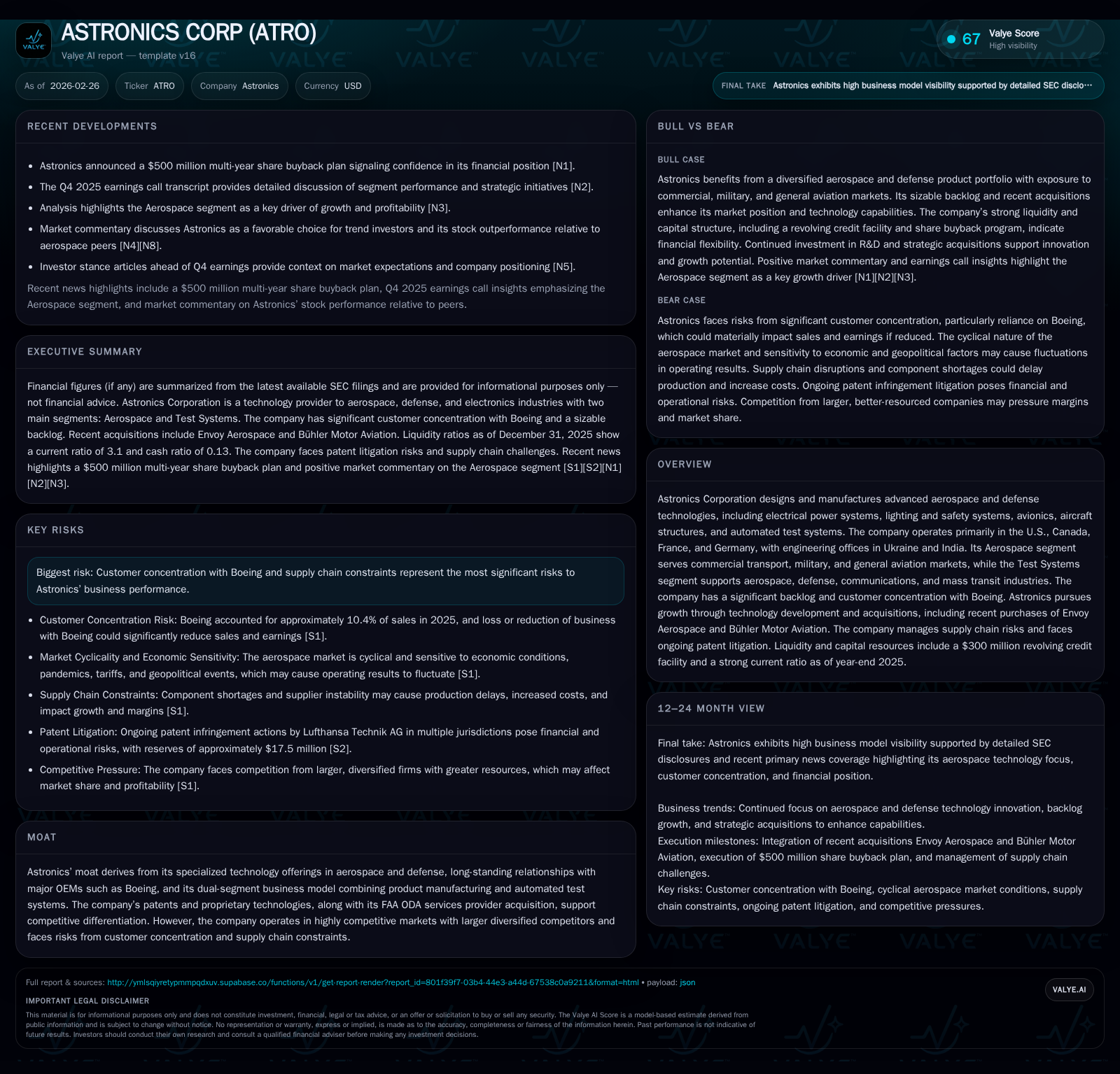

Astronics Corp: Rebounding Operating Income and Strategic Acquisitions Drive 2025 Momentum

Astronics delivered a significant operating income turnaround in 2025, bolstered by key acquisitions and operational improvements amid aerospace sector challenges.

After facing losses in 2022 and 2023, Astronics Corporation dramatically reversed its financial performance in 2025 with an operating income increase of nearly 189% year-over-year. This rebound was supported by strengthened aerospace segment demand, strategic acquisitions including Envoy Aerospace and Bühler Motor Aviation, and improved cash flows. While the company benefits from a solid technological moat centered on specialized aerospace products and test systems, risks remain from Boeing customer concentration and supply chain constraints. Capital allocation has been conservative with a focus on buybacks rather than dividends, and R&D spending remains a core driver for sustaining competitive advantage.

Financial Turnaround: From Losses to Profitability in 2025

Astronics exhibited a remarkable financial recovery in fiscal year 2025 following operational challenges earlier in the decade. After recording operating losses of approximately $30 million and $6.7 million in 2022 and 2023 respectively, the company posted operating income of $26.5 million in 2024 before surging to $76.4 million in 2025—a nearly 189% year-over-year increase [F1]. This positive shift also extended to net income where Astronics swung from a $2.8 million loss in 2024 to a net profit of $29.6 million in the latest year. Operating cash flow followed suit, climbing by approximately 145% to nearly $75 million, supporting robust liquidity and investment capacity.

The turnaround stems primarily from improving sales volumes within its Aerospace segment fueled by recovering demand from commercial transport aircraft OEMs and operational efficiencies obtained through ongoing simplification initiatives implemented during the year [S1],[N1]. Reduced restructuring costs compared to prior periods along with streamlined footprint rationalization efforts helped stabilize margins amid inflationary pressures.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 30 | 75 | 76 | +1145.7% |

| 2024 | -3 | 31 | 26 | -140.6% |

| 2023 | 7 | -24 | -7 | +202.9% |

| 2022 | -7 | -28 | -30 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 21.1 |

| 2024 | -1.1 |

| 2023 | 2.8 |

| 2022 | -2.8 |

Source: SEC companyfacts cache [F1].

Table shows Astronics’ fiscal year performance highlighting operating income surge and improving cash flows according to latest data [F1]

Segment Revenue Drivers: Aerospace Leads with Diverse Market Exposure

Astronics operates via two principal segments: Aerospace and Test Systems [S6]. The Aerospace business contributes overwhelmingly to consolidated revenue—approximately three-quarters of total sales—with its product portfolio spanning power generation/distribution systems to avionics and safety lighting tailored for commercial transport aircraft chiefly served through OEM contracts with major players like Boeing [S5],[S6]. Within this segment's revenues in 2025 were split roughly as: commercial transport at ~75%, military aircraft ~15%, general aviation ~9%, with minimal sales classified under other categories.

The Test Systems segment complements Aerospace by delivering automated testing solutions that support aerospace & defense manufacturers plus communications and mass transit sectors worldwide. This division often engages large multi-year contracts primarily involving prime government contractors or global OEM customers for test platforms essential throughout manufacturing lifecycle stages including post-production validation [S5],[N8].

The commercial transport market exposure provides Astronics with scale benefits from the duopoly structure dominated by Boeing and Airbus OEMs; however the company’s reliance on Boeing constitutes a notable concentration risk accounting for just over ten percent of annual revenue as of recent years [S21],[S22].

Strategic Acquisitions Strengthening Technological Moat

In alignment with its strategy to augment internal capabilities through complementary acquisitions, Astronics added key aerospace-focused assets during mid-to-late 2025. The purchase of Envoy Aerospace provided direct access to FAA Organization Designation Authorization (ODA) services—critical certification authority enabling faster aircraft system approvals—thereby enhancing Astronics' service spectrum for aerospace customers navigating stringent regulatory pathways [S5]. The acquisition cost was about $8.3 million considering milestone payouts spread over two years.

Subsequent acquisition of Bühler Motor Aviation expanded Astronics’ electrical power system expertise particularly relevant for next-generation aircraft platforms requiring sophisticated motion control technologies [S6]. These buyouts effectively deepen Astronics’ technological moat by incorporating niche yet strategically vital competencies that bolster competitive differentiation against larger diversified rivals.

Integrating these entities is expected not only to diversify revenue streams but also accelerate new product certifications leveraging Envoy’s unique FAA regulatory standing—an asset increasingly valued as airlines upgrade fleets under evolving compliance regimes.

Supply Chain and Customer Concentration: Assessing Key Risks

Astronics’ growth trajectory is moderated by tangible risks centered on supply chain constraints and customer concentration vulnerabilities [S14],[N1]. Dependency on Boeing represents one primary source of earnings volatility; single-customer revenue consistently near or just above the ten percent threshold equates to material business sensitivity should Boeing’s delivery schedules fluctuate or program investments adjust downward due to macroeconomic or production challenges [S26],[S11].

Supply chain issues remain pervasive across aerospace manufacturing globally—ranging from semiconductor shortages to raw material delays—which elongate production cycle times for electric power modules or avionics kits offered by Astronics’ Aerospace segment. Such bottlenecks elevate costs potentially suppressing margin expansion despite higher order backlogs reported at nearly $675 million at year-end ’25 up from $599 million twelve months prior signaling sustained inbound demand albeit not risk-free [S15].

Additionally the Test Systems segment encounters concentrated customer exposures typical within defense contract environments where fewer prime contractors dominate procurement pipelines posing similar demand uncertainty risks [S8].

Capital Structure, Liquidity, and Debt Management Insights

Astronics prudently restructured its debt profile recently optimizing liquidity amid capital needs generated by both organic growth initiatives and acquisitions. A significant change occurred October ’25 when the Company terminated its asset-based lending revolving credit facility (“ABL”) replacing it with a cash flow-based revolving credit facility capped at approximately $300 million priced at SOFR plus applicable margins reflective of excess availability metrics [S4],[S7].[S9]

Convertible senior notes further define Astronics’ long-term debt strategy: the $165 million of notes due in 2030 saw repurchases reducing outstanding amounts to roughly $33 million post refinancings whereas issuance of $225 million notes due in 2031 injects no interest burden but incorporates capped call transactions mitigating stock dilution risks upon conversion exercises enhancing equity preservation flexibility.

As of December ’25 liquidity stood robustly supported by almost $18.2 million cash equivalents combined with current assets exceeding current liabilities more than threefold yielding a strong current ratio near 3.1x further underlining comfortable short-term financial footing [F1],[S9]. Compliance with loan covenants such as minimum fixed charge coverage ratios remains intact enabling uninterrupted access to credit lines essential for operational continuity.

Capital Allocation: Share Buybacks, Dividends, and Return on Equity

Astronics has historically prioritized balance sheet strength over dividend issuance; no dividends have been paid since at least FY2014 indicating retained earnings are predominantly reinvested into operations or share repurchases rather than distributed [F1]. The company's latest reported return on equity stands around an impressive ~21%, underscoring efficient leveraging of shareholder capital reflecting gains realized from profitability rebounds coupled with modest equity base following share repurchase activity [F1],[S20].

Recently authorized multi-year share buyback programs signal management’s confidence in underlying business fundamentals while providing liquidity management avenues favorably interpreted by investors seeking capital appreciation over yield.

Research & Development and Innovation as Future Growth Catalysts

Maintaining technological relevance is paramount within aerospace manufacturing sectors where rapid advances can swiftly erode competitiveness. Astronics commits significant resources toward R&D efforts accounting for over $50 million annually with a trend toward separating these expenses distinctly below gross profit line item facilitating clearer visibility on innovation spends per regulatory filings updates during early ’25 reporting periods [N11],[S29].

Investment focuses include electrification subsystems modernization aligned with evolving environmental standards alongside continual enhancements to automated test equipment engineered for reliability validation across emerging aerospace applications thus securing intellectual property assets critical for sustainable market access.

Outlook and Indicators to Monitor Beyond Official Guidance

While explicit forward-looking guidance remains limited partially due to inherent unpredictabilities linked with defense contracts timing plus OEM delivery rate fluctuations around Boeing programs analysts are advised to track several key indicators: backlog book-to-bill ratios reflecting order intake health; milestone achievements related to integration outcomes from recent acquisitions impacting operational synergies; supply chain normalizations reducing lead times; contract awards potentially stemming from Department of Defense funding appropriations shaping Test Systems pipeline vitality among others [N2],[N3].

Ongoing vigilance around patent litigation developments especially European actions could influence risk profiles though presently managed rigorously without material near-term cash impacts disclosed[S19],[S26]. Continual monitoring of broader macro factors affecting airline capital expenditures will remain essential given their outsized influence on Astronics’ principal revenue streams.

This analysis synthesizes verified public disclosures without conjecture beyond available facts emphasizing clearer connections between strategic moves and financial outcomes uniquely pertinent for aerospace-specialized manufacturing firms navigating cyclical industry dynamics.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments