BridgeBio Oncology Advances Early-Stage KRAS and PI3Kα Inhibitors with Multiple Phase 1 Trials Underway

BridgeBio Oncology reports ongoing Phase 1 clinical development of its novel oncology pipeline focused on targeting KRAS and PI3Kα mutations with oral small molecules.

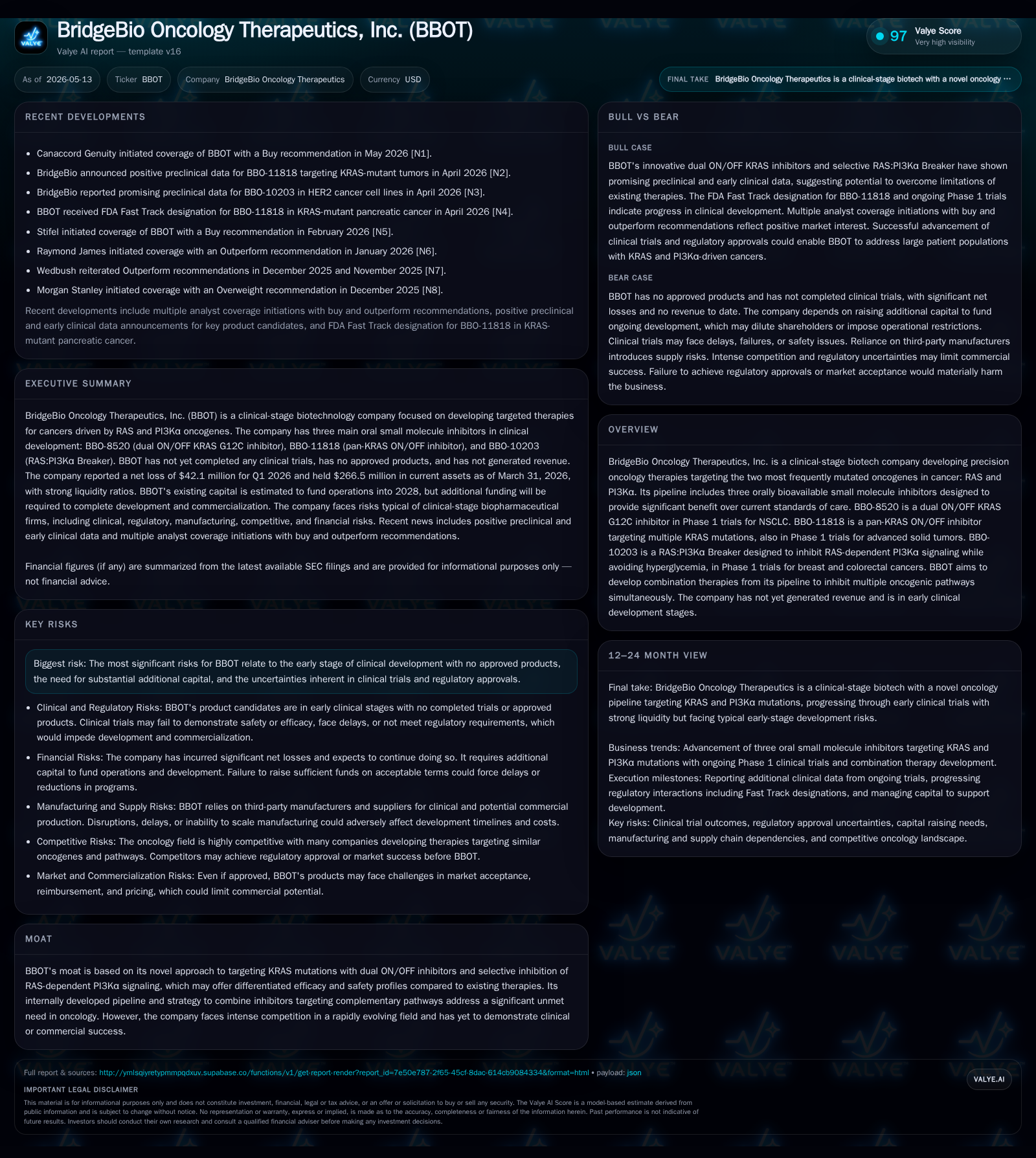

BridgeBio Oncology Therapeutics, Inc. (BBOT) remains a pre-revenue clinical-stage biotech company concentrating on precision oncology therapies aimed at the RAS and PI3Kα oncogenic pathways. Its latest quarterly filing dated May 12, 2026, confirms continued advancement of three Phase 1 small-molecule inhibitors—BBO-8520, BBO-11818, and BBO-10203—with a strategic emphasis on combination regimen development to target multiple oncogenic drivers concurrently. The company operates in a highly competitive, fast-evolving oncology landscape addressing significant unmet needs in KRAS-mutant cancers. While BBOT’s novel approach offers potential differentiation through dual ON/OFF KRAS inhibition and selective RAS-dependent PI3Kα blockade, it faces material execution risks typical of early-stage biotechs including trial outcomes, regulatory approvals, and capital requirements. As of quarter-end, substantial cash reserves support operations into early 2028 but further financing will likely be necessary to sustain progress toward pivotal trials.

Recent Operating Update

The May 12, 2026 Form 10-Q establishes BridgeBio Oncology Therapeutics’ continued progress as a clinical-stage company focused on novel precision oncology therapies targeting mutations in RAS (KRAS) and PI3Kα oncogenes [S2]. All three lead candidates—BBO-8520 (dual ON/OFF KRAS G12C inhibitor), BBO-11818 (pan-KRAS ON/OFF inhibitor), and BBO-10203 (RAS:PI3Kα Breaker designed to inhibit RAS-dependent PI3Kα signaling while minimizing hyperglycemia)—remain in Phase 1 trials for various solid tumors including NSCLC, breast, colorectal, and pancreatic cancers [S2][S3]. Management reiterates its aim to develop combination regimens that simultaneously inhibit multiple oncogenic pathways leveraging their internally developed small molecule pipeline [S2]. These early-stage programs have yet to yield clinical proof-of-concept data but have recently received regulatory Fast Track designation for BBO-11818 in KRAS-mutant pancreatic cancer—a signal of potential accelerated development timelines if positive data emerge [N4].

This latest quarterly update does not report revenue generation or product approvals given the pre-commercial status but confirms sustained R&D investment fueled by existing balance sheet liquidity [S2][F1]. Notably, the company disclosed risks common to clinical-stage biopharma including delays in trial commencement/completion, regulatory uncertainty, manufacturing complexities surrounding novel small molecules, healthcare compliance exposures, and potentially dilutive future capital raises [S5][S22].

Business Model

BridgeBio Oncology Therapeutics operates under a classic early-stage biotech model: discovery and internal development of proprietary precision oncology therapies primarily delivered through orally bioavailable small molecule inhibitors tailored for specific oncogenic mutations. Revenue generation is currently nonexistent; value creation depends on advancing pipeline candidates through rigorous multi-phase clinical trials aimed at demonstrating superior safety and efficacy profiles relative to standard-of-care treatments.

Their targeted approach focuses on the two most prevalent oncogene families driving many cancers: RAS—specifically KRAS mutations—and the PI3Kα pathway. The development portfolio features:

- BBO-8520: A dual ON/OFF inhibitor acting against the G12C mutation of KRAS—commonly mutated in non-small cell lung cancer (NSCLC).

- BBO-11818: A pan-KRAS ON/OFF inhibitor targeting several relevant KRAS mutations across advanced solid tumors.

- BBO-10203: A novel agent disrupting RAS-dependent PI3Kα signaling while sparing systemic glucose metabolism to prevent hyperglycemia side effects.

The firm's strategic edge derives from this dual-pronged approach that attempts not only to inhibit various mutational states of KRAS via combined ON/OFF inhibition mechanisms but also to address downstream pathway activation (via PI3Kα) which drives tumor progression. Furthermore, BridgeBio seeks to develop combination therapies leveraging these agents together or with other drugs to overcome resistance seen with monotherapies.

Revenue mechanics follow conventional biotech expectations: post regulatory approval and commercialization—which are currently distant—the company would monetize product sales via healthcare providers/payers globally. Income drivers would include sales volume growth tied to patient uptake metrics in indication-specific markets plus pricing flexibility influenced by competitive alternatives and reimbursement landscapes. Margins would initially reflect high-cost specialized manufacturing costs tapering towards more normalized biotech commercial margins if scale is achieved.

Industry Structure & Competitive Position

The oncology drug development space focusing on RAS mutations has witnessed intensified competition notably following landmark successes targeting KRAS G12C mutations by companies such as Amgen (sotorasib) and Mirati Therapeutics (adagrasib). While these competitors are past pivotal phases with some approved drugs on market, BridgeBio pursues differentiation through its dual ON/OFF inhibition strategy intended to enhance response durability by preventing canonical reactivation of KRAS signaling —a known resistance mechanism.

Also structurally significant is the focus on PI3Kα signaling downstream of RAS. Effective selective inhibition that avoids hyperglycemia side effects could resolve dosing and compliance barriers hampering current PI3K inhibitors from wider acceptance. This nuanced mechanistic selectivity may confer differentiation; however developing safe combinations poses considerable scientific complexity.

Given the highly fragmented yet intensely competitive oncology R&D ecosystem featuring both large pharmaceutical incumbents with expansive portfolios as well as nimble specialty biotechs aggressively pursuing varied mutant-specific kinase inhibitors or immunotherapy combos—the pathway to market dominance demands not only robust clinical evidence but also timely regulatory navigation and effective commercial partnerships.

Growth Drivers

Growth prospects for BridgeBio hinge principally on several interrelated catalysts:

- Clinical Trial Progression: Advancement from Phase 1 dose-escalation/expansion cohorts into registrational trials represents major de-risking steps. Positive interim efficacy/safety readouts will underpin valuation inflection points.

- Regulatory Milestones: Designations such as Fast Track for BBO-11818 accelerate FDA review timelines enhancing speed-to-market potential.

- Combination Therapy Development: Success in rationally combining pipeline agents may elevate clinical efficacy beyond monotherapy standards offering compelling commercial appeal.

- Platform Expansion: Broadening indications based on mutational targets could enlarge addressable patient populations.

- Strategic Collaborations: Partnering with established pharma may provide capital resources and commercialization infrastructure.

- Capital Availability: Maintaining sufficient funding resources ensures uninterrupted advancement through costly clinical phases.

Metrics linked directly to these growth drivers include patient enrollment rates in trials, biomarker validation success rates, regulatory feedback timelines, IP protection breadth expansions, manufacturing scale-up milestones, partnership deal announcements, and cash burn versus runway calculations.

Risks & Growth Constraints

Several critical risks afflict BridgeBio’s ability to translate its promising science into commercially viable medicines:

- Clinical Uncertainty: Early-stage pipeline candidates face substantial risk of failing efficacy or encountering intolerable safety signals during later-phase trials despite promising preclinical data.

- Regulatory Hurdles: Lengthy unpredictable approval cycles especially given novel mechanisms with little prior precedent can delay market entry.

- Capital Intensity: Extensive cash burn without product-generated revenues necessitates frequent financing rounds which dilute shareholders.

- Manufacturing Complexity: Producing innovative dual-action small molecules at scale entails technical risks impacting supply chain reliability.

- Competitive Pressures: Rapid innovation among global competitors might eclipse BridgeBio’s offerings absent timely differentiation.

- Healthcare Compliance & Legal Exposure: Operating within heavily regulated settings requires vigilance against violations of anti-bribery laws like FCPA or marketing regulations; failures here can lead to costly penalties restraining operations.

- Pricing & Reimbursement Challenges: Global price controls particularly in Europe impose revenue limitations adversely affecting profitability potentials post-commercialization [S4][S9][S18].

What to Watch Next

Investors and industry observers should monitor several upcoming indicators signaling BridgeBio’s execution:

- Additional clinical data releases from Phase 1 trials—especially early signs of efficacy or safety profiles consistent with differentiated outcomes.

- Initiation announcements for pivotal or registration-directed studies allowing closer evaluation of BBOT's commercialization timeline assumptions.

- Reports concerning combination therapy regimen designs or early combination trial enrollment progress.

- Regulatory updates regarding FDA or EMA designations accelerating approval pathways beyond existing Fast Track status.

- Capital raising activities addressing funding adequacy for multi-year late-stage development commitments.

- Intellectual property developments expanding patent coverage protecting proprietary compounds against generic competition.

Financial Profile Snapshot (March 31, 2026)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $53mm | |

| 2026-03-31 | ||

| Total debt | $716000 | |

| 2026-03-31 | ||

| Net debt | $-52mm | |

| 2026-03-31 | ||

| Current assets | $267mm | |

| 2026-03-31 | ||

| Current liabilities | $43mm | |

| 2026-03-31 | ||

| Current ratio | 6.16x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

This strong liquidity position coupled with negligible debt offers a healthy financial runway enabling continued investment through early pivotal program stages as projected by management into early 2028 [F1][S16]. However, the company acknowledges additional capital may be needed thereafter depending on trial outcomes and partnership progress [S2].

Disclaimer

This analysis is provided solely for informational purposes without any recommendation or solicitation related to acquiring securities of BridgeBio Oncology Therapeutics, Inc. Investors should conduct their own due diligence considering all publicly disclosed SEC filings and market factors before making any investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments