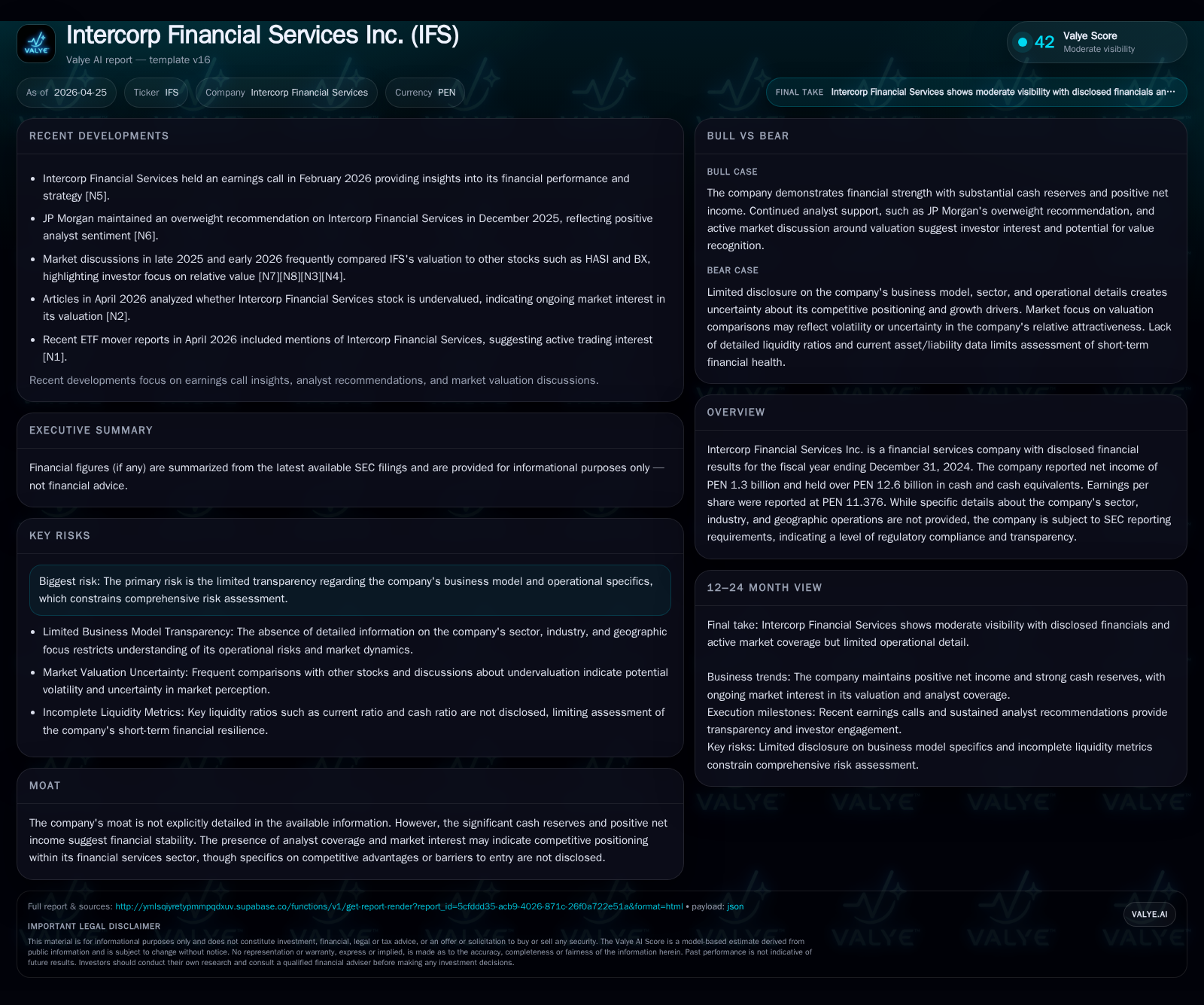

Intercorp Financial Services' Strategic Moves Spotlighted by Quarterly Report

Recent acquisition of a controlling stake in IXP Holding signals Intercorp's commitment to bolstering its integrated financial services platform amid evolving Peruvian market dynamics.

Intercorp Financial Services Inc. (IFS) announced the acquisition of 50% of IXP Holding, completing full control over InFinance XP S.A., marking a significant strategic expansion in its payment processing and financial ecosystem capabilities. This move, disclosed in the April 7, 2026 quarterly filing, aligns with IFS's broader efforts to deepen integration across banking, payments, and wealth management services within Peru’s competitive finance sector. Despite limited transparency on detailed operational metrics, the company's robust cash reserves and steady net income underpin financial stability, while regulatory factors and evolving credit risk policies inform future growth constraints.

Latest Operating Developments: The IXP Holding Acquisition

In its latest quarterly disclosure dated April 7, 2026 [S2], Intercorp Financial Services Inc. announced a definitive Stock Purchase Agreement executed on April 6 whereby it acquired a 50% equity stake in IXP Holding Corp. alongside InRetail Perú Corp., which acquired the remaining half. This deal consolidated indirect ownership of 100% of InFinance XP S.A., formerly Financiera Oh! S.A., a significant player within Peru’s payments processing segment previously partially owned by IFS via PMP.

This transaction marks a strategic milestone by fully integrating core payment facilitation capabilities into IFS’s portfolio through Izipay—currently the group’s centralized payments processor for subsidiaries operating in Peru. This enhanced ownership structure is expected to provide operational synergies through consolidation benefits and strengthened customer value propositions by offering seamless payment acceptance platforms combined with banking products [S2].

Moreover, the April 1, 2026 shareholders’ meeting ratified prudent earnings allocation decisions including allocation of PEN 900 million to voluntary reserves as required by SBS regulation along with allocating PEN 308 million to retained earnings after dividends distribution [S3]. The mandatory nature of these reserves imposes regulatory discipline but limits immediate capital redeployment flexibility without prior approval.

Together these developments underscore an active capital deployment agenda focused on reinforcing IFS’s position within Peru’s expanding digital finance landscape.

Business Model and Product Offering: Integrated Financial Services Ecosystem

IFS operates predominantly through its principal banking entity Interbank alongside wealth management subsidiaries like Inteligo and payment processors such as Izipay. The business model is primarily driven by diversified revenue streams spanning retail banking lending products, transactional fees from acquiring services facilitated by PMP/Izipay, wealth advisory fees from Inteligo’s high-net-worth client base, mutual fund management (Interfondos), brokerage services (Inteligo SAB), and insurance products via Interseguro [S1], [S6], [S28].

Retail loan origination focuses on robust underwriting supported by dynamic collection strategies segmented across early-stage (1–90 days) proactive outreach leveraging credit scoring models and later-stage recovery units for delinquent accounts. Inteligo maintains generous collateral coverage for consumer loans mainly secured against time deposits or securities ensuring minimal non-performing loan incidence (~0.01%) [S1], [S20].

On payments infrastructure, full possession of PMP’s adjacent company Izipay positions IFS as an integrated acquirer providing merchant affiliation services (including low transaction volume merchants) coupled with payment routing to card networks like Visa/Mastercard [S1]. This permits enhanced control over pricing models and service-level agreements underpinning durable pricing power.

By embedding multiple interrelated financial services within one platform—banking deposits/lending, wealth products advisory and payments facilitation—IFS fosters customer retention through cross-selling opportunities while building an ecosystem difficult for peers to replicate without similar scale or regulatory backing.

Market Structure and Competitive Dynamics in Peruvian Financial Services

Peru’s financial industry encapsulates a competitive environment regulated chiefly by the Superintendence of Banking and Insurance (SBS), the Central Reserve Bank of Peru, and antitrust bodies such as Indecopi overseeing competition conditions [S1], [S17]. Within this framework, IFS commands meaningful presence especially via Interbank—a leading retail bank—and its exclusive ownership of PMP/Izipay among key differentiators.

IFS competes against notable players like Credicorp Ltd., particularly through Inteligo contrasting Atlantic Security Bank in wealth management; likewise Niubiz, Culqi represent primary competitors in merchant acquiring space challenging Izipay’s market share [S15], [S17]. Regulatory oversight mandates adherence to Basel III liquidity standards including new liquidity coverage ratios applied since January 2024 restricting rapid asset liquidation risk exposures [S19].

The company also benefits from strong internal governance structures separating commercial units from risk review functions ensuring conservative credit risk concentrations preventing overexposure to any borrower or sector segment [S20]. This operational discipline contributes to maintaining competitive credit quality metrics that cushion cyclicality inherent in emerging market economies like Peru.

Drivers of Growth: Expansion Through Strategic Investments and Service Enhancements

Key growth drivers for IFS include ramping up synergies arising from complete integration of payment processing via the IXP Holding acquisition effectively combining consumer lending platforms with merchant acquiring capabilities allowing bundled offerings with richer value propositions [S2], [S3].

Digital transformation investments planned particularly at Inteligo seek to capitalize on underpenetrated affluent segments delivering personalized advisory services fortified by proprietary analytics platforms improving customer engagement metrics while ensuring scalable cost structures [S1], [S6].

Moreover, expansion into underserved small-and-medium enterprises (SME) via correspondent banking channels leveraging point-of-sale devices leased by Izipay at pharmacies or bookstores creates additional merchant touchpoints enabling volume growth in acquiring fees alongside complementary financing products.

Cross-selling remains central as customers increasingly favor financial groups offering end-to-end solutions under one brand umbrella—a trend reinforcing loyalty and reducing customer acquisition costs while increasing wallet share.

Constraints and Regulatory Environment Impacting Future Trajectory

Despite clear strategic momentum challenges remain centered around evolving regulatory requirements set by SBS including mandatory voluntary reserve buffers which restrict free capital deployment affecting dividend policy dynamics recently seen with PEN 900 million allocated to reserves approved at shareholders’ meeting [S3].

Currency volatility coupled with uncertain future exchange controls poses repatriation risks impacting foreign investor returns even though current laws permit repatriations without restrictions barring certain criminality conditions imposed by Law No. 30737 governing anti-corruption efforts [S1].

Competitive pressures emanating from burgeoning fintech firms innovating rapidly with novel digital native products may erode some client segments if incumbents fail to maintain pace technologically or customer experience-wise particularly within payments facilitation where barriers are lower than traditional banking lines.

Credit risk although currently well controlled could become volatile if macroeconomic headwinds deteriorate business environments impacting SMEs disproportionately requiring agile provisioning methodologies.

Data privacy laws enforced by the National Data Privacy Authority require ongoing compliance investment influencing technology expenditures within digital platforms.

Outlook: Key Milestones and Upcoming Catalysts to Monitor

Looking ahead, several execution points are critical: tracking the financial impact post-consolidation of IXP Holding integration within quarterly earnings will indicate scale-related cost synergies or margin benefits realized beyond stated intentions [S2], [N3].

Advancements related to ESG reporting following recent participation in S&P Global Corporate Sustainability Assessment could enhance institutional appeal potentially lowering cost of capital [S3].

Regulatory updates concerning liquidity coverage ratios or possible SBS amendments impacting dividend distributions merit close observation due to direct financial flexibility consequences.

Technological rollouts enhancing credit recovery automation or AI-enhanced collection workflows may represent further profit levers especially within Inteligo’s loan portfolios.

Finally market reception evidenced via share-price reactions alongside comparative valuation dialogues relative to regional peers will signal confidence levels regarding growth prospects amidst macro uncertainties noted by analysts [N2], [N4].

Financial Profile and Recent Performance Metrics

Historical performance (annual)

|

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2024 | 4 | 1307 | -59.0% | +21.1% |

| 2023 | 10 | 1079 | +56.6% | -35.4% |

| 2022 | 6 | 1671 | -20.0% | -7.2% |

| 2021 | 8 | 1800 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2024 | 427 | 11.9 |

| 2023 | 512 | 10.8 |

| 2022 | 752 | 16.6 |

| 2021 | 634 | 18.8 |

Source: SEC companyfacts cache [F1].

Supporting the operational narrative is the financial profile showing resilience despite cyclical complexities. According to companyfacts data as of December 31, 2024:

- Revenue stood at PEN 4.16 billion,[F1] reflecting a notable contraction compared with prior years possibly due to strategic shifts or portfolio rationalizations.

- Net income remained strong at PEN 1.31 billion,[F1] up approximately 21% year-over-year highlighting effective cost controls or improved margins despite revenue pressures.

- Equity totals maintained robust levels at roughly PEN 10.98 billion supporting solvency needs.[F1]

- Cash and equivalents held were substantial at PEN 12.6 billion[F1], indicating liquidity strength capable of funding acquisitions such as the recent IXP Holding deal totaling US$130 million (~PEN equivalent).

- Dividends distributed in FY2024 amounted to PEN 427 million[F1], subject now to increased reserve allocations constraining distributable earnings going forward.[S3]

This financial footing lends credibility to continued execution on expansion plans balanced against rigorous compliance with SBS directives concerning liquidity coverage and risk buffers.[S5] The approximate return on equity measured near ~11.9%[F1] signals moderate capital efficiency aligned with peer norms under emerging market conditions but leaves room for accretive growth initiatives through ecosystem synergies.

Disclaimer: This analysis is based exclusively on publicly available information including SEC filings dated through April 2026. It does not constitute investment advice or recommendations but aims to provide an informed perspective on Intercorp Financial Services Inc.'s business developments and operating context within the Peruvian financial industry.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments