UTStarcom’s Q4 2025 Result Signals Strategic Shifts in Telecom Infrastructure Innovation

UTStarcom’s recent quarterly results reflect ongoing operational challenges yet underscore its niche strengths in carrier-class telecom infrastructure across Asia.

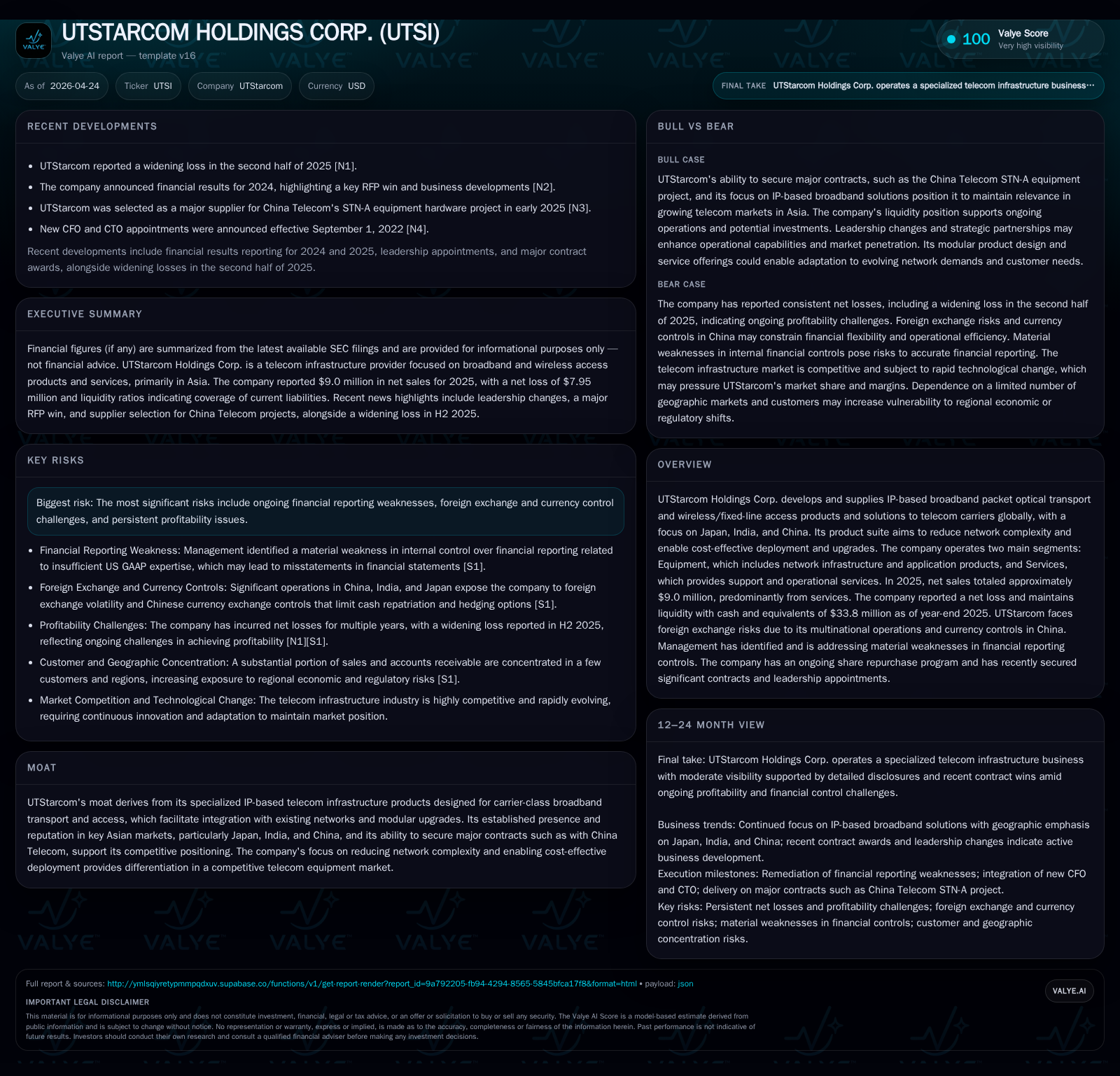

UTStarcom Holdings Corp.'s 4Q 2025 report reveals persistent net losses amid declining revenues, primarily driven by reduced equipment sales and completed service projects. Despite headwinds, the company retains a competitive foothold through specialized IP broadband packet optical transport and access solutions tailored for carriers in Japan, India, and China. Growth is structurally buoyed by escalating bandwidth demand and network simplification needs but constrained by financial reporting issues, foreign exchange controls, and profitability pressures. Key execution milestones to monitor include contract renewals—especially with large Asian carriers—and progress on addressing material weaknesses in financial controls.

Latest Quarterly Results: Operational Highlights and Challenges

UTStarcom Holdings Corp.'s latest interim filing dated March 24, 2026 ([S2]) presents unaudited financials for the second half and full year of 2025. The company reported continuing net losses for the period alongside reduced revenues relative to prior years. Net sales declined roughly 17.5% year-over-year to approximately $9.0 million for the full year ([S12]), driven primarily by a sharp drop in equipment sales—from $1.4 million in 2024 to $0.75 million in 2025—and a fall in services revenue tied to India projects completing with no new major contracts immediately replacing them.

Gross profit compressed significantly, showing a slender margin of about 12% on total net sales compared to 27% the prior year ([S20]). Equipment sales incurred a gross loss mainly due to inventory write-downs and fixed cost absorption challenges amid diminished volumes. Services gross margin retreated due to the high fixed labor costs persisting despite revenue softness.

The cash position remains a relative bright spot; year-end balance sheet data from [F1] shows $33.8 million in cash and equivalents with an ample current ratio of approximately 2.86 ([F1]), suggesting near-term liquidity stability despite ongoing operating cash flow burn (negative $8.82 million in FY2025).

Management continues restructuring actions aimed at reducing operating expenses although these have yet to translate into sustained profitability improvements. The persistence of material weaknesses identified in financial reporting as noted in the annual 20-F ([S1]) adds a wrinkle of risk to near-term outlook clarity.

Business Model Focus: Carrier-Class Packet Optical and Access Solutions

UTStarcom's core value proposition lies in its specialized telecom infrastructure offerings centered around IP-based broadband packet optical transport systems alongside wireless and fixed-line access products ([S1], Valye Report Excerpt). The business operates primarily through two segments: Equipment (network hardware including broadband transport modules and wireless access components) and Services (installation, support, maintenance).

This dual-segment approach allows UTStarcom to cater comprehensively to carrier needs for integrating complex network upgrades while aiming to reduce overall system complexity—an important differentiator given the challenging incumbent telco environments in its primary markets (Japan, India, China). Products are designed modularly enabling carriers to incrementally deploy or upgrade without complete system replacements—a crucial cost-saving measure targeting budget-conscious operators.

The company mainly serves large telecom carriers and cable operators that seek scalable IP-centric broadband infrastructure solutions optimized for mobile backhaul and metro aggregation demands ([S6]). This positions UTStarcom strategically within the value chain between component suppliers and end carrier operators, leveraging tight integration expertise coupled with customization capability as competitive moats.

Competitive Positioning in Asian Telecom Markets

Geographically concentrated exposure defines UTStarcom’s competitive landscape with Japan, India, and China accounting collectively for nearly all revenues ([S12]). Its longstanding relationships with major players such as China Telecom solidify its status as a go-to provider of carrier-grade networking equipment designed specifically for Asian market requirements ().

UTStarcom’s ability to provide cost-effective solutions that simplify network architecture provides insulation from direct price commoditization pressures common among generic hardware vendors or multinational equipment giants. This carrier-class focus supports customer stickiness via technically complex offering features allowing modular upgrades and smoother transitions to next-generation architectures.

Nonetheless, foreign exchange constraints—especially China's stringent currency controls—and geopolitical tensions among these countries introduce operational uncertainties potentially impacting contract negotiations or funding remittances ([S22]). Additionally, ongoing financial reporting deficiencies could undermine trust among institutional customers accustomed to stringent governance standards.

Growth Drivers: Demand for Bandwidth and Network Simplification

Broader industry fundamentals underpinning UTStarcom’s potential growth trajectory include the explosive demand for bandwidth fueled by mobile proliferation, OTT streaming adoption, cloud service usage, and digital transformation initiatives amongst Asian telecom carriers ([S6]).

These demand drivers necessitate continuous network upgrades focusing on capacity expansion while simplifying operations—a niche where UTStarcom’s IP-based packet optical platforms are well suited. The company’s incremental innovation strategy allows customers to enhance existing installations economically rather than undertake costly overhauls.

Given that many Asian operators remain mid-transition towards fully integrated IP/MPLS-based backbone networks, there exists structural runway for UTStarcom’s product suite if it can overcome current commercial execution hurdles.

Growth Constraints: Profitability Pressure, Regulatory & FX Risks

Material obstacles temper near-term visibility. UTStarcom posted an operating loss of roughly $8.56 million in FY2025 with net income down nearly 82% year-over-year ([F1]), indicative of acute profitability challenges stemming from shrinking revenues amidst fixed cost burdens including R&D expenditures totaling $4.6 million annually ([S16]).

Currency controls imposed principally by Chinese authorities limit freely transferable foreign currency balances thereby constraining internal capital allocation flexibility between geographic operations ([S25]). This introduces earnings volatility risk compounded by cross-border regulatory divergences across its main markets.

Management has disclosed material weaknesses regarding financial reporting controls (, [S1]) which could impair investors’ ability to interpret performance trends accurately. These governance issues also expose UTStarcom to compliance scrutiny risks affecting customer confidence.

Operational & Execution Watchpoints: Contracts, Reporting Improvements, and Synergies

Investor focus should track developments around contract renewals or additions particularly with large clients such as China Telecom whose orders materially impact receivables concentration (around 70%) ([S5]). Extending the service backlog or winning new significant equipment deals especially after recent project completions would be key growth triggers.

Progress on addressing audit committee-identified accounting control weaknesses also merits attention as remediation success would bolster corporate governance credibility and potentially improve financing options ([S9], ).

Further cost rationalization initiatives including SG&A reduction efforts reported modest gains last year but require persistence given the ongoing top-line pressures ([S16]). Watch also for potential synergies from cross-subsidiary integration or technology partnerships that management may pursue to leverage product scale or innovation acceleration.

Financial Profile Overview: Liquidity, Losses and Capital Priorities

Historical performance (annual)

|

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -8 | -9 | -9 | 423000 | -82.0% |

| 2024 | -4 | -4 | -7 | 158000 | -13.4% |

| 2023 | -4 | -4 | -7 | 255000 | +23.0% |

| 2022 | -5 | 7 | -4 | 250000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -9 | -21.8 | |

| 2024 | 13000 | -5 | -9.7 |

| 2023 | 13000 | -5 | -7.5 |

| 2022 | 13000 | 7 | -8.7 |

Source: SEC companyfacts cache [F1]. Note: Latest balance sheet datapoints come from [F1] ending Dec-31-2025.

The balance sheet as of December 31, 2025 shows reasonable liquidity supported by $33.8 million cash reserves against current liabilities of approximately $18 million providing a current ratio near three-fold safety ([F1]). Yet recurring negative free cash flow combined with ongoing losses signals the need for disciplined capital management going forward.

The absence of recent share repurchases despite a longstanding board authorization underscores management's prudence about capital preservation amid uncertain profit turnaround timing ([S4]). Rising allowance for credit losses also highlights cautious recognition of collectability risks within accounts receivable portfolios during market softness ([S16]).

In aggregate, while UTStarcom benefits from niche product relevance backed by established customer ties in growing Asian telecom markets, its path toward sustainable profitability is burdened by cyclical project timing variations alongside structural risks stemming from foreign exchange limitations and internal control deficiencies.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments