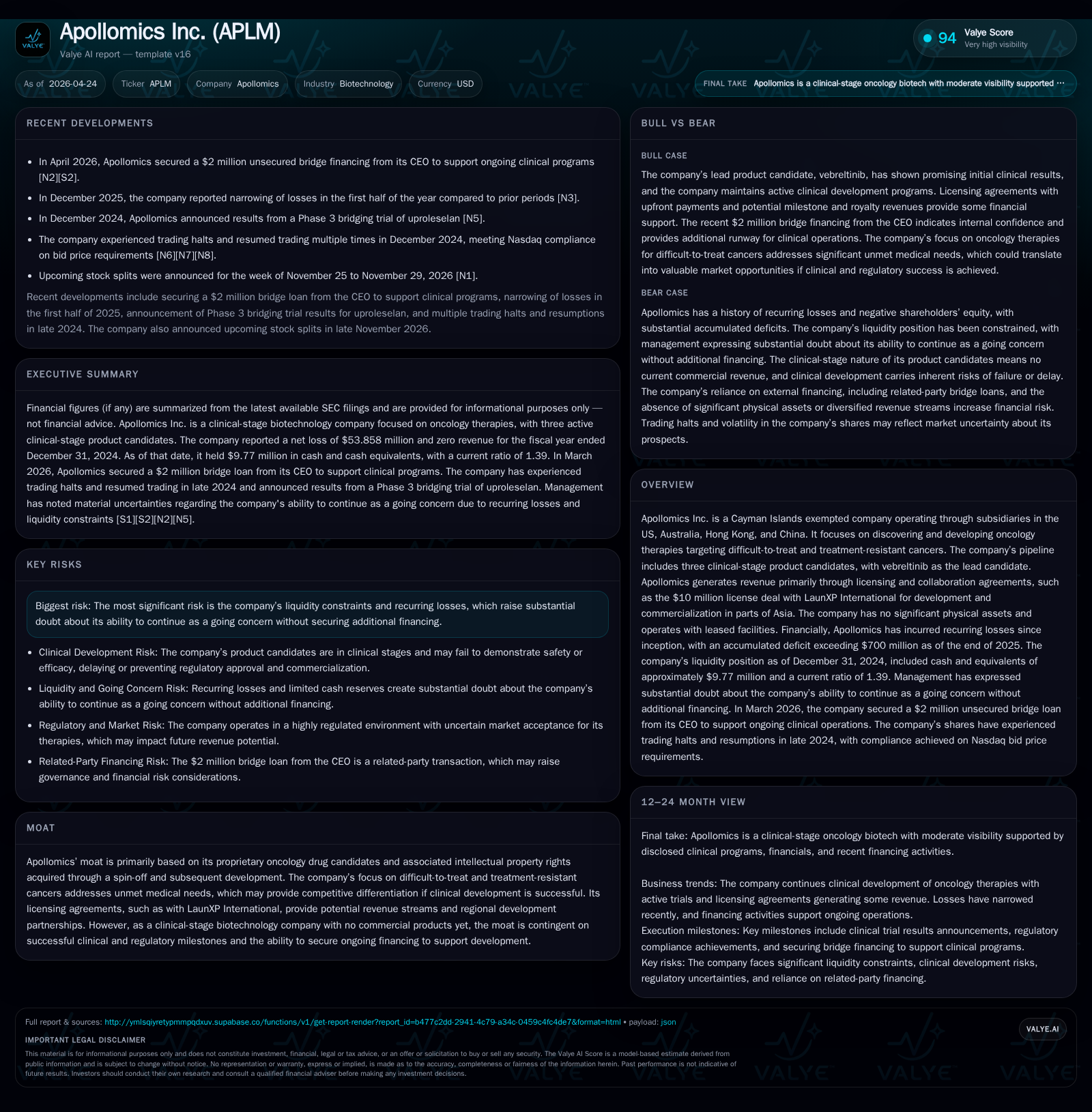

Apollomics Advances Clinical Programs Amid Bridge Financing for Oncology Innovation

Apollomics secures $2 million interest-free bridge loan from CEO to sustain clinical development in challenging oncology niche.

In Q1 2026, Apollomics obtained a critical $2 million unsecured bridge financing from its CEO, facilitating ongoing development of its lead clinical-stage oncology candidate, vebreltinib. The financing, convertible into equity at a discount upon a future $10 million+ equity raise, underscores the company's persistent liquidity challenges amid heavy operating losses. Apollomics operates primarily via licensing deals and collaborations in Asia while focusing on treatment-resistant cancers with proprietary drug candidates. Its growth path hinges on trial outcomes, further financing rounds, and successful partnership extensions within a competitive and highly regulated biotech environment.

Recent Q1 2026 Operating Update: Bridge Loan and Milestones

In March 2026, Apollomics Inc. secured an unsecured convertible promissory note from its Chairman and CEO, Mr. Hung-Wen (Howard) Chen, totaling $2 million [S2]. This zero-interest bridge loan is designed to bolster working capital supporting ongoing clinical operations, especially pivotal as the company advances its lead oncology candidate through clinical trials. The note automatically converts into equity at an 80% discount relative to the lowest price paid by investors in a subsequent equity raising exceeding $10 million—a clear alignment mechanism between management support and shareholder value preservation.

The issuance was approved by an independent Audit Committee despite the related-party nature given Mr. Chen’s executive role. This step both highlights operational urgency amidst persistent net losses and reflects reliance on internal stakeholders for bridging capital gaps.

Business Model Overview: Oncology Drug Development and Licensing Revenues

Apollomics operates as a clinical-stage biotechnology entity focusing strictly on oncology therapies targeting hard-to-treat cancers [S1],. Its revenue generation model predominantly arises from licensing agreements rather than product sales—such as the notable $10 million deal with LaunXP International granting rights within Asian territories [S1]. Revenue from these deals is recognized at the point of license transfer when all performance obligations conclude, reducing future cost or operational burden [S1]. This arrangement limits downstream responsibilities like product enhancement or post-license support.

The company does not have any commercialized products on market currently; instead, it leverages its proprietary pipeline assets to enter collaborations or licensing partnerships that provide milestone payments and upfront fees. This model presents a classic opportunity-risk profile seen in biotechs where commercialization risk is high but early partnering can extend operational runway without incremental CAPEX or infrastructure costs.

Innovation and Product Quality: Clinical-Stage Pipeline Focused on Resistant Cancers

Apollomics’ scientific platform focuses on treatment-resistant cancers—a clinically underserved segment—anchored by its lead molecule vebreltinib [S1],. Developed from spin-off IP portfolios and protected by trademarks across China, Hong Kong, and the U.S., this candidate addresses significant unmet medical needs where standard therapies falter [S6].

While preclinical data positioning apollomics favorably against resistant oncologic indications offers potential moat advantages, approval risks remain high given the stringent FDA processes including IND submissions and phased clinical trials culminating in NDA or BLA filings [S9]. The proprietary nature of the molecular platform supported by IP registrations across key international markets provides formidable barriers against generics or early-stage entrants but is contingent on demonstration of efficacy/safety in controlled studies.

Industry Context: Competitive Set, Regulation, and Intellectual Property Landscape

Operating within the fragmented yet intensely competitive biotech oncology industry, Apollomics faces rivalry not only from specialized small molecule developers but also from large biopharmaceuticals advancing biologics targeting similar refractory cancer types [S4], [S5]. Regulatory challenges loom large: FDA approvals under FDC Act oversight require extended timelines for adequate trial enrollment and endpoint confirmation with accelerated approvals serving as conditional pathways dependent on post-market confirmatory trials [S9], [S22].

Jurisdictional exemptions for R&D patent infringement facilitate operative latitude globally but post-commercialization enforcement remains essential for preserving exclusivity [S6]. Compliance with expansive U.S. healthcare laws governing marketing practices—including Anti-Kickback Statutes and False Claims Acts—adds layers of complexity particularly when transitioning towards commercialization stages [S7], [S8], [S11].

Growth Path Drivers and Constraints: Clinical Advancements, Partnerships, and Financing Needs

The primary driver for growth is successful clinical progression of vebreltinib towards regulatory approval which would unlock pivotal milestone payments and potential commercial revenues directly or via licensing partners. Expansion of regional licensing agreements beyond Asia could diversify revenue streams while extending global reach.

However, growth is severely constrained by the company's consistent net losses (over $70 million accumulated deficit prior to 2025) and liquidity pressures necessitating frequent fundraises or bridge financings such as the recent CEO note, [S2]. Capital intensity of late-stage clinical trials imposes heavy cash burn demands limiting operational runway absent new capital inflows.

Partnerships like LaunXP help partially offset these demands but do not substitute for underlying financing needs tied to long development cycles characteristic of oncology drug approval processes.

Strategic Risks: Liquidity Challenges and Milestone Dependencies

Persistent liquidity stress is a substantial risk factor given the negative equity recorded as recently as end-2025 [$3.2 million net liabilities] combined with recurring annual operating losses ($53.8 million loss reported in FY2024) [F1], [S3]. Dependency on raising upwards of $10 million in foreseeable equity financings is underscored by conversion terms attached to existing debt instruments.

Further compounding risk are milestone dependencies inherent in biotech pipelines—the failure of lead candidates to meet endpoints may derail valuations and precipitate funding crunches. Legal contingencies including ongoing disputes with service providers add another layer albeit currently not deemed materially threatening to solvency [S21].

Review of Key Financials: Balance Sheet Strength, Cash Flow, and Capital Planning

Historical performance (annual)

|

| FY | Rev | Net ($mm) | Net YoY |

|---|---|---|---|

| 2024 | 0 | -54 | +68.8% |

| 2023 | 0 | -173 | +28.3% |

| 2022 | 0 | -241 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | Div | ROE% |

|---|---|---|

| 2024 | 0 | -1107.3 |

| 2023 | 0 | -418.6 |

| 2022 | 0 | 53.7 |

Source: SEC companyfacts cache [F1].

As of December 31, 2024, Apollomics reported cash & equivalents totaling approximately $9.77 million alongside current assets near $10.27 million against current liabilities around $7.4 million representing a current ratio of roughly 1.39 indicating modest short-term liquidity cover [F1]. Net income trends show improvement over recent years from -$240.8 million in FY2022 through -$172.6 million in FY2023 to -$53.8 million in FY2024 though still reflecting ongoing burn.

The newly issued zero-interest convertible note provides short-term relief without adding interest expense burdens but forecasts dilution risk conditioned on future equity raises converting principal at discounted pricing levels relative to next investing tranche price points [S2].

Regulatory submission timelines along FDA guidance compliance will also signal developmental momentum.

Equally important will be announcements regarding execution or closure of the 'Next Equity Financing' event that triggers conversion of the outstanding convertible note thereby reshaping capital structure dynamics [S2]. Expansions or new strategic license partnerships especially in underpenetrated Asian markets offer additional catalysts.

Monitoring litigation developments linked to contract research organizations remains prudent despite current management assessments minimizing potential financial impact [S21]. Any shifts in regulatory landscape affecting pricing or healthcare laws could impose further strategic implications.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available SEC filings and credible news sources as noted; it does not constitute investment advice or recommendations regarding Apollomics Inc.'s securities or operations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments