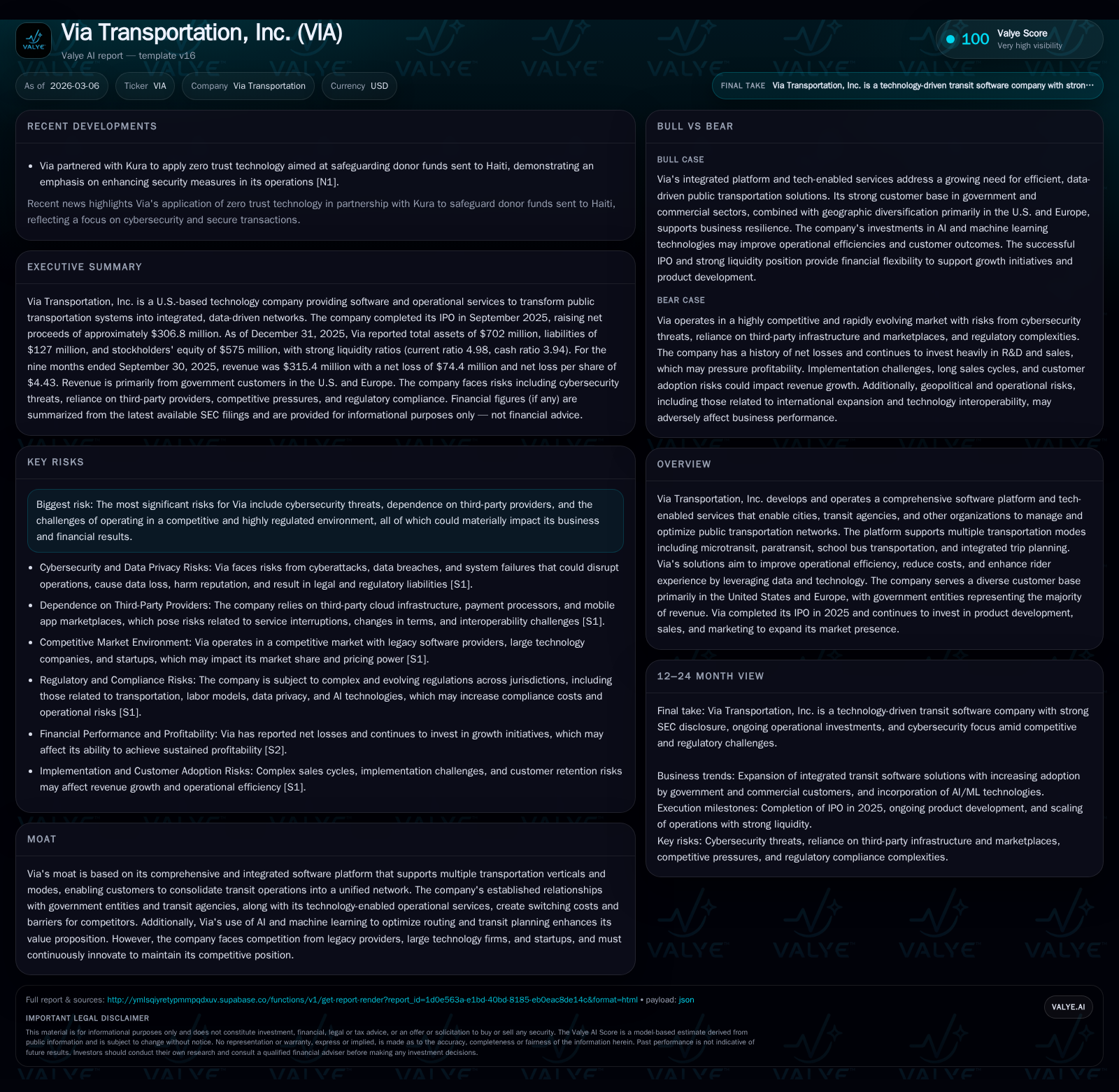

Via Transportation Expands Software Reach Amid Persistent Profit Challenges

Via broadens its integrated transit platform while navigating sustained net losses and complex regulatory dynamics.

Since its IPO in September 2025, Via Transportation has significantly expanded its multi-modal transit software platform, driving considerable revenue growth primarily through government contracts in the US and Europe. However, escalating investment in R&D and sales, alongside regulatory and operational risks, have kept operating income and net profits deeply negative. With a strong cash position supporting product development, Via faces a critical inflection point balancing growth ambitions against profitability challenges amid fierce competition and evolving labor and cybersecurity regulations.

Evolution of Via’s Comprehensive Transit Software: Historical Growth Drivers

Founded in 2012, Via Transportation has emerged as a leading provider of an integrative software platform for public transit agencies globally. Since its IPO in September 2025 [S9],[S3], the company has leveraged its comprehensive suite spanning microtransit — flexible shared rides within defined zones — paratransit services catering to disabled riders, school bus routing solutions, and integrated trip planning to consolidate fragmented legacy transit operations into unified networks. This breadth enables cities and transit agencies to manage diverse transportation modes from a single technology stack.

Via's historical revenue trajectory showcases rapid scaling driven primarily by government contracting. According to recent filings [F1],[S14],[S7], government clients accounted for approximately 94% of total revenue in the first nine months of 2025, reflecting heightened adoption within public-sector entities such as city transit authorities and school districts. The U.S. market dominates with nearly 71% of revenues that period, complemented by European business (26%), chiefly Germany where Via has established notable footholds [S14].

In the first nine months of 2025, Via reported revenues of $315 million — a substantial increase from $246 million during the same period in 2024 — equating to nearly a 28% year-over-year uplift [S7]. This surge aligns closely with newly secured contracts that underpin a remaining performance obligation backlog of $291 million at Q3 2025 [S5], signalling robust forward revenue visibility especially given that roughly two-thirds of this backlog is slated for recognition over the next eighteen months. The company's offerings increasingly exhibit cross-vertical adoption within client bases employing AI-driven algorithms for dynamic fleet routing optimization — a key differentiator enabling cost reductions while enhancing rider experience.

The table below summarizes Via’s recent financial performance based on available data:

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Shifts in Financial Performance and Underlying Cost Dynamics

Despite rapid revenue growth concurrent with scaling contract wins post-IPO [S1],[S2], Via continues to operate at a meaningful net loss level which reached approximately $96 million in fiscal year 2025 [F1]. Operating income remains negative at about -$77 million for the same period. These losses stem largely from heavy reinvestment into platform enhancements including R&D expenditures focused on expanding multi-modal capabilities and integrating advanced AI & machine learning features aimed at optimizing route dispatching algorithms [S2].

Simultaneously, sales and marketing expenses have risen sharply as Via competes aggressively to secure government contracts amid competitive pressures from legacy software vendors like Constellation Software and emerging tech firms such as RideCo [S20]. Amortization expenses related to capitalized commissions also weigh on profitability; they totaled around $3.6 million year-to-date Q3 2025 compared with $4.2 million for all of last year indicating elevated customer acquisition efforts [S5].

Cost structure analysis reveals that despite growing top-line traction via multi-modal platform adoption, operating leverage gains are constrained amid investments necessary to maintain market leadership. This dynamic is typical for SaaS providers transitioning post-IPO while seeking scale economies.

Current Market Position and Competitive Differentiation via AI-Enabled Solutions

Via Transportation’s moat centers on its end-to-end software platform capable of integrating various public transportation verticals under a singular technology umbrella [S20]. The incorporation of sophisticated AI-driven routing optimization significantly enhances operational efficiencies allowing customers to reduce vehicle idle times and better match supply with demand dynamically — features that materially increase switching costs.

The firm's close collaboration with municipal governments cultivates strong relationships that serve as barriers against encroaching competitors from both traditional transit system vendors like Siemens Mobility or Tyler Technologies as well as newer entrants such as Uber's microtransit initiatives or startups engaging niche markets [S20]. This ecosystem lock-in benefits from Via's technological advances protected through active patent enforcement including victorious litigation against rival RideCo concerning virtual bus stop technologies [S16],[S13].

Yet this competitive landscape remains challenging; rivals possess deeper pockets or established client bases demanding relentless innovation from Via to preserve its category leadership.

Outlook on Growth Opportunities Across Public Sector and Mobility Verticals

Looking ahead, Via’s sizeable backlog of remaining performance obligations at approximately $291 million as of September 30, 2025 signals continued revenue visibility predominantly via government contracting pipelines [S5]. The company emphasizes expansion within heavily regulated public transit markets—including paratransit programs accommodating specialized accessibility needs—which command premium service levels and complex compliance frameworks that can serve as competitive moats but also implementation hurdles.

Further opportunities reside in international markets where local incumbents dominate but technological modernization is nascent [S14]. However international expansion introduces localization demands such as translation, regulatory adherence variations across jurisdictions including GDPR compliance or motor carrier licensing regimes necessitating calibrated operational approaches.

Analysts should monitor contract renewal rates alongside new awards especially amid shifting political environments influencing public transportation funding or policy priorities impacting mobility solutions adoption—for instance changes in transit subsidies or labor regulations that could affect pricing models.

Operational Constraints and Regulatory Risks Impacting Expansion

Via faces multifaceted regulatory challenges complicating growth trajectories. Foremost among these are legal disputes over driver classification featuring independent contractors versus employees—a crucial labor model given Via’s reliance on both employed drivers and contractor partners allocated flexibly based on service type [S4]. These disputes expose the business to costly litigation risk alongside potential shifts in operating costs if courts mandate reclassification.

Cybersecurity stands out as a material operational peril given the sensitive nature of personal data it processes involving riders (including vulnerable populations), drivers, and partner organizations coupled with dependence on external IT infrastructures prone to advanced persistent threats [S1],[S17]. Adherence failures could result not only in financial penalties but significant reputational damage impairing customer trust.

Further regulatory complexity arises from intersecting compliance regimes across TNC laws, data protection statutes (GDPR/CCPA), federally mandated standards for paratransit safety (ADA), student data protections under FERPA/COPPA for school transport verticals—all underpinning the need for granular controls across global operations [S10],[S22],[S19].

Contractual risks due to termination-for-convenience clauses prevalent in government agreements create additional revenue uncertainty potentially precipitated by policy reversals or budgetary constraints impacting contract longevity [S15].

Capital Structure, Cash Flow Patterns, and Investor Return Metrics

Via ended fiscal year 2025 with substantial liquidity totaling approximately $371 million in cash and equivalents on its balance sheet following net proceeds of roughly $307 million from its September IPO after underwriting costs [F1],[S9],[S24]. This cash war chest supports continued investments into product development various vertical expansions despite persistently negative free cash flow estimated near -$32.5 million annually reflecting elevated capex alongside operating losses [F1].

Current assets exceed current liabilities by nearly fivefold yielding a healthy current ratio above 4.9x which provides short-term financial flexibility amid uncertain cash burn schedules post-IPO activities [F1]. However return metrics such as ROE remain deep in negative territory around -15.4%, illustrating ongoing challenges converting burgeoning revenues into shareholder returns amid large accumulated deficits approaching $1.2 billion at year-end 2025 [F1],[S1].

Capital allocation thus prioritizes scaling investments over capital returns such as dividends or buybacks which remain absent given nascent profitability horizons.

Strategic Initiatives to Bolster Profitability and Mitigate Risks

Management acknowledges profitability constraints stemming from expansion-stage spend profiles tied to maintaining technological edge especially integrating AI/machine learning modules enhancing demand prediction & resource allocation across transport modes [S2],[S3]. Efforts underway include streamlining sales cycle efficiencies post-IPO bolstered by amortization management around capitalized commissions aiming at improved customer acquisition cost control [S5],[S2].

Robust legal defenses continue targeting intellectual property assertions particularly defending patents essential to virtual bus stop innovations securing differentiated capabilities vis-à-vis competitors like RideCo whose appeals remain pending [S16],[S13]. Concurrently compliance teams intensify monitoring evolving labor regulations whilst advocating adaptations or exemptions where feasible to preserve contractor engagement models mitigating workforce classification litigation risks [S4].

Heightened investment into cybersecurity frameworks addresses increasing external threat vectors underlying critical infrastructure protecting rider/driver data confidentiality aligned with stricter privacy law enforcement globally [S1].

These initiatives indicate management prioritizes sustainable platform leadership via innovation balanced cautiously against expense discipline realizing path toward eventual profitability remains elongated.

Key Milestones to Monitor for Via’s Trajectory

Given limited explicit forward guidance publicly available ([N/A]), stakeholders should track several pivotal indicators including:

- Contract renewal bandwidth among key government agency clients reflecting satisfaction & pricing power;

- Execution success of AI rollouts quantitatively improving fleet utilization & cost per ride metrics;

- Legal resolution progress particularly surrounding independent contractor cases impacting cost structures;

- Cybersecurity incident frequency/severity reports influencing operational resilience;

- Timelines aligned with deferred revenue recognition per remaining performance obligations disclosures illustrating revenue conversion cadence;

- International market penetration rates evidencing effectiveness of localization strategies amid complex regulatory environments. Monitoring these factors will illuminate whether Via can reconcile accelerating platform adoption against persistent profitability gaps inherent in transitioning incumbent-heavy municipal ecosystems into digitally empowered transit services.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments