RLI CORP Stakes Its Niche with Specialty Insurance Focus and Solid Q1 Performance

RLI Corp’s Q1 2026 results underscore its specialized underwriting strengths and diversified distribution as key growth levers in the specialty insurance market.

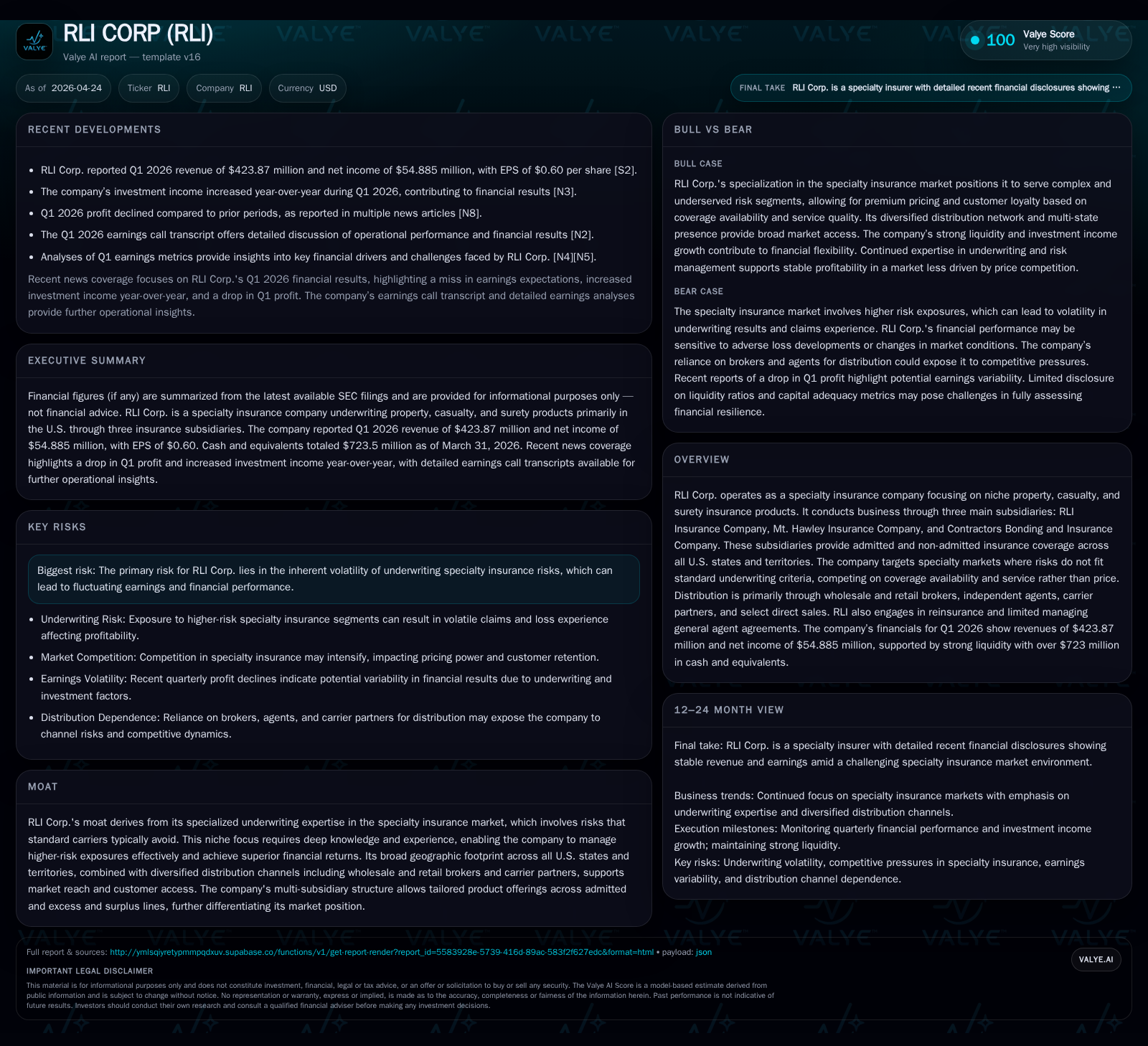

RLI Corp reported first-quarter 2026 revenues of $423.87 million and net income of $54.88 million, slightly missing earnings expectations despite improved investment income. The company’s specialty focus, spanning admitted and excess & surplus lines through three subsidiaries, continues to differentiate it in a market driven by coverage availability over pricing. RLI’s broad geographic footprint and multi-channel distribution support steady premium growth, though underwriting volatility remains an inherent risk. Strong liquidity and conservative leverage underpin financial stability as management navigates evolving specialty insurance dynamics.

Recent Operating Update: Q1 2026 Performance Highlights

RLI Corp’s latest quarterly filing (Form 10-Q dated April 24, 2026) reveals revenue of approximately $423.87 million for Q1 2026 alongside net income of $54.885 million. While the quarter showed an uptick in investment income relative to prior periods, underwriting results posed challenges leading to a modest shortfall against analyst earnings estimates [S2][N3]. The combined ratio—though not explicitly detailed in the excerpt—likely exhibited some pressure given the lower-than-expected bottom line.

Management commentary from the April 23 earnings call transcript framed this outcome within industry-wide volatility affecting specialty lines and reiterated discipline in pricing and risk selection [N2]. Further corporate updates around April 22 via Form 8-K confirmed ongoing initiatives to optimize reinsurance structures and refine product offerings aligned with shifting market demands [S3]. This operating environment remains dynamic, with RLI leveraging its underwriting technical capabilities to navigate fluctuating loss trends.

Business Model Deep Dive: Specialty Insurance and Product Differentiation

RLI Corp's business model centers on underwriting selected property, casualty, and surety insurance products targeting specialist niches underserved by standard carriers [S1]. Conducting operations through three segment-focused subsidiaries—RLI Insurance Company (admitted lines), Mt. Hawley Insurance Company (excess & surplus non-admitted lines), and Contractors Bonding and Insurance Company (specialized admitted coverage)—the company spans all U.S. states and territories with tailored product sets.

Unlike commoditized standard insurance markets where price often drives competition, RLI differentiates via underwriting expertise that manages complex or higher-risk exposures effectively [S4]. This specialty focus requires rigorous risk selection capabilities that constitute the firm's competitive moat — an ability to profitably underwrite risks avoided by mass-market insurers while offering coverage breadth supported by robust claims handling.

Revenue streams derive primarily from written premiums across these specialized lines along with investment income from its sizable fixed-income portfolio. The company also supplements growth via limited direct sales channels and strategic managing general agent partnerships that extend reach without diluting control [S1]. This layered approach balances disciplined underwriting with selective distribution expansion, ensuring alignment of risk appetite with sustainable growth.

Competitive Landscape: Market Position and Distribution Channels

In the fragmented specialty insurance sector marked by a mix of admitted and excess & surplus carriers, RLI holds a unique positioning enabled by its multi-subsidiary architecture serving different licensing standards nationally [S9][S20]. Its presence in all U.S. jurisdictions equips it to write diverse risks at scale while managing regulatory complexity adeptly.

Distribution operates through a balanced ecosystem of wholesale brokers specializing in complex risk placement plus retail agents serving regional markets — complemented by partnerships with carrier networks providing additional access points [S1]. This multi-channel strategy reduces reliance on any single route-to-market and enhances renewal persistency via broad intermediary relationships.

Crucially, competitive differentiation stems not from aggressive pricing but from providing availability where others decline coverage due to higher volatility or specialization requirements [S4]. Such a focus tends to command stronger client loyalty based on service value rather than price swings — an important structural advantage in the specialty space where switching costs are embedded in underwriting familiarity.

Growth Drivers and Challenges: Assessing Expansion Potential

The core driver underpinning RLI's growth trajectory is its specialized underwriting discipline targeting niche markets characterized by persistent demand for coverage unavailable in standard pools [S5][N13]. By maintaining expertise in sectors like contract surety bonds or executive liability where risk profiles deviate from conventional models, RLI captures premium volume at adequate rates that justify elevated risk retention.

However, inherent challenges accompany this niche approach. Specialty lines carry greater loss volatility potential — accident years can yield latent losses or concentrated large claims that disrupt earnings consistency [S5]. Market cycles influence capacity availability sector-wide; therefore, sustaining pricing adequacy remains critical to offset elevated claim severity trends observed intermittently.

Competitive pressures also exist as other specialty insurers seek turf expansion; however, RLI's entrenched relationships with broker networks and MGA agreements provide barriers against easy entry. Regulatory evolution affecting non-admitted lines could pose constraints but currently poses limited direct threat given RLI’s geographic diversification [S5].

Near-Term Outlook: Key Milestones and Market Signals to Monitor

Key near-term indicators include examination of upcoming quarterly earnings releases for signs of stabilization or improvement in combined ratios and overall underwriting profitability [S2][N2]. Management has flagged ambitions around premium growth acceleration driven by recalibrated pricing strategies applied during late 2025 — their implementation effectiveness will be closely watched.

Reinsurance program refinements announced recently constitute another execution point—program terms influence loss absorption capacity directly impacting net margins [S3]. Expense management initiatives aiming to optimize operational leverage while supporting targeted growth spurts will also merit investor attention.

Lastly, selective expansion into new specialized coverages or augmentations of existing product suites via MGAs represent strategic levers capable of incremental premium base enhancements as market conditions permit without sacrificing discipline.

Financial Profile: Liquidity, Profitability, and Capital Allocation

Financially, RLI demonstrates strong capital adequacy supported by conservative leverage metrics resembling specialty insurer best practices. As of Q1 2026 end-period data indicates total debt near $297 million against cash and equivalents above $723 million per [F1], yielding a net cash position that enhances balance-sheet flexibility.

Historically the firm exhibits compound annual top-line growth north of 6%, reaching nearly $1.88 billion in revenue for FY2025 with net income increasing approximately 16.6% YoY to over $403 million [F1]. Operating cash flow generation has been robust as well—exceeding $614 million last fiscal year—supporting both sustained dividend distributions ($241.6 million in FY2025) and manageable capital expenditures amounting roughly to $5.5 million annually.

Return on equity sits near a healthy ~22.7%, reflecting effective capital deployment amid moderate cyclicality in underwriting results [F1]. The firm’s capital allocation philosophy prioritizes steady dividends supplemented occasionally by share repurchase programs historically executed more opportunistically than systematically [S11][S12].

Historical performance (annual)

|

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1882 | 403 | 614 | 6 | +6.3% | +16.6% |

| 2024 | 1770 | 346 | 560 | 5 | +17.1% | +13.5% |

| 2023 | 1512 | 305 | 464 | 6 | -11.0% | -47.8% |

| 2022 | 1698 | 583 | 250 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 242 | 609 | 22.7 |

| 2024 | 236 | 556 | 22.7 |

| 2023 | 140 | 458 | 21.5 |

| 2022 | 365 | 245 | 49.6 |

Source: SEC companyfacts cache [F1].

These financial hallmarks underscore firm resilience amidst episodic underwriting pressures while maintaining capital buffer for market contingencies.

This analysis draws exclusively from the latest SEC filings as of April 24, 2026 ([S2], [S3], [S1]) and recent supporting financial data ([F1]), alongside contemporaneous market commentary ([N2], [N3], [N13]). The information herein is presented solely for informational purposes without any investment recommendation or advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments