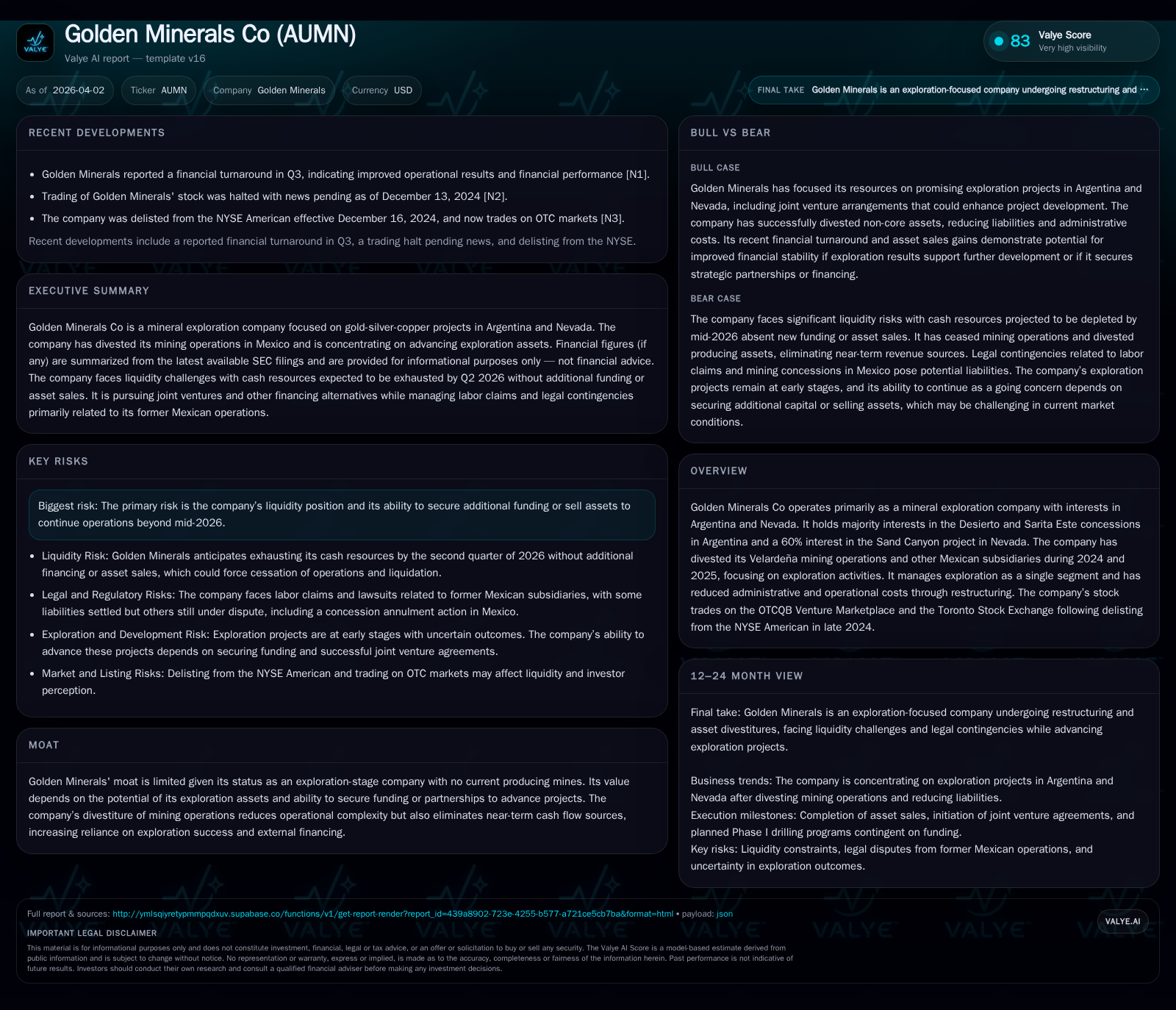

Golden Minerals Co Confronts Cash Constraints While Transitioning to Pure Exploration Focus

The company’s pivot to exploration-only assets introduces funding and operational challenges amid asset sales.

Golden Minerals has restructured from owning producing mines to focusing exclusively on exploration projects in Argentina and Nevada following the divestiture of its Mexican mining operations. Its financial results reflect significant revenue decline and ongoing losses, with a precarious liquidity position projecting cash exhaustion by mid-2026 absent external financing or asset sales. The company’s near-term strategy hinges on advancing key exploration assets through joint ventures and drilling programs, but appreciable value realization remains contingent on exploration success and capital access. Recent cost reductions and asset monetizations have improved the balance sheet somewhat, yet sizable operational risks, legal claims related to former operations, and regulatory uncertainties persist.

Company Background and Recent Strategic Shift

Golden Minerals Co (ticker: AUMN) has undergone a marked transition over recent years from an intermediate producer with mining operations largely centered in Mexico toward an exploration-stage company focused primarily on South America and select U.S. projects. This repositioning culminated with the sale of Velardeña sulfide plant, Chicago mines, and multiple Mexican subsidiaries during 2024 and 2025 [S26]. Concurrently, Golden Minerals divested advanced exploration properties such as El Quevar in Argentina and Yoquivo in Mexico.

This strategic pivot reduced operational complexity by exiting cash-flow-producing assets but also eliminated near-term revenue sources, critically heightening reliance on successful exploration outcomes and third-party financing [S6]. The company now operates as a single segment focused solely on mineral exploration, primarily holding majority interests in the Desierto (67%) and Sarita Este (51%) concessions in Salta Province, Argentina, plus a 60% stake in the Sand Canyon project in Nevada acquired through an earn-in agreement [S7][S17].

Historical Financial Performance

Golden Minerals’ top-line performance has shown significant contraction alongside persistent operating losses amid restructuring activities. Revenue declined sharply from $25.6 million in 2021 to $12.0 million by end-2023 — a near halving reflecting asset sales and ceased production [F1]. Operating income remained negative throughout this period but showed marginal improvement moving from -$14.7 million in 2021 to -$4.6 million in 2024, attributable largely to lower operating costs after divestitures.

Net losses continue to be substantial with the latest available full-year net loss recorded at -$7.6 million for 2024 [F1]. Operating cash flow has been consistently negative outside of an anomalous positive CFO of $1.4 million in 2021 when the company was still generating revenue from mining. Most recently, operating cash flow fell -$7.7 million in 2024 [F1]. Capital expenditures have been negligible (~$27k), consistent with an explorer expensing most exploration costs rather than capitalizing development outlays [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | ||||||

| 2024 | -8 | -8 | -5 | +17.6% | ||

| 2023 | 12 | -9 | -10 | -9 | -48.5% | +6.8% |

| 2022 | 23 | -10 | -10 | -10 | -9.0% | -372.8% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | |

| 2024 | 361.6 |

| 2023 | -180.5 |

| 2022 | -152.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue YoY indicates percent change compared to prior year.

The company's equity position turned negative as of year-end 2024, roughly -$2.1 million [F1], impairing traditional return metrics like ROE which stand at approximately +361%, but this distortion arises because net losses outpace shrinking equity.

Liquidity Position and Capital Allocation

Golden Minerals’ liquidity profile illustrates mounting constraints as cash balances declined from $3.2 million at December 2024 to about $1.3 million by year-end December 2025 [S5][S16], with current liabilities around $1.4 million giving a current ratio near ~0.64 based on latest data [F1]. The company acknowledges that available funds will likely be exhausted by Q2 2026 absent new financing or asset monetization [S7][S16].

Cost containment via restructuring had been effective during 2024-25, preserving capital while divesting non-core assets for proceeds totaling several million dollars across multiple transactions [S7][S26]. However, operating losses continue sharply negative while ongoing expenditures relate almost exclusively to exploration activities without offsetting revenues.

Capital allocation decisions tilt strongly toward survival: expenditures remain minimal, share-based compensation expense is nominal (~$3k recognized for restricted stock grants in 2025) [S21], and no dividends or buybacks are planned — unsurprising given strained finances.

Operational Highlights and Growth Prospects

Exploration efforts are concentrated on advancing the Sarita Este/Desierto projects in northwest Salta Province Argentina alongside the Sand Canyon project in Nevada.

At Sarita Este/Desierto, geological surveys identified alteration zones consistent with precious metal systems, prompting joint venture agreements — notably with Cascadero Mining Ltd — to support Phase I drilling programs designed to test extensions of gold mineralization across property boundaries [S7]. Progress here depends critically upon finalizing joint venture terms and securing additional funding.

The Sand Canyon project represents an early-stage gold-silver venture acquired under an earn-in agreement granting Golden Minerals a majority interest if certain milestones are met [S7][S17]. Exploration here is nascent but geologically promising given regional mining history.

Despite this pipeline potential, all properties remain exploratory without demonstrated mineral reserves compliant with SEC standards (Regulation S-K Subpart 1300), limiting material near-term valuation catalysts until substantive drilling results convert potential into proven reserves [S17].

Risks and Legal Contingencies

The transition away from producing assets has not entirely mitigated all historical operational risks:

- Labor claims totaling approximately $250k remain accrued related to former employees of Argentine subsidiaries as of year-end 2025; these are being vigorously contested by management [S1][S8].

- Previous labor claims and supplier disputes tied to Mexican subsidiaries were resolved concurrent with asset sales between late-2024 and late-2025 [S1][S3][S8].

- A disputed Mexican mining concession fee claim approximating $403k linked to previously sold subsidiaries was rejected by authorities following cancellation of the concession; Golden Minerals intends legal challenge asserting procedural irregularities [S1][S3][S9][S15].

- An ongoing appeal exists regarding joint and several liability rulings involving prior subsidiary Minera William connected to settlement disputes; management currently assesses low likelihood of future liability [S8][S18].

These legacy exposures underscore challenges inherent within divesting mining properties abroad where environmental reclamation obligations, tax uncertainties, and labor law complexities persist beyond operational control.

Market Presence and Corporate Governance Notes

With delisting from NYSE American effective December 16, 2024, Golden Minerals’ shares currently trade primarily on the OTCQB Venture Marketplace as well as the Toronto Stock Exchange under symbol AUMN [N1][S26][S27].[N1]

The Board enforces strict insider trading policies including prohibitions against short sales or margins for directors/executives aiming to preserve governance integrity amidst volatile market conditions [S14].[N1]

Conclusion: Sustained Uncertainty Hinges on Financing Success

Golden Minerals today epitomizes a junior mineral explorer navigating financial distress while betting on geological prospects across two continents without producing operations or near-term revenue streams.

Its past growth was anchored substantially in mining operations now relinquished; future growth potential concentrates on exploration success at Sarita Este/Desierto and Sand Canyon coupled tightly with its ability to secure capital or partner deals before mid-2026 liquidity horizons close.

Investors should monitor announcements related to joint venture progress, drill results clarifying mineralization potential, updates on financing rounds or asset sales as critical milestones that could reshape viability narratives beyond the stark working capital constraints currently disclosed.

This report synthesizes publicly available SEC filings, recent news releases, and financial data without providing investment advice or specific recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments