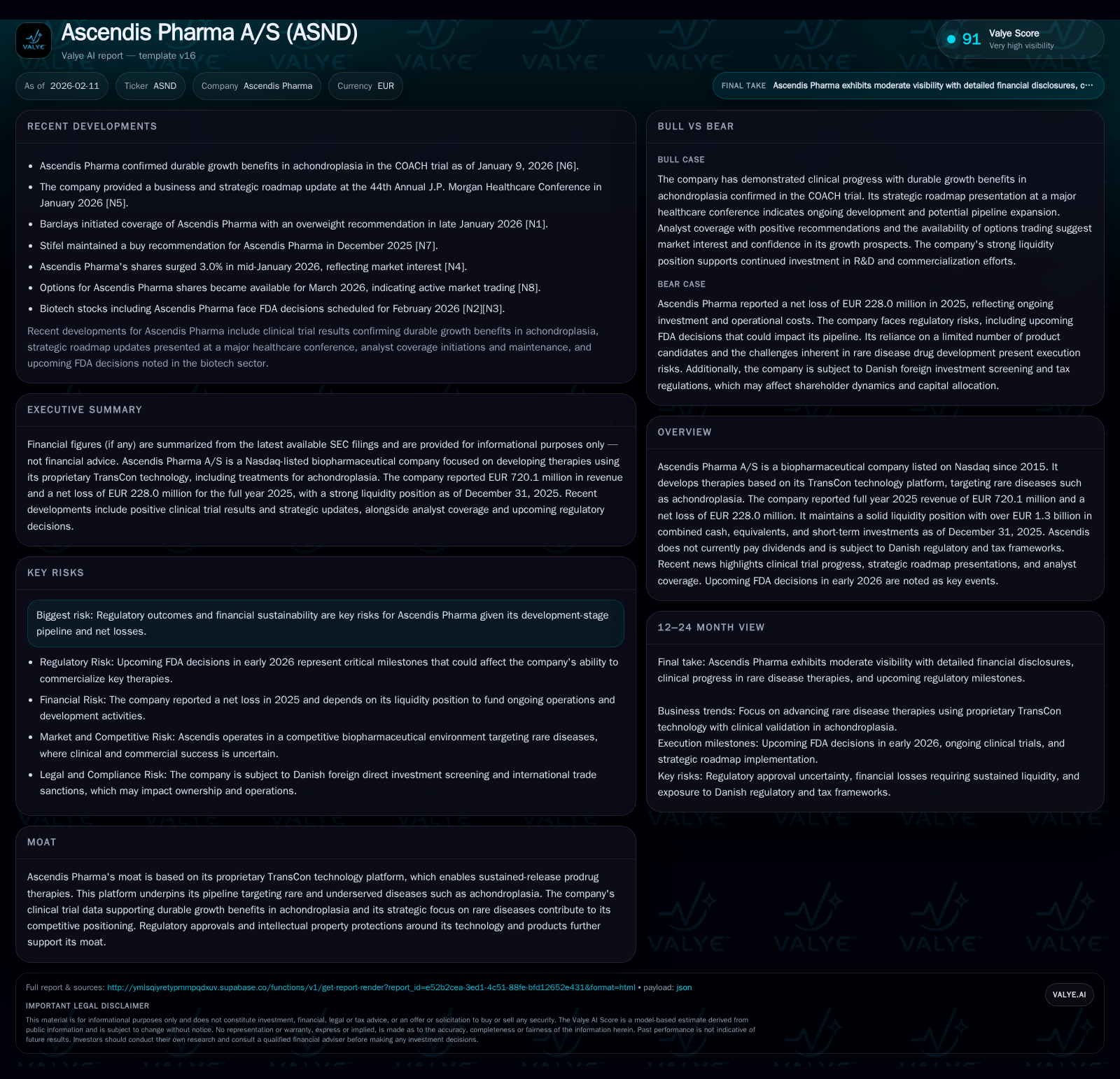

Ascendis Pharma's TransCon Platform Drives Rare Disease Progress Amid Financial Challenges

A deep dive into Ascendis Pharma’s 2025 performance, proprietary technology, pipeline, and looming regulatory catalysts.

In 2025, Ascendis Pharma more than doubled its revenue primarily through expanded sales of YORVIPATH, signaling a shift from pipeline promise to commercial execution despite continued net losses. The company’s distinctive TransCon technology platform remains the core competitive moat underpinning its rare disease focus, including achondroplasia. Key FDA decisions anticipated in early 2026 stand as pivotal inflection points for validating pipeline assets and shaping investor sentiment. While liquidity remains robust with over €1.3 billion in cash and equivalents, managing operational expenses and regulatory uncertainties will be critical for sustainable growth.

From Pipeline Potential to Commercial Reality: Navigating 2025 Performance

Ascendis Pharma’s full-year 2025 results underscore a pivotal transition phase as the company converts its developmental promise into tangible commercial traction. Revenue soared to approximately €720 million—more than double the prior year—primarily fueled by global sales of its lead commercial product, YORVIPATH®, which jumped from around €29 million in 2024 to over €477 million in 2025 (F1, S1). The commercial launch momentum evidences successful market penetration in achondroplasia treatment.

Despite this top-line leap, Ascendis persisted with a net loss of €228 million during 2025 (down from a deeper €378 million deficit in 2024), reflecting ongoing significant investment in research and development alongside elevated commercial expenses supporting market expansion (F1). Operating loss narrowed substantially to approximately €136 million compared to last year’s near €279 million, signaling improved operational leverage amid scaling activities (S1).

Improved cash flow generation is notable as well; operating cash inflows swung positively by over €360 million relative to the prior year step-down driven by higher earnings before non-cash items signifying progress towards operational sustainability (S1). The results depict a company maturing beyond extensive R&D stages into commercialization yet still navigating cost structures typical for biotech firms heavily invested in late-stage development.

Foreign currency translation effects mildly dampened reported revenue by nearly €39 million yet offered partial relief on operating expenses—nonetheless these currency volatilities do not obscure the robust underlying growth trajectory anchored by product adoption (S1).

TransCon Technology: The Moat Behind Rare Disease Therapies

The cornerstone of Ascendis Pharma’s differentiation lies in its proprietary TransCon technology platform — a sustained-release prodrug system engineered to provide durable therapeutic exposure while improving dosing convenience (valye_report_excerpt). This platform delivers extended control of drug release kinetics which is crucial for chronic rare diseases such as achondroplasia where steady systemic drug levels can translate into sustained clinical benefits.

Ongoing clinical programs and intellectual property protections around TransCon bolster competitive barriers protecting against generic or alternative formulations. The durability signal recently reinforced by COACH trial data for achondroplasia provides empirical validation for the platform's unique value proposition in delivering meaningful patient outcomes over time (N6).

Beyond achondroplasia, TransCon serves as a vehicle for addressing unmet needs within endocrine rare diseases and other niche indications — enhancing the strategic rationale for diversified pipeline assets built around this technology backbone. Regulatory approvals tied to TransCon-enabled products further entrench the moat through exclusivity periods common in orphan drug designations (valye_report_excerpt).

YORVIPATH and SKYTROFA: Commercial Drivers and Market Traction

YORVIPATH®, Ascendis’ flagship commercial offering targeting achondroplasia, emerged as the primary revenue engine in 2025. The steep increase — from roughly €29 million to nearly half a billion euros — signifies growing clinician acceptance and patient access globally (F1). This expansion coincides with COACH trial results confirming durable growth benefits reinforcing provider confidence and driving prescription volumes upward (N6).

Meanwhile, SKYTROFA® has maintained steady revenue contribution around €206 million—a modest lift over prior year levels—reflecting its established presence in growth hormone deficiency treatment markets (F1). Both products benefit from differentiated dosing regimens leveraging TransCon to improve patient adherence and outcomes relative to legacy therapies.

Commercial efforts including inventory buildup and supply chain optimization underpin this scaling success, although cost of sales rose accordingly by nearly €51 million amid heightened sales volume and strategic collaborations costs (S1). The combined commercial portfolio thus anchors Ascendis’ expanding revenue base but also shapes its near-term cost dynamics.

Strategic Blueprint Unveiled at J.P. Morgan Healthcare Conference

At the January 2026 J.P. Morgan Healthcare Conference, Ascendis articulated clear forward-looking plans emphasizing three strategic pillars: accelerating clinical development efforts primarily focused on late-stage rare disease candidates; expanding geographic reach especially into underserved international markets; and actively pursuing partnership opportunities to leverage external capabilities while managing capital efficiently (N1).

This roadmap aligns with recent operational performance improvements while signaling management’s intent to buttress commercial scale via both organic expansion and strategic collaboration. Geographic rollout ambitions aim at consolidating footholds established during product launches while future pipeline assets potentially benefit from shared risk partnering models typical within biopharma innovation ecosystems.

These strategic elements contextualize Ascendis’ ongoing investments against a backdrop of anticipated FDA decision milestones that could unlock new approvals or label expansions.

Regulatory Crossroads: Anticipating the February FDA Decisions

Looking ahead, February 2026 represents an inflection point marked by several pending FDA decisions related to Ascendis’ pipeline assets (N3, N4). Such regulatory outcomes carry substantial weight considering the company remains unprofitable overall and depends critically on successful product approvals to justify extensive R&D spending.

FDA verdicts will influence market access timelines directly impacting eventual revenue streams while shaping investor confidence amidst prevailing losses. Historically, biotech stocks face notable volatility surrounding these announcements given their binary nature—approval can propel valuation inflections upward whereas delays or rejections may heighten uncertainty (valye_report_excerpt).

Ascendis’ approach involves proactive engagement with regulators combined with robust clinical data submissions leveraging TransCon-enabled differentiation factors aiming to mitigate risk but inherent unknowns remain. Ultimately, these regulatory gateways serve as catalysts defining the transition from advanced development toward fully commercialized status across pipeline compounds.

Analyst Outlook and Market Sentiment Shifts

Market analysts have started revising views on Ascendis amidst clearer signs of maturation bolstered by rising revenues and clinical validation milestones. A recent initiation of coverage by Barclays with an Overweight rating exemplifies increased institutional optimism predicated on improving fundamentals including progressive revenue growth, manageable losses narrowing faster than feared, and positive clinical updates supporting pipeline prospects (N2).

Short-term share price rallies witnessed post-earnings announcements reflect this sentiment uplift although structural challenges remain evident given free cash flow deficits persist alongside regulatory dependency profiles (N5). Analyst rationale integrates balanced assessment acknowledging upside potential tempered by execution risks inherent in pioneering rare disease therapeutics.

Investor dialogue increasingly incorporates discussions about scalability of TransCon-based franchises alongside evolving competitive landscapes particularly regarding market positioning against established biologics or novel entrants.

Financial Health Dive: Liquidity, Operating Results, and Risk Factors

Ascendis concluded 2025 with combined liquidity—cash, cash equivalents plus short-term investments—exceeding €1.3 billion (€616 million cash alone) supporting runway for innovation-heavy biopharma ventures requiring sustained capital infusion before tipping into consistent profitability (F1, S1). Current ratio stands near adequacy at approximately 1.04 indicating balanced short-term asset-liability positioning.

Operating expenses nearing €761 million reflect heavy R&D spending including clinical trials and pre-commercial manufacturing costs alongside SG&A expense inflation linked to global sales force expansion (S1). Convertible debt instruments figure prominently within capital structure adding complexity around financial leverage though no immediate covenant restrictions constrain operations currently.

Management highlights foreign exchange fluctuations mainly versus USD impart moderate earnings variability but opts not to hedge systematically exposing reported figures to periodic currency translation adjustments (S1). Risks enumerated prominently focus on regulatory approvals' unpredictability—as failure or delay could exacerbate losses—and achieving eventual sustainable profitability amidst market competition remains open questions given current loss trajectories.

Balancing Innovation and Sustainability in Rare Disease Spaces

Ascendis Pharma exemplifies the quintessential biopharmaceutical challenge: striving for transformative innovation within orphan diseases while wrestling with the economics imposed by costly clinical development cycles and complex reimbursement landscapes (valye_report_excerpt).

The company’s mission anchored on the TransCon technology represents an ambitious attempt at redefining therapeutic delivery paradigms addressing unmet medical needs where few competitors venture due to scientific or market constraints.

Nonetheless, translating leading science into robust financial health mandates rigorous execution extending beyond scientific milestones—including strategic partnerships, prudent capital deployment, geographic diversification, coupled with keen management of operational burn rates highlighted throughout its recent public disclosures.

Stakeholders must weigh potential long-term value creation rooted in newly established commercial footholds like YORVIPATH against persistent challenges endemic to emerging biotech: regulatory hurdles still looming large; sizable investment requirements; evolving competition; plus uncertainties around pricing dynamics within rare disease segments where healthcare payers increasingly scrutinize cost efficacy.

Ascendis’ evolution throughout 2025 illustrates forward motion along this demanding path propelled chiefly by differentiated technology coupled with growing market validation but leaves room for cautious monitoring as upcoming FDA verdicts loom large as future determinants shaping trajectory beyond early commercialization phases.

This analysis synthesizes publicly available information without providing investment recommendations. Readers should consider individual circumstances before considering implications related to Ascendis Pharma A/S or similar companies.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments