Intelligent Living Application Group: Strategic Restructuring and Market Diversification under Tariff Pressures

ILAG’s January 2026 quarter highlights accelerated tariff-induced restructuring and a pivot toward Asian markets.

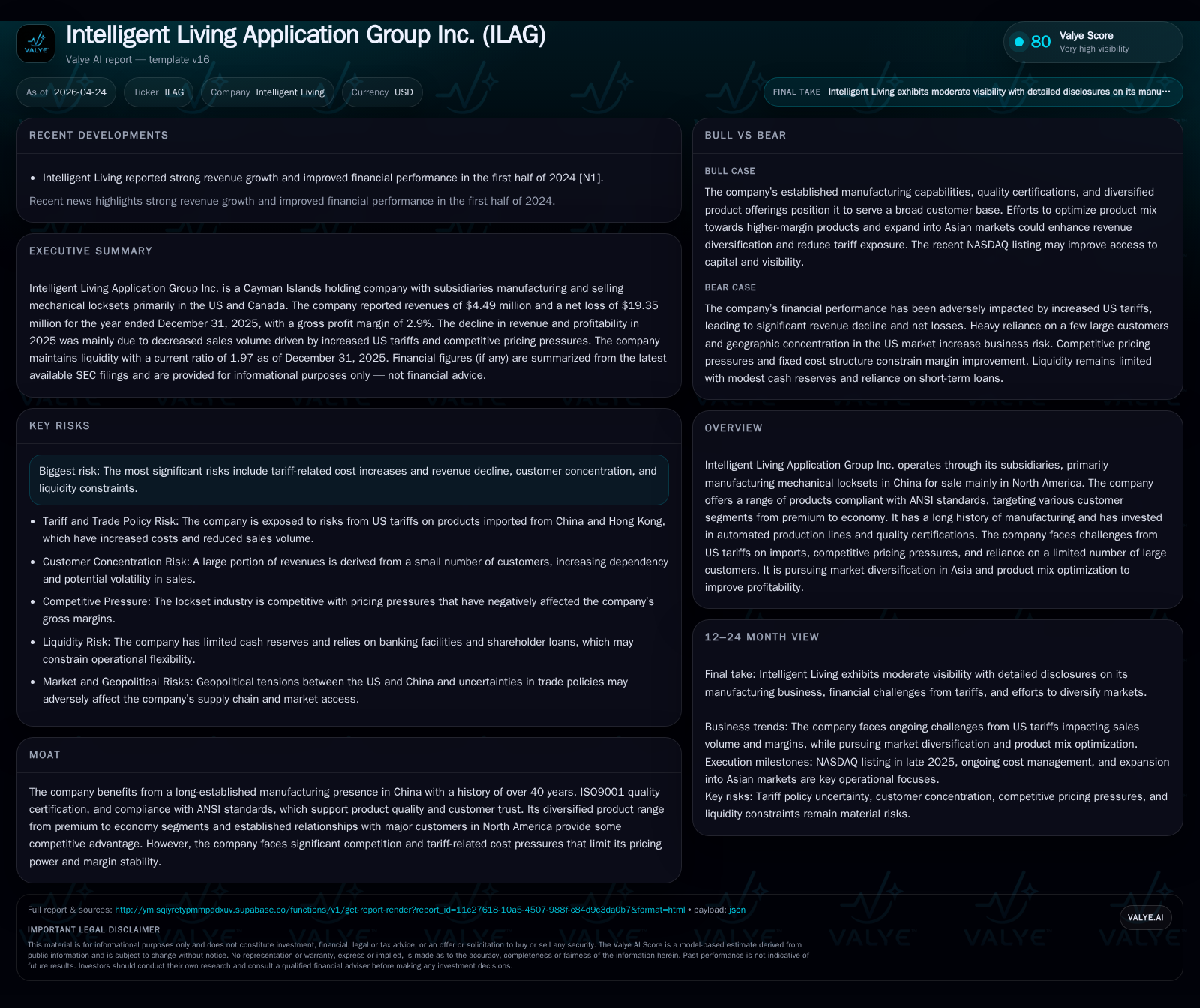

In the latest quarterly update, Intelligent Living Application Group Inc. reported significant operational restructuring triggered by increased U.S. tariffs and declining North American orders. The company is addressing excess capacity through asset impairments and subleasing initiatives while recalibrating its product mix and geographical footprint toward Asia to alleviate margin pressures. Despite strong historic manufacturing credentials and ANSI-certified mechanical locksets catering largely to the U.S., ILAG faces headwinds from tariff volatility, steep pricing competition, and concentrated customer reliance. Continued automation investments and market diversification remain pivotal in its turnaround strategy amid sizable losses reported in fiscal 2025.

Latest Quarterly Overview: Operational Impact of Tariffs and Capacity Adjustment

Intelligent Living Application Group’s January 2026 Form 6-K [S2] sheds crucial light on near-term challenges faced throughout fiscal year 2025 and their response strategies. The company recorded about $2.75 million impairment related to electroplating production lines — assets critical for surface finishing but suffering from reduced expected utilization under revised strategic priorities [S1]. This signals a revaluation of legacy capacity following persistent slowdowns in U.S. demand exacerbated by tariffs.

Further operational shifts include subleasing roughly one-third of Xingfa’s manufacturing plant space (~4,300 m²) at Dongguan facilities in China to reduce overheads during this period of diminished production volume [S1]. The combination of increased tariff burdens—17.5% levied since early 2025—and resultant lower order intake forced management to adjust capacity utilization aggressively while maintaining crucial certification protocols necessary for their ANSI-compliant mechanical locksets.

These measures highlight ongoing efforts to right-size the production footprint amidst external macroeconomic pressures disproportionately impacting imports into North America.

Business Model Insights: Mechanical Lockset Manufacturing and Product Quality Standards

ILAG operates predominantly as an OEM/ODM producer of mechanical door locksets through wholly owned subsidiaries based in China, chiefly serving North American clients via its Hong Kong trading entity Kambo Locksets [S1]. The product lineup spans premium through economy segments, offering designs adhering to ANSI Grade 2 & Grade 3 certifications—benchmarks developed by BHMA that assure buyers of minimum performance thresholds important for both residential and commercial door hardware applications.

Xingfa subsidiary, the core manufacturing hub since inception in the early ’80s, boasts robust capabilities including die casting, furnaces, polishing, and automated electroplating lines underpinning quality control [S1]. ISO9001 certification further reinforces confidence among a largely institutional customer base focused on consistent product performance at competitive price points.

With roughly four decades’ experience refining its processes, ILAG’s manufacturing remains anchored by investments in automation aimed at labor efficiency gains—a vital consideration given rising wage pressures within China’s industrial sectors [S1]. Approximately 78% of revenues still derive from U.S. sales with Taiwan contributing another significant share (18%), underscoring the North American focus despite recent diversification attempts [S1].

Industry Positioning: Competitive Environment and Customer Concentration Risks

The mechanical lockset industry manifests moderate switching costs but intense price competition among manufacturers across China and other low-cost regions supplying the U.S. and Canada. ILAG’s competitive edge lies mainly in sustained compliance with ANSI standards coupled with quality benchmarking secured via ISO certifications which are critical for entry into key distribution channels.

However, as highlighted in the annual report, escalating input costs driven by tariff-related pricing increases materially squeeze gross margins—from a healthy 17.5% in 2024 down precipitously to approximately 2.9% in 2025—reflecting limited pass-through power combined with fixed overhead burdens [S1], [S5]. Raw materials like copper, stainless steel, iron, and zinc alloys dominate cost structures; without long-term supplier contracts, ILAG remains exposed to commodity price fluctuations that are magnified under heavy import duties [S13].

Customer concentration intensifies risk profiles; top five customers accounted for roughly 90% of total revenues during the last two years [S4]. While directly managing large buyer relationships provides some stability, such dependence amplifies vulnerability if major accounts reduce orders or renegotiate terms unfavorably amid economic turbulence.

Growth Strategy: Market Diversification, Automation Investments, and Product Portfolio Optimization

Facing cyclical challenges amplified by structural trade barriers, ILAG pivoted strategically toward market diversification beyond North America focusing increasingly on Asian markets such as Thailand and other Southeast Asia countries [S1],[N1]. This approach aligns with observed declines in U.S. order volumes (down approximately 12.5% units sold from ~1.6M units in 2024 to ~1.4M units including spares in 2025) attributed largely to tariff headwinds [S16].

Automation investments continue as a cornerstone of the company’s restructuring agenda; upgraded equipment reduces direct labor costs while aiming to maintain throughput quality amid fluctuating demand cycles,[S1]. Notably, smart lock projects incorporating IoT features were discontinued late-2025 due to limited funding prospects compounded by adverse market conditions—foregoing earlier attempts at innovation driven by premiumization trends but constrained by resource allocation pressures post-tariffs [S1], [S14].

Simultaneously, ILAG is optimizing its product mix towards higher-margin mechanical lock models while leveraging internet-focused sales under proprietary brand "Bamberg," targeting platforms like Amazon.com for e-commerce penetration and broader geographic reach beyond traditional wholesale channels [S1],. Marketing research expenditure cutbacks in Asia also reflect refined resource allocation favoring proven product lines over exploratory ventures [S14].

Risks and Constraints: Tariff Exposure, Pricing Pressures, and Customer Dependency

Material risk factors remain centered on continued tariff volatility that inflates raw material costs adversely impacting gross margins despite attempts at volume rebate negotiations signed off management discussions [S1],. Fixed production overheads exacerbate margin compressions when sales volumes decline unexpectedly.

The pronounced concentration of revenue among five largest customers (~90%) amplifies vulnerability should any major buyer reduce commitments or shift sourcing preferences—a common dynamic within mature building hardware supply chains characterized by large retail chains or distributors wielding procurement leverage [S4]. Furthermore, lack of long-term supplier contracts imparts sensitivity around raw material pricing shocks which can cascade into cost unpredictability threatening overall profitability sustainability.

Liquidity constraints arise amid extended operating losses as illustrated later; though supported by some available cash reserves, persistent negative operating cash flow highlights execution risks related to turnaround strategies amid macroeconomic uncertainties.

Financial Summary: Profitability Trends, Margins, Liquidity, and Capital Structure

Historical performance (annual)

|

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -19 | -2 | -19 | 0 | -424.3% |

| 2024 | -4 | -3 | -4 | 0 | -5.4% |

| 2023 | -4 | -3 | -4 | 1 | -111.5% |

| 2022 | -2 | -4 | -2 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -2 | -398.4 |

| 2024 | -3 | -29.2 |

| 2023 | -5 | -21.3 |

| 2022 | -8 |

Source: SEC companyfacts cache [F1].

ILAG’s financial trajectory underscores mounting profitability challenges borne out by its fiscal 2025 results filed April 24th describing a stark drop in revenues (-40.1% YoY) down to $4.49 million following prior year $7.51 million peak levels largely reflecting tariff-induced volume slowdowns [F1],[S16]. Operating income plunged deeper into loss territory at approximately -$19.35 million (versus -$3.87 million in FY24), an almost fivefold increase highlighting intensified cost impacts including the $2.75 million asset impairment charge noted earlier [F1],[S23].

Gross margin compression from mid-teens percentage points historically down near breakeven territory (2.9%) reflects limited pass-through ability plus inability to reduce fixed facility-related costs proportionately during downturns [F1],[S13]. Research & development expenses surged (+154%) attributable primarily to one-time termination costs related to abandoned smart lock projects alongside AI robotic production planning adjustments impacted negatively by tariffs and US real estate slowdown effects [F1],[S14].

Despite bleak operating results, balance sheet metrics reveal stable working capital dynamics supported by a current ratio near two (1.97) reflecting roughly $6.8 million current assets versus $3.46 million liabilities as of December-end 2025 alongside net positive cash ($645k) outweighing total debt ($158k) confirming manageable leverage profile albeit modest absolute liquidity buffers given recurring negative free cash flow trends (-$2.45 million FY25) fueling ongoing losses [F1],[S9],[S20].

Capital actions include a recent share consolidation approved December 2025 primarily aimed at compliance with Nasdaq minimum bid price rules enhancing listing stability rather than direct liquidity effects [S4],[S8]. Ongoing working capital funding derives partly from bank borrowings backed by shareholder guarantees evidencing intertwined operational-financial support mechanisms within management.[F1]

Monitoring Indicators: Upcoming Milestones and Execution Focus Areas

Critical upcoming monitoring points revolve around effectiveness of ILAG’s geographic diversification execution particularly traction gained within Southeast Asia markets where initial marketing research was curtailed yet potential remains unproven amidst uncertain tariff outlooks [N1],[S14]. Improvements or stabilization in capacity utilization rates tied directly to success deploying automation upgrades will serve as bellwethers for operational efficiency gains mitigating fixed cost rigidity experienced recently.

Contract renewals or expansions with key major customers will be vital as revenue concentration risks amplify stakes around retention amidst competitive pressures heightened by tariff-induced cost inflation—any erosion here could materially alter recovery prospects.[S4]

Tariff policy developments remain highly unpredictable; timely updates on regulatory adjustments affecting electroplating inputs or final product import duties should be watched carefully for implications on cost structure normalization.[S19]

Subsequent quarterly filings should clarify whether gross margin trajectories improve through targeted volume rebates negotiated partially during late FY25 plus product mix enhancements pivoted towards higher-margin segments.[S5]

Liquidity markers such as cash burn rates relative to financing access will inform capital adequacy perceptions alongside potential strategic pivots involving divestiture or further asset rationalization hinted at during latest impairment disclosures.[F1],[S2]

This analysis synthesizes publicly available filings without offering investment guidance or recommendations. It aims solely to provide an informed perspective grounded in latest corporate disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments