From Loan Portfolio Diversity to Capital Returns: Atlantic Union Bankshares’ Pathway to Enhanced Profitability

Atlantic Union’s strategic loan mix and disciplined capital allocation drove a notable net income jump in 2025 while maintaining liquidity and risk controls.

Atlantic Union Bankshares Corp recorded a 30.9% rise in net income in fiscal 2025 compared with 2024, fueled by multi-segment loan diversification and robust operational cash flow growth. Its broad loan portfolio spanning commercial real estate, construction, automobile, and residential loans helped balance credit risks and revenue streams. Capital structure strengthening via equity expansion and limited buybacks positioned the bank for consistent dividend payments and moderate ROE, even as it navigates elevated credit and operational risks. Forward-looking management commentary highlights geographic expansion and interest rate variability as key growth determinants.

Historical Growth Trends and Key Earnings Drivers in 2025

Atlantic Union Bankshares Corp experienced considerable financial momentum during fiscal year 2025. The net income accelerated to $273.7 million, marking a substantial 30.9% increase over the $209.1 million reported in 2024 [F1]. This marked improvement was underpinned by a dramatic surge in operating cash flow, which climbed more than sixfold from $308 million in 2024 to $2.24 billion in 2025, suggesting enhanced core earnings quality and efficiency gains within its banking operations [F1]. An expanded equity base also supported this performance surge, growing approximately 59% year-over-year from $3.14 billion to just over $5 billion [F1].

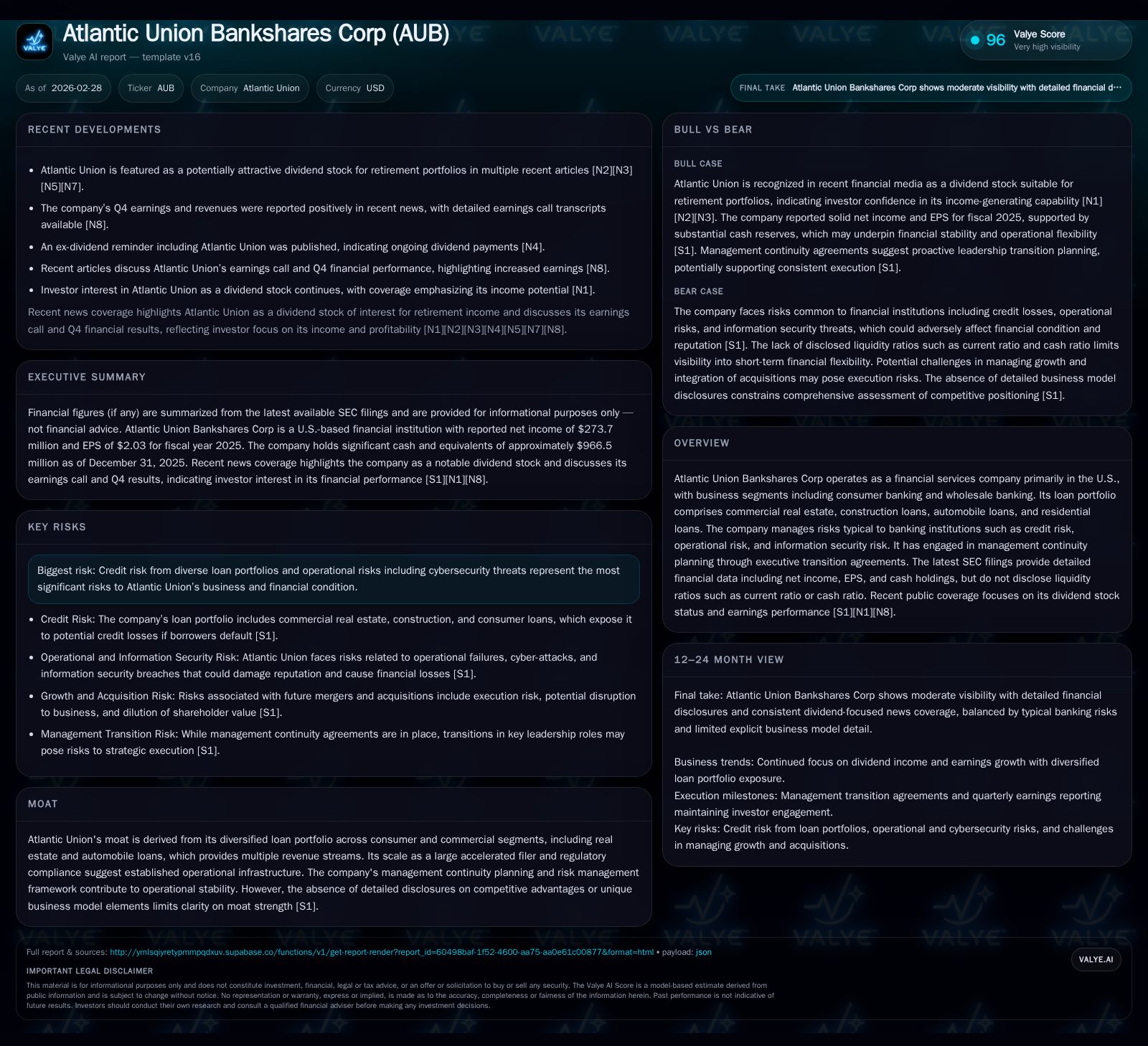

Historical performance (annual)

| FY | Net ($mm) | CFO ($bn) | Net YoY |

|---|---|---|---|

| 2025 | 274 | 2.2 | +30.9% |

| 2024 | 209 | 0.3 | +3.6% |

| 2023 | 202 | 0.3 | -13.9% |

| 2022 | 235 | 0.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 5.5 | |

| 2024 | 0 | 6.7 |

| 2023 | 0 | 7.9 |

| 2022 | 48 | 9.9 |

Source: SEC companyfacts cache [F1].

This blend of rising profitability paired with robust cash flow generation points towards improved net interest margins and fee income contributions driven by the company’s diversified lending approach detailed later. These results come against the backdrop of an environment in which lenders face increasing challenges related to credit risk management and heightened regulatory oversight [S1][N1]. Atlantic Union’s ability to leverage its operational scale following acquisitions appears integral to sustaining such earnings momentum.

Loan Portfolio Composition: Multi-Segment Diversity as a Financial Edge

Atlantic Union’s loan portfolio is notably segmented across various asset classes including commercial real estate (CRE) — subdivided into owner-occupied and non-owner-occupied sectors — construction loans, automobile financing, and multiple residential loan categories [S25][S1]. This heterogeneous credit mix serves as both a revenue stabilizer and mitigant against concentration risk endemic to regional banking institutions.

In particular, commercial real estate lending encompasses owner-occupied properties that tend to carry lower volatility but also serve as collateral anchors; meanwhile, non-owner-occupied CRE exposes the bank to market-driven cyclicality that requires steadfast underwriting vigilance [S25]. Construction loans add another dimension of risk-return tradeoff tied closely to economic development activity. Automobile loans provide consumer-oriented exposure with relatively shorter tenor profiles.

Importantly, the residential loan segment includes both revolving lines (such as HELOCs) and more traditional consumer/mortgage exposures, diversifying asset duration and interest rate sensitivity [S25][S1]. The multi-faceted loan mix not only broadens revenue sources but also fosters incremental cross-selling opportunities across Atlantic Union’s consumer banking and wholesale divisions.

Navigating Credit and Operational Risks in Consumer and Wholesale Banking

Credit risk remains paramount given the composition of Atlantic Union’s lending book [S15][S18]. The bank discloses segmented delinquency statistics including past-due categories (30–59 days, 60–89 days) and loans in nonaccrual status across key segments such as construction, automobile, residential loans, CRE owner/non-owner occupied, commercial & industrial borrowers [S8][S12][S16]. While specific impairment allowances are not itemized here, proactive monitoring frameworks are implicit from disclosures emphasizing model reviews and loss allowance assessments.

On the operational front, Atlantic Union addresses heightened cybersecurity threats as a substantive risk vector that could disrupt business continuity or erode customer trust through data breaches or infrastructure failures [S18]. Complementing these risks are exposures related to technological changes impacting service delivery capabilities alongside compliance with intricate regulatory mandates [S15][S18].

Given these challenges, Atlantic Union's layered risk management protocols targeting both credit underwriting standards and technology defenses are essential pillars supporting sustained franchise integrity.

Capital Structure and Liquidity Position After Recent Acquisitions

The bank's capital resources expanded markedly entering into fiscal year-end 2026 driven by equity growth reflecting recent strategic acquisitions such as Sandy Spring Bancorp [S4][F1]. Total equity nearly reached $5.01 billion at year-end versus roughly $3.14 billion a year prior [F1], enhancing capital adequacy ratios critical for regulatory compliance.

Alongside equity growth, Atlantic Union maintains subordinated debt facilities maturing between 2029 and 2032 that supplement stable funding profiles while preserving capacity for contingency liquidity measures such as repurchase agreements linked to assets pledged as collateral [S5][S6]. Core deposits remain a significant funding base enhancing liquidity resilience despite broader macroeconomic volatilities.

The company’s balance sheet adaptations post-acquisition reinforce its position against stresses while enabling deployment of capital toward organic lending growth initiatives.

Returns to Shareholders: Dividends, Buybacks, and ROE Analysis

Dividend stability has emerged as an important feature of Atlantic Union’s capital strategy, with distributions consistently exceeding $78 million annually over recent years; dividends paid in fiscal 2022 amounted to approximately $86.9 million indicating steady shareholder returns [F1]. Notably absent have been share repurchases since at least fiscal years 2023–24 when buybacks ceased following active repurchase activity up to fiscal 2022 ($48.2 million) and fiscal 2021 ($125 million) [F1].

Calculating return on equity based on disclosed figures yields a moderate figure of roughly 5.5% for fiscal 2025 ($273.7 million net income divided by $5.01 billion equity) [F1]. While this suggests room for efficiency enhancements given the sizeable equity base expansion post-acquisitions, it reflects prudent capital retention supporting growth investments and risk buffers.

Strategic Outlook: Growth Opportunities and Industry Challenges Ahead

Management commentary highlights geographic expansion into North Carolina among key growth avenues leveraging existing platform strengths after recent acquisitions [N1][S20]. Executives caution variability in loan demand tied closely to interest rate environments remains a pivotal factor influencing future net interest margins.

Economic uncertainties including fluctuating real estate values within lending markets present ongoing headwinds alongside competition from fintech entrants reshaping aspects of customer acquisition and service models [S15][N13]. Nevertheless, Atlantic Union aims to capitalize on its diversified product suite targeting both retail consumers and mid-sized businesses seeking tailored financial solutions.

Monitoring Milestones: What Investors Should Watch Next

Key performance indicators warranting close observation include quarterly updates on loan portfolio credit quality metrics such as delinquency rates across classified loan segments [N2][N3]. Additionally, shifts in net interest margins will provide clarity on the impact of monetary policy changes on lending profitability.

Continuing integration outcomes from acquired entities like Sandy Spring stand as operational milestones influencing cost synergies realization alongside strategic market penetration metrics [N13]. Dividend consistency amid evolving economic conditions will also serve as an indicator of financial health.

Disclaimer: This analysis is solely for informational purposes based on available public data including SEC filings (10-K reports), news transcripts, company disclosures, and financial data archives up to date as of February 28, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments