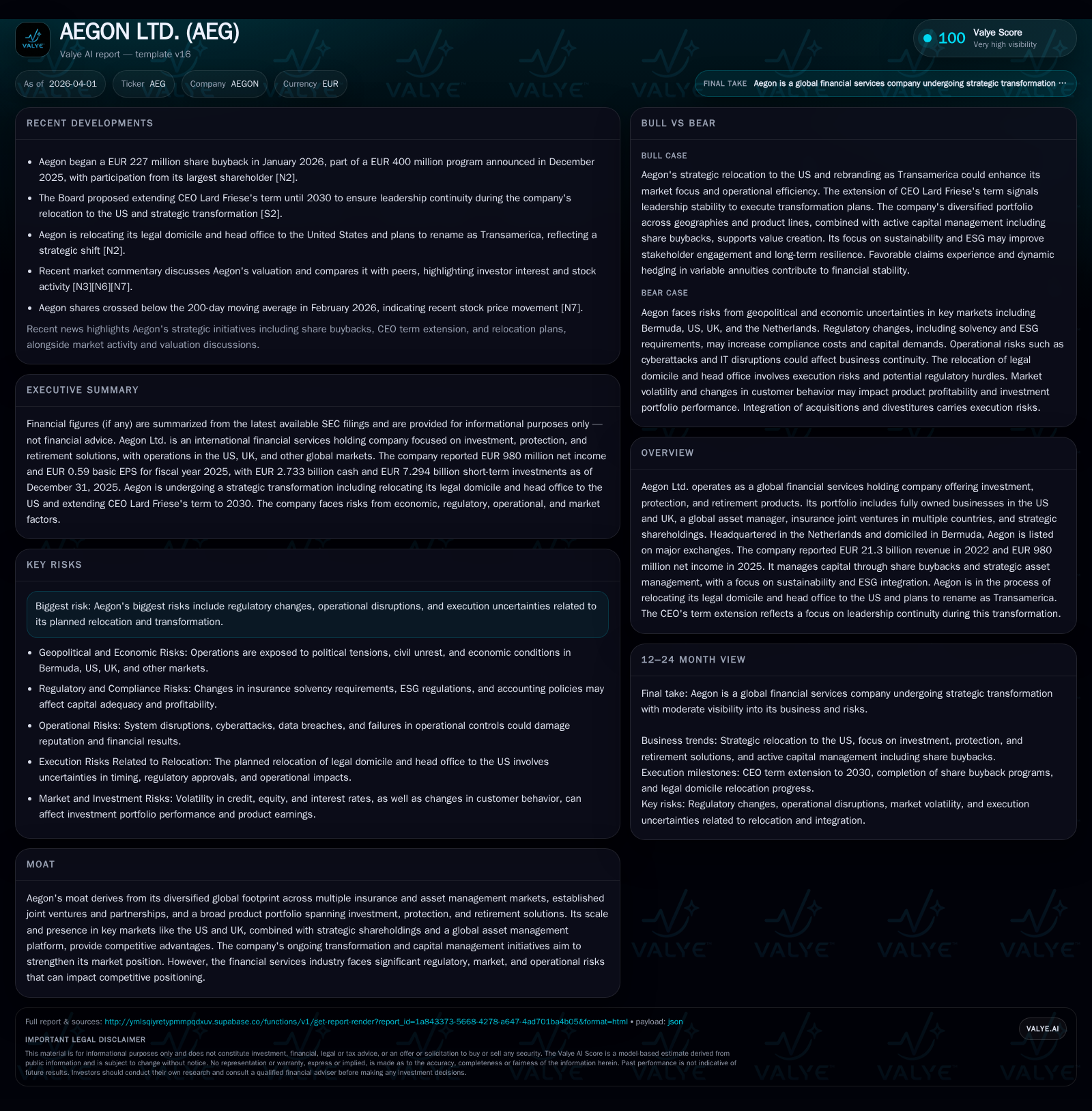

AEGON Ltd. Transformation Spurs Turnaround and Capital Discipline

Aegon Ltd. recovers from prior net losses with leadership stability as it embarks on relocating its legal domicile and headquarters to the U.S.

After a steep revenue decline from €28.2 billion in 2019 to €21.3 billion in 2022, Aegon Ltd. has reversed its profitability trajectory, reporting €980 million net income in 2025 following negative results in preceding years. This turnaround coincides with the company’s strategic decision to relocate its headquarters and legal domicile to the U.S., rebranding as Transamerica, focusing on expanding its U.S. life insurance and retirement market presence. Concurrently, Aegon demonstrates disciplined capital management through robust dividend growth and share buybacks, supporting an approximate 10.3% ROE in 2025 amid ongoing operational transformation and regulatory complexities.

Historic Financial Performance and Profitability Shift

Aegon Ltd.'s financial trajectory over recent years is marked by a dramatic contraction in revenue accompanied by a sharp earnings recovery that underscores a profound transformation journey. The company’s annual revenue shrank from €28.2 billion in fiscal year (FY) 2019 to €21.3 billion by FY2022—a substantial decline of approximately 24% over three years [F1]. This period was also characterized by severe net income losses, highlighted by a €-1.4 billion loss in FY2022.

However, subsequent years show marked improvement. By FY2025, Aegon reversed course decisively, posting a net income profit of €980 million after incurring losses of €199 million in FY2023 and positive but modest profits of €676 million in FY2024 [F1]. This swing from negative returns toward profitable operations indicates successful efforts to optimize cost structures and enhance underwriting margins amidst lower top-line volumes.

Equity capital displays fluctuation aligned with earnings volatility: from €14.2 billion at end-2022 down to approximately €9.5 billion at end-2025 [F1], demonstrating capital base recalibration responsive to operational shifts and risk exposures.

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | 980 | +45.0% |

| 2024 | 676 | +439.7% |

| 2023 | -199 | +85.8% |

| 2022 | -1404 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 596 | 10.3 |

| 2024 | 521 | 7.3 |

| 2023 | 495 | -2.1 |

| 2022 | 347 | -9.9 |

Source: SEC companyfacts cache [F1].

This historic progression reflects Aegon’s strategic reshaping including focused investment on markets where it sees sustainable competitive advantages.

Strategic Renewal: US Relocation and Rebranding Plans

In December 2025, Aegon publicly announced its intention to relocate its legal domicile and head office from the Netherlands/Bermuda arrangement to the United States [S6]. This pivotal corporate action aims not only at tax optimization but more critically aligns with Aegon's strategic ambition to fully integrate into the largest life insurance and retirement market globally—the U.S.

Alongside this move is a planned rebranding whereby Aegon Ltd. will rename itself Transamerica Inc., leveraging one of its strongest U.S.-based operating brands which already accounts for approximately 70% of group operations [S6]. The name change marks a signal of commitment toward establishing dominant presence catering primarily to "Main Street America" families and medium-sized companies.

This transition involves considerable complexity: cross-jurisdictional regulatory approvals, adoption of US GAAP accounting standards expected from FY2027 onwards, restructuring governance frameworks, and aligning compliance protocols across multiple state-level insurers [S2][S6]. Such structural shifts represent not only monetary costs—estimated one-time relocation expenses near EUR350 million—but also operational risks related to executing seamless continuity during migration [S6][S12].

Capital Management: Dividends, Buybacks, and ROE Analysis

Aegon’s capital allocation philosophy has demonstrated consistency even through its transformation phase—with clear emphasis on returning excess capital while maintaining prudential buffers at holding level [S8]. Dividends paid have grown meaningfully from €347 million in FY2022 up to nearly €596 million by FY2025—a near doubling indicative of restored free cash flow confidence [F1][S4][S19].

Moreover, Aegon executed a EUR400 million share buyback program completed by December 2025 that contributed notably to reducing share count thereby supporting per-share metrics; follow-up repurchase programs totaling EUR400 million were launched for fiscal year 2026 [S4][S7][S9]. These moves collectively underpin shareholder returns against the backdrop of improved earnings generation.

An approximate return on equity (ROE) calculation using FY2025 figures yields around 10.3% (€980 million net income / €9.5 billion equity), reflective of significantly improved capital efficiency compared to recent years’ losses while continuing to face margin pressures intrinsic to life insurance underwriting environments [F1].

Growth Drivers and Portfolio Diversification Across Regions

Aegon’s business model is deeply anchored in offering investment products combined with protection (life insurance) and retirement solutions across multiple geographies—primarily via wholly owned subsidiaries in the U.S. and U.K., a global asset management platform, various well-established insurance joint ventures (Spain & Portugal, China, Brazil), and strategic shareholdings such as a stake in Dutch pensions giant a.s.r.[F1][S1]

The diversification helps mitigate localized economic or regulatory shocks yet demands sophisticated portfolio management balancing protection product margin dynamics against fee compression risks characteristic of asset management operations . Particularly notable is the scale achieved via Transamerica’s affiliated distribution network—World Financial Group—with plans targeting double-digit growth rates in life sales backed by enhanced agent recruitment [S21].

Strategic partnerships further bolster earnings quality through remittances that support group operating results without requiring full capital consolidation—a structural advantage utilized effectively amid the relocation initiative [S18].

Navigating Regulatory and Operational Risks Amid Relocation

Foremost among Aegon's current challenges are risks inherent in both its core financial services operations and those specifically tied to the redomiciliation effort [S12][S15][S17][S22][S24][S27].

Operationally, these encompass underwriting uncertainty due to shifting mortality/morbidity trends; exposures linked to catastrophic events; reliance on third-party technology providers vulnerable to cybersecurity breaches; the complexities introduced by fragmented distribution channels; plus hurdles associated with integrating new systems under US regulatory frameworks [S12][S15].

On the regulatory front, evolving solvency requirements across jurisdictions necessitate holding increased technical provisions or additional regulatory capital—factors that calibrate available resources for dividends or buybacks [S20][S24]. The domicile change exposes Aegon to different taxation rules potentially raising effective tax rates along with compliance burdens [S27]. Moreover, retaining top talent amid protracted relocation is critical yet fraught with execution risk including potential cost overruns beyond original budget assumptions [S12][S22].

Vigilant risk governance remains imperative given these overlapping pressures compounded by macroeconomic uncertainties affecting interest rates, inflation expectations, currency fluctuations impacting multinational earnings translation.[N3]

Leadership Continuity: CEO Extension and Governance Implications

In a decisive move underlining board confidence during this transformative period, Aegon's Board announced plans (to be voted on at the June AGM) proposing an extension of CEO Lard Friese's tenure until at least 2030—two years beyond his current term expiry set for mid-2028 [N6][S2].

Mr. Friese has been leading since May 2020 through two significant chapters: initial turnaround stabilization followed by launching aggressive U.S.-centred growth strategy culminating in relocation decisions.

Chairman David Herzog emphasized his "vision centrality" for driving sustainable value creation whilst ensuring strategic consistency during potentially disruptive corporate restructuring phases [N6]. This governance continuity seeks to reduce investor uncertainty associated with CEO transitions amid multi-year complex organizational realignment.

Outlook: Key Milestones and What to Watch Next

Looking forward into late-2026 through early-2028 horizon periods presents several critical milestones shaping investor sentiment:

- June AGM vote on CEO tenure extension solidifying leadership continuity ahead of major implementation phases [N6]

- Progress updates on domicile change formalities aiming for completion around January 1st, 2028 with attendant US GAAP adoption slated for FY2027 disclosures [S6]

- Monitoring earning run-rates primarily within Transamerica operations reflecting sustainable profitability improvement while managing integration costs [S13]

- Tracking dividend policy adherence aligned with promised >5% annual per-share dividend growth funded though improved cash flow generation supported by disciplined capital returns frameworks [S8][S19]

- Potential strategic review outcomes regarding UK unit proposing either accelerated digital transformation or divestment options acknowledging focus shift towards US market priorities [S18]

- Ongoing regulatory developments affecting insurance technical provisions requirements or solvency ratios that might impact dividend capacity or capital allocations [S20][S24]

These developments warrant close attention given their decisive impact on overall financial stability during an extensive remapping from European-centric legacy toward American market leadership ambitions.

This analysis is based solely on information available as of early April 2026 including company filings and public disclosures; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments