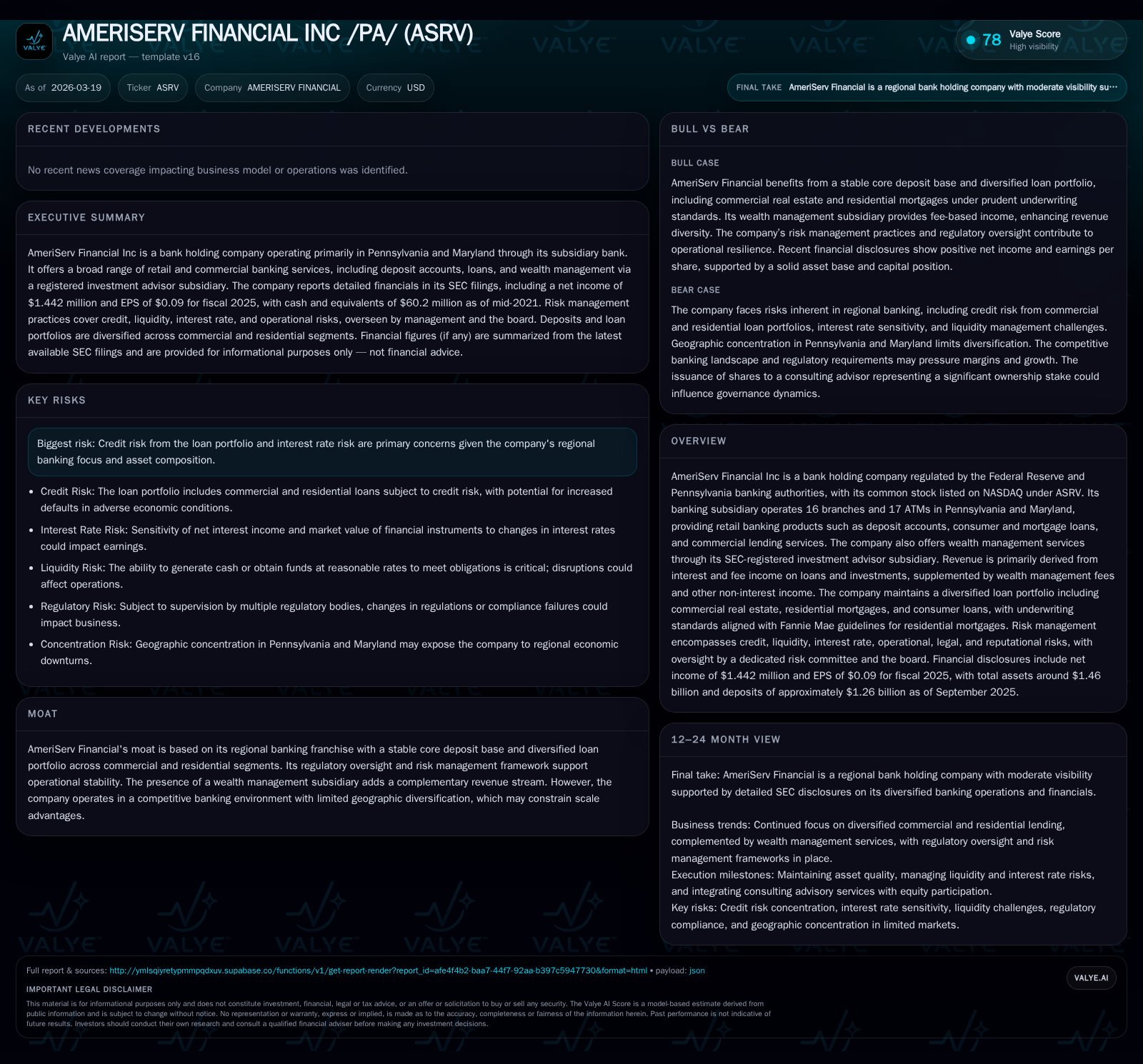

AmeriServ Financial’s Path From Regional Stability to Growth Challenges

AmeriServ Financial has rebounded into profitability after recent losses, balancing its regional franchise strengths with capital discipline amid competitive and regulatory constraints.

AmeriServ Financial emerged from a significant net loss in 2023 to post positive earnings growth in 2024 and 2025, reflecting operational stabilization and prudent risk management within its Pennsylvania and Maryland markets. The company’s diversified loan portfolio spans commercial real estate, residential mortgages adhering to Fannie Mae guidelines, and consumer loans, but is constrained by geographic concentration risks and regulatory scrutiny of commercial real estate exposure. Capital allocation has prioritized steady dividends and modest buybacks while maintaining a conservative liquidity profile governed by its asset/liability management policies. Looking ahead, growth may hinge on loan portfolio diversification and increased wealth management fee income, but remains limited by scale and regional competition.

History of Growth and Profitability Fluctuations

AmeriServ Financial's financial trajectory over the past four fiscal years illustrates a notable recovery arc marked by volatility tied to market conditions and portfolio composition shifts. In FY2023, AmeriServ reported a substantial net loss of $5.3 million after posting modest net gains just prior (around $947 thousand in FY2022) [F1]. This loss reflected pressure on earnings potentially linked to loan performance or market disruptions impacting interest income and credit costs.

However, by FY2024 the company returned to profitability with net income of $889 thousand, advancing further to $1.44 million in FY2025, representing a robust 62.2% increase year-over-year [F1]. Operating cash flow followed a somewhat different pattern; it peaked at $6.3 million in FY2023 before settling near $3.2 million in FY2025 after declining from the elevated prior-year level [F1]. This divergence suggests episodic cash inflows or working capital adjustments related to loan repayments or securities sales.

Meanwhile, shareholders' equity grew steadily from $106 million at end-FY2022 to approximately $119 million by end-FY2025 [F1], underpinning regulatory capital requirements amid enhanced supervisory scrutiny, especially linked to commercial real estate concentrations [S4]. Dividend payments exhibited consistency around two million dollars annually despite earnings fluctuation, signaling disciplined capital policy focused on shareholder returns without undue strain [F1]. Buyback activity was minimal but resumed modestly ($1.5 million) mainly in FY2024 after a long gap since earlier repurchases [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 1 | 3 | +62.2% |

| 2024 | 1 | 3 | +116.7% |

| 2023 | -5 | 6 | -661.9% |

| 2022 | 1 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 2 | 1.2 |

| 2024 | 2 | 0.8 |

| 2023 | 2 | -5.2 |

| 2022 | 2 | 0.9 |

Source: SEC companyfacts cache [F1].

All figures sourced from [F1]

Loan Portfolio Composition and Regional Market Dynamics

AmeriServ’s loan portfolio is distinctly diversified across three principal categories: commercial loans (both owner-occupied and non-owner-occupied commercial real estate), residential mortgages subject to Fannie Mae underwriting standards, and consumer installment loans—including home equity loan products [S5][S6].

The emphasis on commercial real estate lending reflects AmeriServ’s regional franchise strategy operating primarily within Pennsylvania and Maryland’s localized economies [S18]. This geographic focus shapes both opportunity and constraint: while broad familiarity with local market dynamics supports underwriting precision and deposit stability, it narrows scale economies and amplifies concentration risk.

Commercial loans secured by non-owner occupied properties underscore this positioning; these include acquisition/construction of investment properties across retail facilities, multi-family housing units, and other commercial types [S6][S7]. Underwriting adheres to internal Credit Policies regulating maximum amortization periods, debt service coverage ratios (which traditionally set minimum thresholds for sustainable cash flow relative to debt obligations), leasing status requirements for investment properties, as well as prevailing loan-to-value caps aligned with industry norms [S7]. Personal guarantees remain customizable based on borrower creditworthiness but are common particularly where higher-risk speculation exists.

For residential mortgage lending—primarily conforming to Fannie Mae criteria—the bank focuses on performing originations that can be sold or retained selectively as adjustable-rate mortgages or specialized construction loans [S6].[S7] The consumer loan segment complements this with installment loans secured often against residential collateral but is also exposed materially to economic cycles given borrower credit sensitivity [S6].

Local market competition constrains aggressive expansion; new loan production faces headwinds from limited borrower pools within AmeriServ’s footprint as well as pricing pressures inherent among community bank competitors clustering deposit-gathering efforts regionally.

Risk Management Framework in Context of Commercial Real Estate Exposure

Risk management at AmeriServ integrates comprehensive controls overseen by a Management Enterprise Risk Committee which includes board-level representation ensuring governance over credit risk, interest rate sensitivity, liquidity adequacy, operational contingencies, legal compliance, strategic positioning, reputational safeguards, and cybersecurity protocols [S4]. The risk agenda reports formally at least biannually to the Board.

Credit underwriting processes apply rigorous discipline around portfolio composition focusing notably on commercial real estate exposure which constitutes approximately half or more of total regulatory capital allocations per recent filings—non-owner occupied CRE alone accounted for about 352% of regulatory capital at end-FY2025 but declined from the previous year due to portfolio contraction alongside rising capital buffers [S7][S13].

In managing interest rate risk—a critical factor given variable repricing schedules among assets/liabilities—the company employs an Asset/Liability Management Policy that continuously monitors net interest income sensitivity scenarios alongside duration targeting within its investment securities portfolio (aiming for durations under five years) [S4][S6]. Liquidity risk is similarly addressed using contingency funding plans calibrated for cash flow sufficiency amid stressed environments affecting depositors or credit borrowers alike.

Commercial real estate loans undergo intense ongoing scrutiny through semi-annual stress testing evaluating shifts in debt service coverage ratios driven by tenant occupancy changes or collateral value impairments plus trend analysis identifying emerging underwriting risks before deterioration materializes [S7][S12]. These metrics support proactive adjustments to underwriting criteria or lending strategies enhancing resilience against economic downturns predominant in property sectors.

Future Growth Drivers and Headwinds in the Pennsylvania and Maryland Markets

Prospective drivers for AmeriServ hinge on leveraging its stable deposit franchise base combined with gradual expansion into complementary revenue streams such as wealth management fees generated by its SEC-registered subsidiary administering approximately $2.7 billion of client assets outside the company balance sheet [S18][S24]. This division specializes in personal trusts, retirement plans including defined contribution products like IRAs/401(k)s; their revenue is less sensitive to interest rate fluctuations compared to traditional banking operations.

Loan growth potential remains tethered substantially to controlled regional economic conditions supporting commercial real estate demand alongside prudent consumer credit origination tailored to local borrower profiles with reliable cash flow capacity assessed via debt service coverage tests [S5][S6]. However geographic concentration limits scale benefits typical of larger banks’ market diversity while regional competition intensifies pressures on pricing margins.

Regulatory considerations compound these external challenges; heightened supervisory oversight specifically addressing CRE exposure forces incremental costs through risk management enhancements coupled with possible limitations on speculative CRE lending mandates that restrict accelerated asset growth or force deleveraging when concentrations approach regulatory thresholds [S12][S13]. These factors collectively dampen prospects for rapid top-line scaling absent strategic diversification beyond core geographies.

Capital Structure, Liquidity, and Regulatory Considerations

AmeriServ maintains a conservative capital framework oriented toward regulatory compliance defined by supervision from both the Federal Reserve Bank of Philadelphia and Pennsylvania Department of Banking Securities under state-charter mechanisms applicable to its banking subsidiary [S18]. Total assets stood near $1.45 billion with investments comprising high-quality agency mortgage-backed securities plus corporate/municipal holdings managed within duration & credit parameters outlined in formal Investment Policy guidelines restricting exposure levels and credit risk assumptions [S6][S12].

Liquidity resources are robust with cash equivalents reported historically at approximately $60 million mid-2021 aligning with internal contingency funding plans designed for flexibility during deposit demands or sudden loan draw requests [F1][S4]. The company’s asset leverage ratio measured around 9.32%, indicative of typical moderate leverage consistent with regional bank peers adopting prudent balance sheet leverage amid volatile macro environments [S4].

Debt maturities include subordinated notes along with short-term borrowings structured prudently excluding reliance on wholesale funding vulnerable to market shocks; hedging instruments such as interest rate swaps accompany these positions mitigating repricing gaps affecting net interest margins per Asset/Liability Management protocols [S4][S7].

Regulatory monitoring exerts influence through mandated stress tests around CRE portfolios forcing elevated allowances for credit losses when warranted plus strict capital buffer maintenance constraining aggressive dividend hikes or large-scale share repurchases beyond measured levels observed historically [F1][S12].

Returns to Shareholders: Dividends, Buybacks, and ROE Analysis

Despite recent earnings fluctuations including the large loss recorded in FY2023, AmeriServ preserved a relatively stable dividend policy distributing close to $2 million annually throughout FY2022–FY2025 period denoted by actual payments between $1.98 million to just above $2 million per annum without suspension or cuts even during lean earnings cycles [F1].

Buyback activities were dormant until intermittent repurchase programs restarted modestly during FY2024 totaling approximately $1.5 million worth of stock retirements; this conservative approach aligns with balancing capital return preferences against maintaining ample buffer for future uncertainties especially influenced by regulatory caution over CRE concentration risks discussed previously [F1].

Measured against equity base near $119 million as of end-FY25,the company's approximate return on equity stands low near 1.2%, reflecting subdued profitability relative to typical community banking benchmarks which often target mid-single digit ROEs under normalized economic conditions.[F1]

This low ROE further underscores challenges stemming from heightened reserve provisioning needs amid commercial property sector risk perceptions alongside limited top-line growth opportunities constraining earnings leverage.

What to Watch: Indicators for AmeriServ’s Forward Momentum

Absent explicit forward guidance disclosures, key indicators warranting close monitoring include segmented loan growth rates particularly within commercial versus residential categories given differential underwriting risk profiles tied directly to local economic vitality.

Also critical is tracking momentum within non-interest income streams principally wealth management fees benefiting from expansion or retention gains inside stewardship assets approximating nearly three billion dollars providing fee diversification beyond traditional lending spreads.

Additional vigilance over evolving credit quality trends via allowance for credit losses adjustments combined with metrics such as impaired loans ratios—especially surrounding CRE subsets—will signal emerging pockets of portfolio strain amid tightening monetary policy cycles or regional downturns.

Finally,the firm’s investment security valuations tied to duration targets alongside effectiveness of interest rate hedge strategy will impact net interest margin sustainability thus profitability trajectory into coming fiscal periods.

This report is based exclusively on publicly available company filings as detailed herein along with reasoned analysis derived therefrom; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments