How Immuneering’s Novel MEK Inhibitors Are Shaping Late-Stage Oncology Development

Immuneering Corp advances cyclic MEK inhibition to tackle pancreatic cancer, balancing innovation with financial sustainability amid clinical and regulatory challenges.

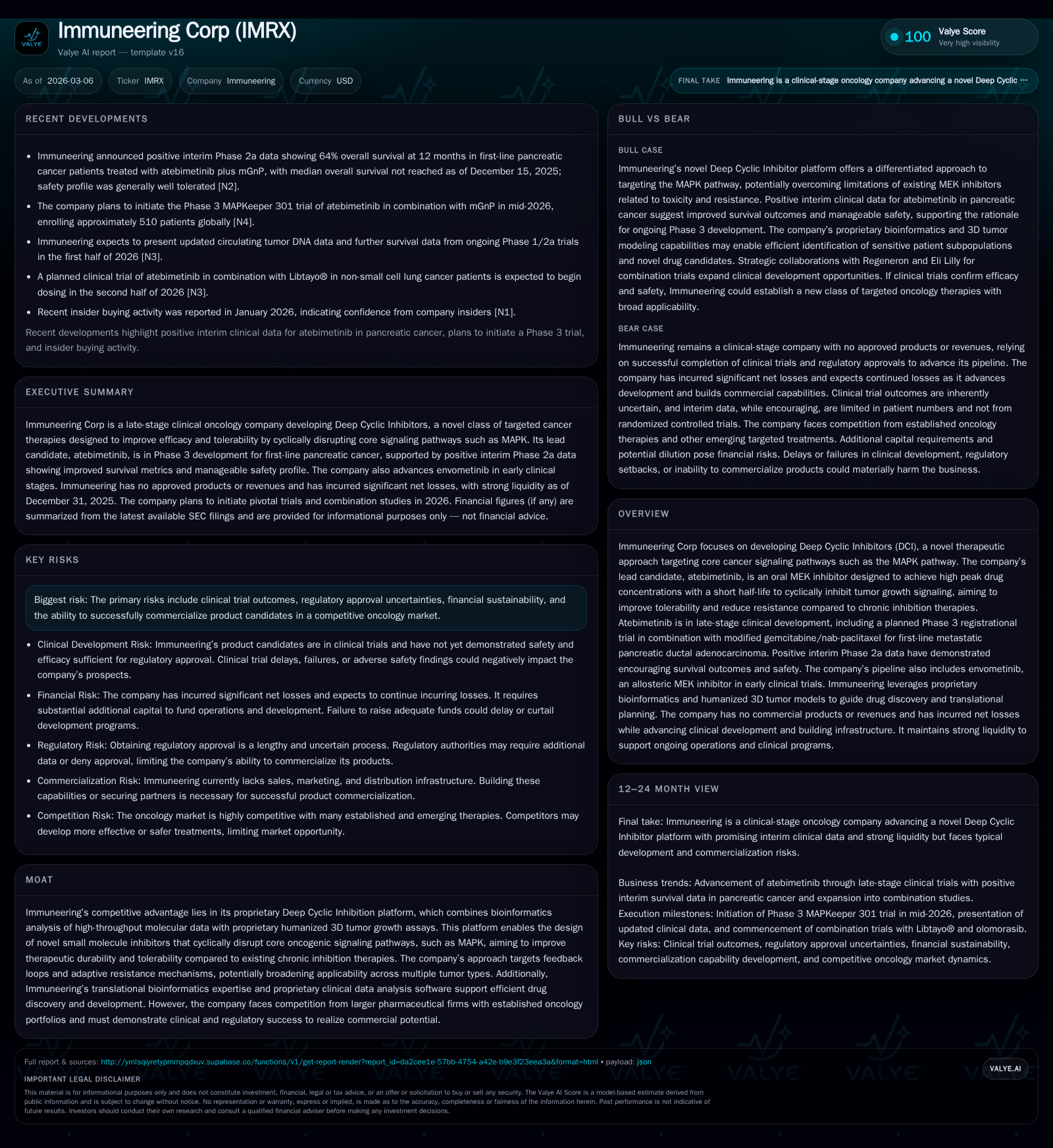

Immuneering Corp is pioneering its Deep Cyclic Inhibition platform targeting MAPK pathway-related cancers, particularly through its lead candidate atebimetinib. The company has demonstrated promising Phase 2a interim data in metastatic pancreatic cancer and is preparing for a pivotal Phase 3 trial while maintaining strong liquidity despite consistent operating losses. Key near-term milestones include enrollment initiation of the MAPKeeper 301 trial and further biomarker data presentations. Challenges remain around regulatory approvals, competitive oncology market dynamics, and transitioning to commercial operations.

Building Momentum: Immuneering’s Historical Investment and Growth Trajectory

Immuneering has no approved products or revenue from product sales as of December 31, 2025 [F1]. The company has shifted focus from computational biology services toward oncology drug development centered on its Deep Cyclic Inhibition (DCI) platform. Over recent years, revenues declined to zero by fiscal year-end 2023 as service operations ceased, while research and development expenses increased substantially [F1].

For fiscal year 2025, Immuneering reported net losses of approximately $56 million, driven primarily by R&D activities supporting clinical progression of its product candidates and infrastructure build-out to support late-stage development. Operating loss moderated slightly to -$59.4 million from -$64.1 million in 2024 [F1]. Cash and equivalents stood at about $128.6 million against current liabilities near $10.1 million, resulting in a strong current ratio of approximately 17.5, providing runway security into key clinical milestones [F1]. This financial foundation reflects a capital allocation strategy focused mainly on advancing pipeline candidates rather than near-term revenue generation.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -56 | -45 | -59 | +8.2% | ||

| 2024 | -61 | -55 | -64 | -14.1% | ||

| 2023 | 0 | -53 | -49 | -58 | -100.0% | -5.9% |

| 2022 | 316952 | -51 | -44 | -52 | -84.8% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -45 | -25.6 |

| 2024 | -55 | -147.5 |

| 2023 | -49 | -59.0 |

| 2022 | -45 | -46.0 |

Source: SEC companyfacts cache [F1].

The Deep Cyclic Inhibition Platform: Technical Edge and Differentiators

Immuneering’s proprietary DCI platform aims to disrupt oncogenic signaling pathways such as MAPK via strategic cyclic kinase suppression. This approach contrasts with chronic inhibition methods that often cause dose-limiting toxicities and adaptive resistance [S1].

Atebimetinib exemplifies this strategy as an oral MEK inhibitor designed for high peak plasma concentration followed by rapid clearance to enable intermittent pathway suppression. This dosing profile intends to preserve normal cellular signaling while depriving tumor cells of sustained proliferative signals [S1]. The platform integrates humanized three-dimensional tumor growth assays offering enhanced predictive preclinical modeling over traditional methods. Complementary translational bioinformatics workflows analyze molecular data to optimize target engagement timing against resistance mechanisms [S1].

These innovations distinguish Immuneering’s DCI approach within kinase inhibition strategies by potentially broadening therapeutic indices across multiple cancers.

Late-Stage Pipeline Spotlight: Atebimetinib’s Clinical Progress in Pancreatic Cancer

Atebimetinib targets metastatic pancreatic ductal adenocarcinoma (PDAC), a malignancy with limited effective therapies. Positive interim Phase 2a data showed encouraging survival outcomes and a favorable safety profile when combined with modified gemcitabine/nab-paclitaxel chemotherapy [S1,S3].

The company plans mid-2026 initiation of the global Phase 3 MAPKeeper 301 trial enrolling approximately 510 first-line metastatic PDAC patients randomized between atebimetinib+mGnP versus standard GnP alone. Primary endpoint is overall survival; secondary endpoints include progression-free survival and quality of life measures [S1]. Updated circulating tumor DNA biomarker data are expected at a major scientific meeting in Q2 2026 [S3]. Additionally, dosing initiation is planned for an atebimetinib plus Libtayo® combination trial in non-small cell lung cancer during H2 2026 [S3]. These efforts mark significant steps toward clinical proof-of-concept across solid tumors using the DCI platform.

Navigating Near-Term Clinical Milestones and Regulatory Outlook

Key upcoming catalysts include patient dosing start for MAPKeeper 301 in mid-2026 and interim survival updates from ongoing pancreatic cohorts within H1 calendar year [S1,S3]. The non-small cell lung cancer combination trial commencement later in the year adds developmental momentum.

MAPKeeper serves as a registrational study aligned with FDA and international review protocols. While approval remains uncertain given industry complexities around oncology durability and tolerability endpoints, the focus on overall survival alongside integrated biomarker analyses strengthens submission packages [S1]. Successful navigation will be critical for investor confidence as Immuneering advances toward commercialization readiness.

Financial Overview: Strong Liquidity Amid Elevated Research Investment

As of December 31, 2025, Immuneering held $128.6 million in cash against $10.1 million in current liabilities yielding a robust current ratio near 17.5 [F1]. Operating cash flow was negative $45.3 million for FY2025 due mainly to continued investment in clinical programs without product revenues [F1]. Capital expenditures were modest at approximately $142 thousand reflecting prioritization of clinical development over infrastructure expansion [F1].

This financial position supports operational continuity through pivotal inflection points but underscores reliance on future financing or partnerships beyond existing reserves.

Capital Deployment Trends and Outlook

Year-over-year net loss narrowed slightly (-$56 million vs. -$61 million), indicating controlled incremental spending amid expanding developmental activity [F1]. No product sales revenue to date; funding has come from prior service revenues (now ceased), equity issuance, and convertible debt [F1]. Approximate return on equity stands at -25.6% consistent with early-stage biopharma investing heavily ahead of commercialization potential [F1].

Capital allocation emphasizes sustaining pivotal trials rather than commercial infrastructure build-out at this stage.

Risk Assessment: Trial Uncertainties and Commercial Complexity

Immuneering faces typical late-stage oncology risks including potential failure of pivotal trials or safety issues limiting labeling . Regulatory approval remains uncertain despite robust design focusing on overall survival.

Competitive pressures from large pharmaceutical firms with established oncology portfolios could impact market positioning post-approval [S4]. Intellectual property litigation risks may affect exclusivity duration or require costly licensing arrangements [S5,S9,S15]. Compliance burdens under healthcare fraud statutes, pricing transparency rules including Medicaid rebate obligations, HIPAA privacy regulations and international standards add complexity and potential cost inflation . Product liability insurance costs are rising even pre-commercialization [S6,S10,S18,S20]. Transitioning from research-focused operations to commercial execution poses organizational risks.

Investor Takeaways: Upcoming Catalysts to Monitor

Key near-term events shaping investor outlook include:

- Mid-2026 initiation of MAPKeeper 301 patient dosing marking entry into registrational trial phase;

- Q2 2026 presentation of ctDNA biomarker data elucidating resistance mechanisms;

- Interim survival updates from ongoing pancreatic cohorts within H1 calendar year;

- Late-2026 start of atebimetinib plus Libtayo® combination trial expanding indication breadth;

- Monitoring cash runway relative to operating cash flow deficits informing financing needs.

Balancing innovative science underpinning DCI differentiation against inherent developmental risk will be essential for assessing Immuneering’s trajectory toward late-stage success.

This analysis is based entirely on disclosed company data from SEC filings ([F1], [S1]-[S29]) without projection or endorsement of investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments