American Shared Hospital Services Battles Liquidity Crisis While Managing Contract and Volume Pressures

Specialized medical equipment leasing and operations confront near-term financial distress amid shrinking procedure volumes and customer concentration risks.

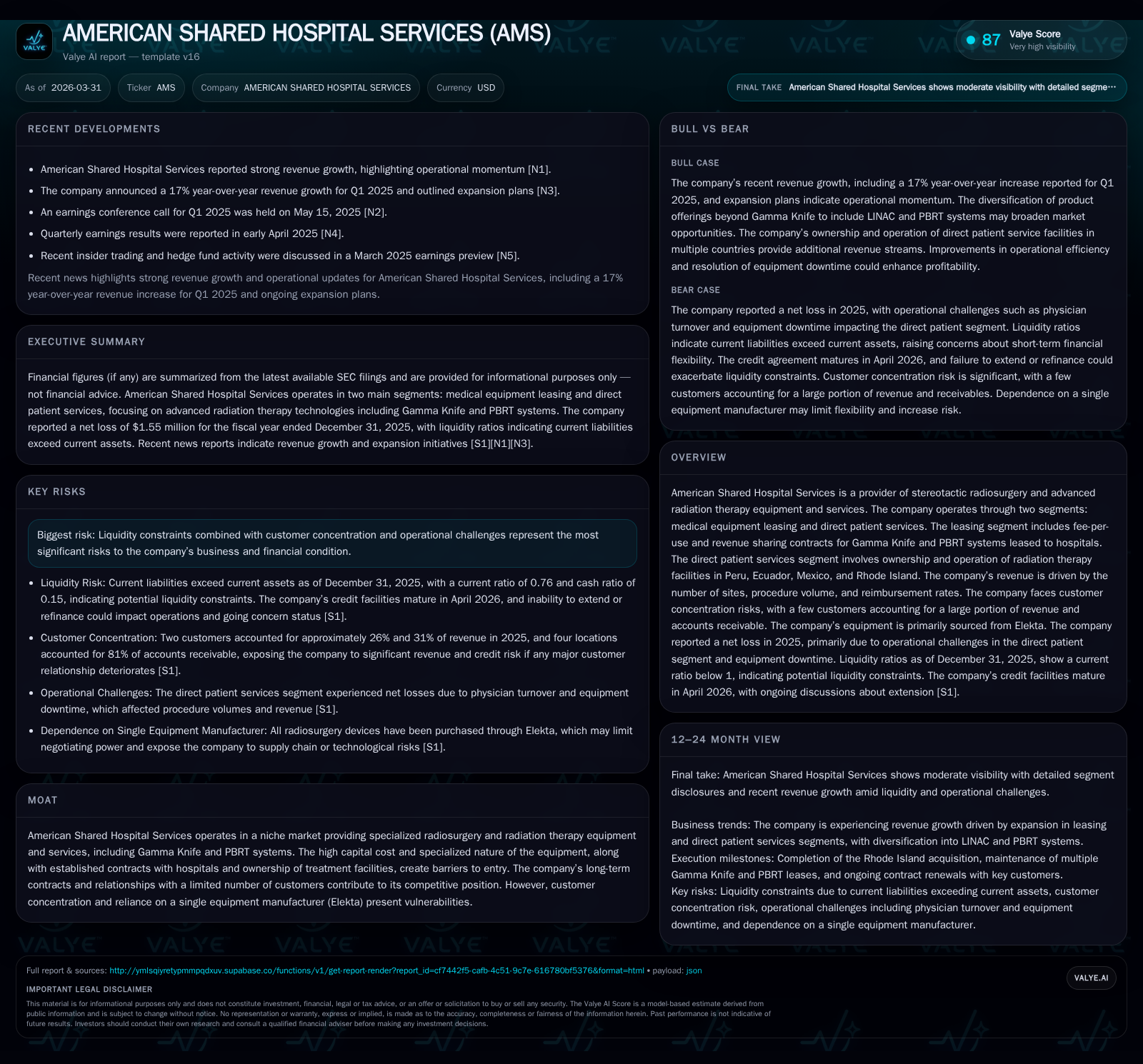

American Shared Hospital Services (AMS) operates in a niche segment providing stereotactic radiosurgery and advanced radiation therapy through medical equipment leasing and direct patient services. The company’s growth has been pressured by contract expirations, declining procedure volumes in key segments, and significant liquidity challenges exacerbated by covenant defaults on its credit agreements. While procedure volume growth was seen in some areas like LINAC treatments post-acquisition, AMS faces substantial risks related to debt maturities, customer concentration, and operational disruptions. The ability to refinance debt and stabilize cash flow will be critical as it navigates these combined headwinds.

Company Overview and Historical Performance

American Shared Hospital Services (AMS) specializes in stereotactic radiosurgery and advanced radiation therapy solutions primarily through two segments: medical equipment leasing and direct patient services [S1]. As of December 31, 2025, AMS leased seven Gamma Knife systems and one Proton Beam Radiation Therapy (PBRT) system under fee-per-use or revenue-sharing contracts with hospitals [S1]. The direct patient services segment operates six facilities—two Gamma Knife centers and four LINAC facilities—including three acquired in Rhode Island during May 2024 [S1].

AMS's total leased sites decreased from ten to eight between 2024 and 2025 due to early lease terminations and expirations, while direct patient service sites remained constant at six [S1].

Procedure volumes reflected mixed trends: Gamma Knife procedures declined about 13.6% year-over-year due to contract expirations (three major leases ended between late-2024 and mid-2025) and downtime for equipment upgrades such as the transition to the Esprit model impacting the Peru facility [S1]. PBRT procedures fell over 21%, likely reflecting cyclical fluctuations [S1]. In contrast, LINAC procedures nearly doubled (+92%) driven by the integration of Rhode Island facilities acquired mid-2024 [S1].

Financially, AMS recorded operating losses worsening from $2.8 million in 2024 to $3.6 million in 2025 with net income shifting from a profit of $2.18 million to a loss of $1.55 million—a clear indicator of operational pressures [F1]. Operating cash flow rose sharply to nearly $3.1 million in 2025 compared to $167 thousand the previous year, largely due to working capital improvements rather than core profitability [F1]. Capital expenditures remained high at approximately $7.6 million focused on equipment upgrades and facility investments—resulting in negative free cash flow around $4.5 million for the year [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -2 | 3 | -4 | 8 | -171.0% |

| 2024 | 2 | 0 | -3 | 8 | +258.4% |

| 2023 | 1 | 6 | 0 | 6 | -54.1% |

| 2022 | 1 | 7 | 2 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5 | -6.5 |

| 2024 | -8 | 8.7 |

| 2023 | -1 | 2.7 |

| 2022 | 7 | 6.1 |

Source: SEC companyfacts cache [F1]. | Revenue not explicitly disclosed for these years

AMS’s approximate return on equity turned negative (~-6.5%) for fiscal year ending 2025 given net losses despite a solid equity base at year-end [F1].

Operational Drivers and Industry Dynamics

AMS operates within a capital-intensive niche reliant on specialized technology primarily supplied by Elekta—the exclusive manufacturer of Gamma Knife systems utilized under lease agreements—and Proton Beam Therapy technologies requiring substantial investment [S1][N1]. These factors create high entry barriers but also supplier dependency.

Significant customer concentration exists with two customers comprising roughly 57% of total revenue during fiscal year 2025 (~26% and ~31%, respectively), elevating risk exposure should contracts not be renewed or customers reduce engagement [S6].

Contract expirations notably impacted revenues as three key Gamma Knife leases ended between late-2024 and mid-2025 leading to lower volumes; same-center procedural growth partially offset declines driven by equipment upgrades enabling broader treatment indications via the Esprit system [S1].

Equipment upgrades led to temporary downtime impacting short-term volume but aim to enhance long-term clinical capabilities.

The direct patient services segment experienced robust growth in LINAC procedures after strategic acquisitions including Rhode Island facilities integrated since May 2024—providing complementary treatment modalities that partially offset declines elsewhere [S1].

Liquidity Challenges and Capital Structure

A critical near-term concern is AMS's liquidity strained by multiple covenant breaches under its Credit Agreement with Fifth Third Bank supporting approximately $16.2 million in long-term debt as of December 31, 2025—a reduction from $18.5 million at prior year-end but insufficient given the looming April 9th maturity without refinancing or amendment [S4][S13][F1].

Key credit covenant terms include maintaining:

- Minimum fixed charge coverage ratio of 1.25x,

- Maximum funded debt-to-EBITDA ratio capped at 3x,

- Unrestricted domestic cash floor of $5 million, all of which were breached during fiscal year 2025 leading to declared events of default notifications from Fifth Third Bank as well as suspension of revolving loan commitments [S4][S16][S17][S20].

The company is negotiating waivers but uncertainty remains regarding lender consent amid defaults [S17][N1]. The credit facilities are secured by liens on substantially all assets including domestic subsidiaries which restricts asset disposals for liquidity management; acceleration rights upon default pose material going concern risks absent refinancing solutions [S8][S12][S15][S21].

Additionally, AMS holds a subordinated loan from DFC secured against GKCE assets totaling about $1.3 million at year-end with waivers granted so far but potential acceleration risks if primary credit issues persist [S16][S20].

Outlook: Growth Prospects Versus Constraints

While no formal forward guidance was issued publicly:

- Expansion of direct patient services through further acquisitions or organic growth could drive procedural volume increases similar to Rhode Island integration effects observed since mid-2024 [N1][S1],

- Equipment upgrades like Gamma Knife Esprit may broaden clinical applications boosting volumes over time post-downtime,

- Reimbursement environment remains uncertain but critical for sustainable returns per procedure.

Risks include:

- Customer attrition especially with further contract expirations scheduled (e.g., one more contract expected mid-2026), potentially reducing volumes if replacements are not secured timely [S1],

- Liquidity constraints limiting investment capacity,

- Supplier dependence on Elekta restricting flexibility.

Investors should monitor:

- Progress on credit facility extensions or refinancing before April maturity,

- Stabilization or improvement in operating results,

- Procedural volume trends following upgrade completions.

Returns and Capital Allocation Priorities

AMS has not engaged in share repurchases or dividend payments recently consistent with a conservative capital allocation approach amid financial stress [F1]. Capital expenditures remain focused on sustaining competitive positioning through technology upgrades rather than shareholder distributions.

Negative free cash flow underscores ongoing funding gaps despite operational cash inflows driven by working capital changes highlighting structural challenges requiring resolution.

Summary: Balancing Niche Leadership Against Financial Fragility

AMS occupies a specialized niche offering advanced radiosurgical technologies supported by entrenched customer relationships and technical barriers linked exclusively to Elekta systems.

However substantial near-term risks persist including procedural volume contractions tied directly to contract expirations compounded by operating losses alongside severe liquidity pressures manifested through repeated covenant defaults threatening refinancing ahead of imminent credit facility maturity.

Management's ability to negotiate extensions or amendments with lenders alongside selective growth initiatives targeting LINAC procedural expansion will be crucial for navigating these headwinds without severe operational disruption or asset impairment.

Disclaimer

This analysis is based solely on publicly disclosed filings up to March 31st, 2026 ([F1],[S#],[N#]) and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments