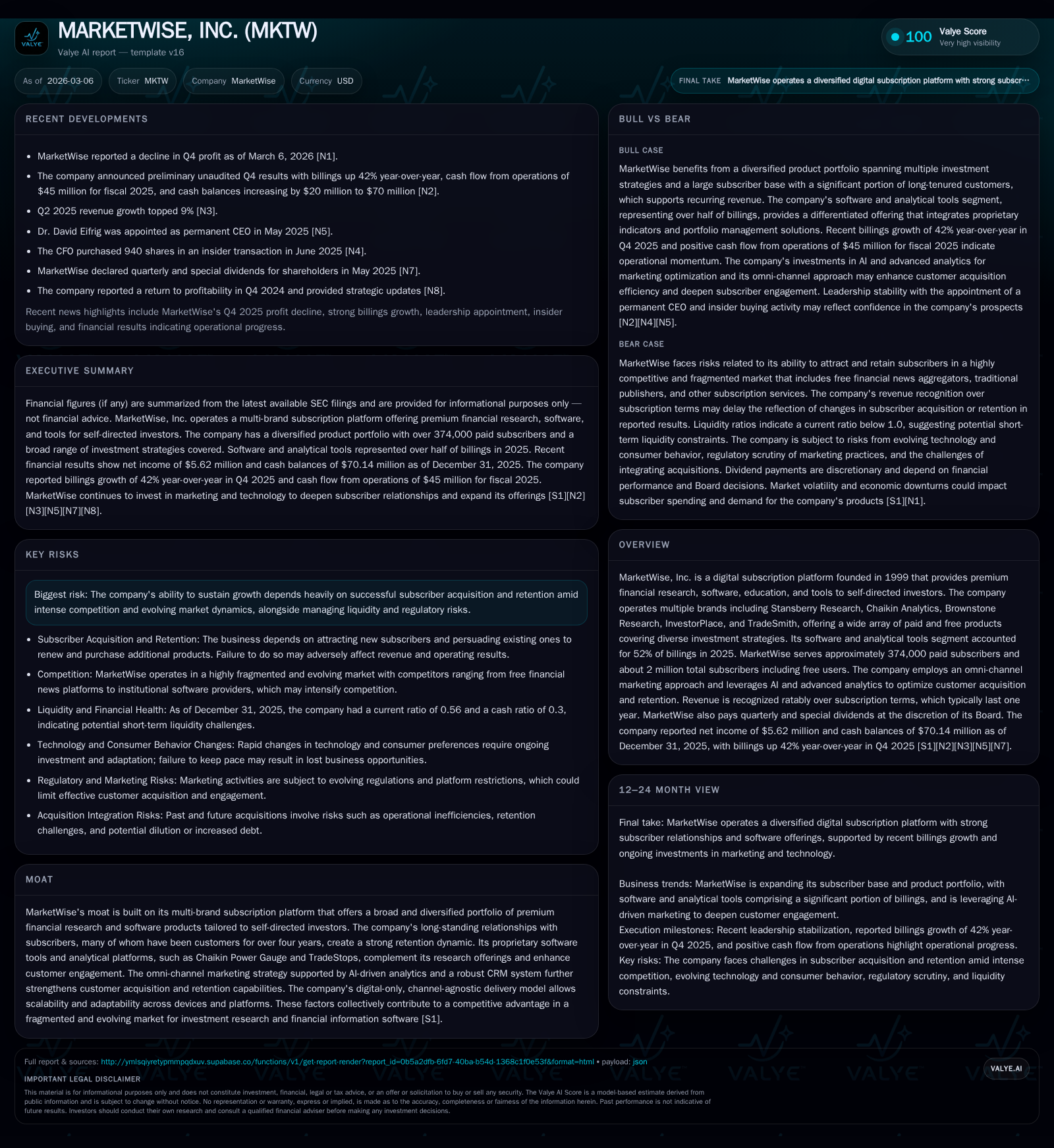

MarketWise Inc. Endures Profit Headwinds While Pursuing Subscription Expansion

Despite revenue and profit contraction, MarketWise grows its subscriber base and strengthens cash flow through technology-enhanced marketing and diversified offerings.

MarketWise’s 2025 results exhibit a paradox of shrinking earnings but robust cash generation amid strategic expansion of its multi-brand subscription ecosystem. The company’s transition towards software and analytical tools now accounts for over half of billings, underscoring its shift to technology-driven solutions for retail investors. While operating income declined nearly 30% in FY2025 due to margin pressures and heightened competition, operating cash flow surged by over 300%, supporting continued dividends and modest buybacks. Persistent legal, regulatory, and market risks, however, temper outlooks despite the company’s AI-powered omni-channel marketing prowess.

Decoding MarketWise’s Historical Growth and Earnings Trajectory

MarketWise operates a complex digital subscription ecosystem servicing self-directed investors since its founding in 1999. Over the last four fiscal years, its revenue has contracted from $549 million in FY2021 to $512 million in FY2022 — a roughly 6.7% decline further reflected in recent quarters [F1]. This downward trend corresponds with intensified competition and pricing pressures documented in their disclosures [S5].

Operating income illustrates notable volatility: after peaking at $89 million in FY2024, it declined sharply by nearly 30% to about $62.6 million in FY2025. Net income fell more modestly but remains positive at $5.6 million for the same fiscal year [F1]. The squeeze on profitability aligns with increased spending on marketing and technology investments designed to support subscriber growth efforts (discussed below).

Notably contrasting these profitability declines is a marked rebound in operating cash flow (OCF), which surged from a negative $22 million in FY2024 to nearly $46 million in FY2025 — a staggering improvement of over 300%. Capital expenditures remain minimal relative to operating costs; this efficient capex spend underpins strong free cash flow generation estimated at approximately $45.6 million post-capex [F1]. This dichotomy between earnings pressure and cash flow strength reflects MarketWise's subscription billing model with ratable revenue recognition tied to contract terms.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 6 | 46 | 63 | 391000 | -20.4% |

| 2024 | 7 | -22 | 89 | 133000 | +296.1% |

| 2023 | 2 | 62 | 52 | 65000 | -90.1% |

| 2022 | 18 | 48 | 87 | 35000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 3 | 46 | -48.1 |

| 2024 | 11 | -22 | -56.3 |

| 2023 | 0 | 62 | -16.1 |

| 2022 | 13 | 48 | -84.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue stable from FY2022 baseline; YoY changes calculated where data available.

Multi-Brand Subscription Dynamics: Revenues, Retention, and Customer Engagement

MarketWise’s business model revolves around an extensive portfolio of distinct financial research brands such as Stansberry Research, Chaikin Analytics, Brownstone Research, InvestorPlace, and TradeSmith [S6]. This multi-brand strategy allows tailored offerings addressing diverse investment strategies ranging from value investing to alternative assets including cryptocurrencies.

The company reported approximately 374,000 paid subscribers out of roughly two million total users including free registrants as of late 2025 [S1]. Free offerings operate as a top-of-funnel customer acquisition channel feeding conversion into paying subscribers through demonstrated content value — a classic free-to-paid subscription funnel common for digital publishing vendors.

Retention strength is a critical competitive moat; more than half the billings in fiscal year 2025 were attributable to subscribers with over four years’ tenure [S7]. This persistent renewal dynamic indicates durable consumer trust built on high-quality independent research coupled with risk-focused contrarian investment philosophies consistent across brands [S15]. Such longevity supports predictable recurring revenues despite churn typical during market volatility.

Cross-selling multiple tiers and product categories within this brand ecosystem fosters a “flywheel effect”: subscribers engage deeply via research newsletters complemented by software tools driving expanded wallet share over time [S6]. These include both educational subscriptions priced around $100 annually as well as premium memberships costing several thousands per annum [S7]. Maintenance fees on membership products add further revenue stability.

Technology as a Differentiator: Advanced Analytics & AI in Marketing

MarketWise leverages proprietary AI-driven analytics combined with cutting-edge CRM platforms to execute a channel-agnostic distribution model optimized for cost-effective subscriber acquisition and retention [S8]. Through continuous performance attribution at granular levels—down to individual marketing advertisements—the company refines its omni-channel marketing mix that includes digital ads, email campaigns, direct mailout programs, and episodic radio/television spots.

Underlying this sophisticated engagement framework are algorithmic portfolio management tools integrated into its Chaikin Analytics suite along with back-tested proprietary algorithms embedded within TradeSmith software solutions [S6]. These functions enhance investor decision-making capabilities while increasing user engagement duration across devices from desktop browsers to mobile tablets.

This investment into AI not only improves lead scoring accuracy but also enables timely customer feedback loops that inform product development cycles — tying innovation tightly to observed consumption patterns [N1][S5]. Such technology initiatives create scalable subscriber touchpoints resilient against shifting platform preferences among retail investors.

Financial Performance Metrics: Understanding Profitability and Cash Flows

Despite positive operating earnings in FY2025 ($62.6 million), MarketWise shows negative shareholders’ equity of roughly -$11.7 million reflecting accumulated deficits or other balance sheet adjustments [F1]. Consequently, trailing ROE calculations appear negative (approximately -48%), stemming from the small net income figure relative to negative equity.

The company maintains relatively lean capital expenditure demands ($391k in FY2025) compared with strong operational cash flow recovering robustly after a trough year (-$22m CFFO in FY2024) [F1]. The resultant free cash flow generation supports discretionary capital returns including quarterly dividends plus special dividends determined by the Board’s discretion [N1][S23].

Liquidity metrics illustrate challenges: current assets ($131 million) fall significantly short of current liabilities ($234 million), resulting in a current ratio near 0.56 [F1]. This leverage may reflect timing differences on payables or obligations linked to subscription billing cycles and requires ongoing monitoring for solvency implications.

Overall capital efficiency appears sound given the platform’s digital nature but balancing cash cycle management alongside earnings compression due to competitive investments will be critical going forward.

Navigating Risks: Competition, Regulatory Scrutiny, and Market Pressures

MarketWise operates within an intensely fragmented industry facing competition from multiple vectors: free online aggregators (Yahoo! Finance), established financial newshouses (WSJ), subscription-focused rivals (The Motley Fool), social media investing communities (X/Twitter), plus institutional-grade software providers like Bloomberg [S16]. Low barriers to entry catalyze ongoing challenger emergence.

Regulatory complexities pose persistent risks tied to compliance with securities laws governing financial publications plus evolving consumer protection rules impacting digital marketing practices including email & SMS communications under TCPA/CAN-SPAM frameworks [S4][S18][S21]. Recent class-action litigations within the sector heighten exposure.

Intellectual property claims alleging infringement or misuse related to proprietary data sources or AI-powered technologies add potential legal contingencies requiring vigilance [S11][S20]. Furthermore, compliance burdens from global regimes such as GDPR increase operational complexity outside North America [S14][S18].

Executives disclose ongoing litigation from former executives seeking damages unrelated directly to operations but potentially distracting management resources [S13]. Ultimately these factors underscore that maintaining consumer trust alongside legal prudence forms an integral element of sustaining long-term earnings.

Capital Deployment: Buybacks, Dividends, and Balance Sheet Health

MarketWise has historically returned capital via both dividends and stock repurchase programs though recent trends reveal moderation:

- Buybacks contracted sharply from $13 million in FY2022 down to about $3.4 million in FY2025,

- Dividend payments continued quarterly plus occasional special dividends as approved by the Board at discretion [F1][N1][S23].

Given net income constraints combined with negative shareholder equity on the balance sheet (-$11.7 million at end-2025), buyback programs have been scaled back reflecting cautious capital stewardship aligned with preserving liquidity amidst profit headwinds.

This conservative capital allocation approach balances rewarding shareholders without exacerbating leverage or restricting operational flexibility amid persistent market uncertainties highlighted earlier.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments