bolstered by established partnerships with major insurance companies and financial institutions that vouchsafe recurring contracts relying heavily on integrated workflows impossible to replace easily without incurring high switching costs.

However, this technological moat must be weighed against practical constraints:

- Heavy reliance on a small number of large clients limits bargaining leverage against concentrated buyer power.

- Supplier concentration undermines hosting network resilience; there is risk around supply chain disruptions impacting delivery consistency.

- Regulatory complexities endemic to Chinese AI firms limit cross-border fundraising options and increase compliance overheads.

In Chinese SaaS AI markets serving financial verticals where trust and reliability are paramount yet innovation cycles compress rapidly, balancing tech leadership with operational robustness remains challenging.

Growth Drivers: Strategic Partnerships and AI Adoption Momentum

Xiao-I’s expansion avenues arise from deepening collaboration agreements with leading insurers and banks pushing intelligent digital transformation agendas across China’s financial landscape.

These partnerships facilitate co-development projects embedding Xiao-I’s AI models into complex internal processes such as underwriting automation or fraud detection enhancements translating into incremental contract value expansion beyond original scope.

Moreover, increased market awareness around AI-enabled customer service solutions fuels structural demand uplift. Organizations face rising pressure to modernize legacy call centers using scalable conversational platforms capable of handling growing volumes efficiently while maintaining quality standards.

Broader adoption trends within Chinese fintech ecosystems prompt opportunities for Xiao-I to introduce SaaS-enabled add-ons like predictive analytics modules capitalizing on its existing cloud platform footprint.

Risks and Constraints: Liquidity, Customer/Supplier Concentration, and PRC Regulations

Several systemic risks underline caution:

- Liquidity Stress: The company reported operating losses nearing $96.6 million for fiscal year ending 2025 alongside net losses above $101 million despite holding approximately $2.3 million cash versus $1.4 million total debt at year-end 2025 reflecting challenging capital positions [F1]. Strikingly imbalanced current liabilities exceeding $103 million dwarf current assets around $11.9 million producing a dangerously low current ratio (~0.12) indicative of tight working capital constraints limiting day-to-day operational flexibility [F1].

- Counterparty Concentration: Both customer revenue dependency (~66% from top five customers) and supplier share usage (>50% spent on three main vendors) increase exposure to single points of failure or contract renegotiation risk adversely impacting revenues or margins [S1][S22].

- Regulatory Limitations: Foreign exchange regulations inhibit agile capital deployment across borders restricting parent-subsidiary fund flows essential during scaling phases. Statutory reserves obligations limit cash dividend distributions thereby compounding financial resource scarcity internally [S1].

- Internal Controls: Material weaknesses identified previously in accounting practices create execution risk requiring significant ongoing management attention related to U.S. GAAP compliance enhancements underscoring governance vulnerabilities [S3][S18].

Forward Looking: Milestones and Market Signals to Track

Key developments warrant monitoring include:

- Post-Reverse Split Pricing Dynamics: Following the effective date on May 11th, how well Xiao-I maintains Nasdaq minimum bid price compliance through sustained trading levels will impact exchange listing status maintaining investor confidence [S2].

- Operational Leverage Gains: Tracking new client wins or expansions within existing partnership frameworks could signal improved top-line trajectories tied closely to AI adoption momentum specifically within insurance tech niches.

- Liquidity Improvements: Quarterly filings confirming stabilization or easing of working capital deficits would evidence successful internal cost management or external funding initiatives mitigating present strains.

- Governance Enhancements: Updates relating to auditor transitions (effective April 13th audit firm switch) may provide insights into management focus areas around financial control environment strengthening[S3].

- Regulatory Developments: Any shifts easing PRC foreign exchange restrictions or modifying dividend distribution rules could materially affect corporate cash flow management capabilities supporting expansion strategies.

Financial Overview: Recent Performance Snapshot and Capital Structure

These financial dynamics reinforce previously detailed liquidity challenges amplified by customer concentration risks combined with regulatory funding limitations warranting close investor surveillance going forward.

This analysis synthesizes available regulatory filings and corporate disclosures as of mid-2026 without speculative forecasts nor investment research views, providing a rigorous foundation grounded strictly in verifiable operating developments and documented balance-sheet metrics relevant for institutional evaluation purposes.

Financial position in context

As of 2025-12-31, companyfacts shows $2mm in cash and equivalents and $1387082 of total debt [F1]. The same snapshot implies net debt of roughly $-932371, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $12mm and current liabilities of $103mm imply a current ratio near 0.12x for 2025-12-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments