Healthier Choices Management Ramps IP-Driven Vape Market Strategy After Spin-Off

HCMC’s latest quarter highlights a strategic pivot towards intellectual property monetization amid tightening liquidity and regulatory pressures.

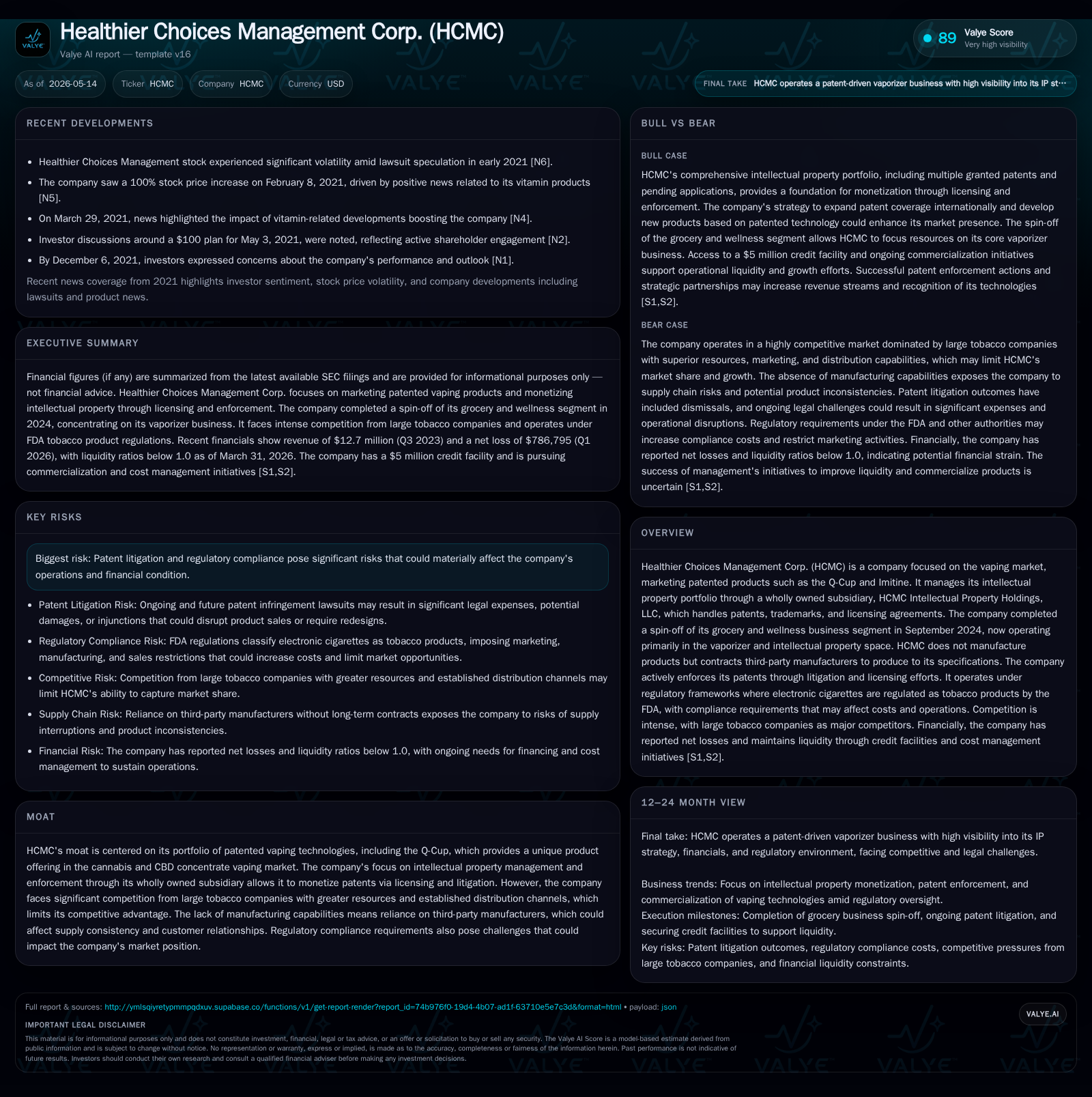

Healthier Choices Management Corp. is accelerating its transition to a patent-centric business model after spinning off its grocery and wellness segments in late 2024. The May 2026 10-Q revealed a $5 million credit line with initial borrowings for working capital, underscoring ongoing operational challenges and the need for financing as HCMC focuses on licensing its patented vaping technologies such as the Q-Cup™. The company faces a competitive landscape dominated by large tobacco firms, regulatory complexity under FDA tobacco product oversight, and patent litigation risks that collectively shape its growth trajectory. Key milestones to monitor include licensing deals, patent enforcement outcomes, and FDA compliance adjustments.

Latest Quarterly Developments Set Operational Tone

In its latest quarterly filing dated May 14, 2026 ([S2]), Healthier Choices Management Corp. disclosed accessing its recently established $5 million unsecured loan facility arranged with Sabby Volatility Warrant Master Fund, Ltd., drawing $500,000 as of March 27, 2026 ([S3]). This credit line was secured primarily to bridge working capital needs during this strategic transition phase after completing its spin-off of the grocery and wellness businesses in September 2024 ([S1]).

The borrowing highlights liquidity pressure points despite management’s prior $4 million debt-for-equity exchange which materially improved balance sheet flexibility ([S4]). At quarter-end March 31, 2026, HCMC had cash and equivalents of approximately $1.1 million against current liabilities of about $2.14 million, yielding a current ratio of just 0.62 ([F1]). Without these funds, operational continuity would face heightened risk given ongoing investments in commercialization and patent enforcement activities.

This borrowing also indicates an urgent need to sustain operations given historical net losses and negative working capital reported pre-spin-off ([S1]). Despite these constraints, management remains focused on advancing licensing negotiations and fostering strategic partnerships aimed at leveraging its intellectual property portfolio ([S4]).

Business Model: From Wellness Spin-Off to IP-Focused Vapor Tech

Following the carve-out of the grocery/wellness segment (now traded as Healthy Choice Wellness Corp.) in late 2024 ([S1]), HCMC repositioned itself as a pure-play intellectual property holding company centered on vaping technologies. Revenues are driven exclusively by royalty income from licensing patented products and settlements arising from active patent enforcement litigation conducted via its wholly owned subsidiary HCMC Intellectual Property Holdings LLC ([S1],[S7],[S11]).

Notably absent is any direct manufacturing capability; instead, production is outsourced entirely to third-party OEMs contracted on purchase order terms without binding output guarantees ([S15]). This approach minimizes capital expenditure but adds supply chain risks that could affect product availability and quality perception in the competitive vape market.

The flagship offering within this model is the patented Q-Cup™ technology—a microdosing vaporizer cartridge design using a small quartz cup tailored for cannabis or CBD concentrates. This external heating without direct concentrate contact enhances efficiency and consumer convenience especially for medicinal or recreational users sensitive to dosing accuracy ([S1],[S7]). Complementing Q-Cup™ is the Imitine product line, also backed by patents intended to diversify revenue sources.

The company augments revenue streams through exclusive and non-exclusive licensing arrangements while also exploring joint ventures or co-development deals that spread commercialization risk and tap additional markets ([S11]). These initiatives underscore a strategy relying heavily on intellectual property asset leverage rather than volume-based product sales.

Distinct Competitive Position in a Crowded Vape Patent Landscape

HCMC operates in an intensely competitive environment dominated by entrenched tobacco conglomerates such as Altria Group Inc., Philip Morris USA, JT International, Imperial Tobacco, and Reynolds American Inc. These competitors possess far superior distribution networks, marketing muscle, scale economies, and deeper R&D budgets which pose formidable barriers for smaller entities like HCMC ([S9],[S15],[S18]).

To defend its niche position centered on patented vaporizer innovations like Q-Cup™, HCMC pursues vigorous litigation strategies enforced through federal courts focusing on alleged infringements by industry giants (e.g., lawsuits filed against Philip Morris's IQOS™ product and R.J. Reynolds Vapor’s Vuse) ([S10],[S15]). However, not all legal outcomes favor HCMC; for example, an appeal denial before the Federal Circuit in late 2024 invalidated certain patent claims leading to dismissal of related suits ([S10]).

Regulatory scrutiny adds additional complexity as the FDA classifies electronic cigarettes as "tobacco products" subjecting manufacturers like HCMC’s licensees to stringent marketing controls such as banned free samples, health warnings inclusion, retailer age restrictions (minimum age 21), packaging mandates, and advertising limitations under the Tobacco Control Act ([S9],[S10],[S16]). Compliance costs have increased materially though exact impacts remain difficult to quantify. Moreover, potential future rules around child-resistant packaging or ingredient disclosures threaten further cost inflation or marketing constraints.

The combination of high-profile patent battles plus evolving federal/state tobacco regulations creates a challenging playground where legal defensibility of patents and regulatory agility are prerequisites for sustained competitiveness.

Growth Catalysts: Licensing, Product Innovation, and Strategic Partnerships

Growth prospects hinge critically on expanding the scope and geographic coverage of HCMC’s intellectual property portfolio. Since 2019 through end-2025 alone, nine new U.S. patents were granted in vaping-related technology fields indicating steady innovation output ([S11],[S18]). Efforts are underway to extend protection internationally targeting key markets where vaporizer adoption grows.

Commercialization avenues also lean heavily on securing both exclusive licenses commanding premium royalties and broad non-exclusive agreements enabling widespread adoption by third-party distributors or vape manufacturers seeking differentiated technology ([S11]). Product development spending remains material despite tight financials reflecting commitment to maintain competitive edge amid rapid technological evolution within vaping hardware segments ([S11],[S7]).

Additionally,"marketing campaigns targeting medicinal/recreational cannabis consumer niches who value precise dosing solutions offered by Q-Cup™ devices aim to build brand awareness while attracting licensees able to scale adoption ([S11]). Partnerships may involve co-development projects sharing R&D cost burdens while amplifying commercialization capacity against larger incumbents.

Cost rationalization post spin-off—including reduced consulting fees combined with measured reinvestment focused on IP expansion—features prominently in management's playbook ensuring efficient capital use supports sustainable growth endeavors rather than costly diversification attempts outside core competencies ([S4],[S6]).

Risks on the Horizon: Litigation, Regulatory Compliance, and Manufacturing Dependency

A critical watchpoint for HCMC lies in ongoing patent litigation which is double-edged: while successful cases can generate licensing income or settlement windfalls securing exclusivity windows that justify premium pricing for licensees; adverse rulings—as experienced with recent Federal Circuit decisions invalidating key claims—can erode these intangible assets severely impacting revenue predictability ([S10],[S14],[S15]). Such lawsuits are capital-intensive requiring legal expertise while diverting management attention away from commercial execution.

Regulatory developments also pose systemic risks. The FDA’s dynamic rulemaking could impose heightened testing standards or impose new restrictions limiting permissible claims about reduced harm potentially curbing consumer uptake or increasing compliance costs significantly beyond current estimates ([S9],[S16],[S12]). State-by-state legislation complicates market access creating fragmentation unlike standardized food or drug sectors.

Dependency on several third-party contract manufacturers exposes operational vulnerabilities. Any disruption or inconsistencies in supply quality—since contracts are purchase-order based rather than volume-guaranteed—could tarnish brand reputation among niche consumers drawn to premium experience attributes embedded in Q-Cup™ products ([S15]). Moreover, these relationships limit operating leverage whereby renegotiating pricing terms upward or ensuring raw material availability becomes challenging without vertical integration.

Financial strain linked to negative working capital relative to short-term liabilities also accentuates enterprise risks particularly under scenarios of delayed monetization from licensing efforts or protracted litigation costs requiring further debt draws elevating interest burdens at relatively high rates (12% annual rate per recent credit agreement) despite unsecured status ([F1],[S3],[S4]).

Upcoming Milestones and Indicators to Monitor

Investor attention should closely track several operational signposts signaling progress toward strategic goals:

- Announcements of new licensing deals or renewals expanding revenue bases indicating traction for patented tech penetration into broader vape markets.

- Patents pending decisions or legal rulings (particularly inter partes reviews) which can affirm or weaken core IP protections underpinning revenue streams.

- Updates on FDA regulatory compliance adaptations including timelines for meeting new labeling/testing mandates reflecting operational readiness ahead of intensified enforcement.

- Quarterly cash burn rates vis-à-vis credit facility utilization rates providing insight into sustainability of current liquidity buffers without dilutive equity events or refinancing risk.

- Any cost rationalization outcomes indicating enhanced operating discipline improving margins through optimized SG&A expenditure reflective of leaner administrative footprint after spin-off transitions. These milestones collectively provide measurable KPIs aligning with management’s publicly stated focus areas outlined in recent filings ([S2],[S3],[S6]).

Current Financial Position and Liquidity Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1137634 | |

| 2026-03-31 | ||

| Current assets | $1319064 | |

| 2026-03-31 | ||

| Current liabilities | $2mm | |

| 2026-03-31 | ||

| Current ratio | 0.62x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

While past restructuring efforts replaced approximately $4 million intercompany obligations with equity shares strengthening solvency metrics structurally ([S4]), total reported reported debt exposures remain elevated due largely to prior financing arrangements not yet fully retired [F1]. Managing this leverage alongside investment in patent commercialization will require delicate balance given historical operating losses persisting through recent years ([F1]).

Disclaimer

This analysis is for informational purposes only based entirely on publicly available SEC filings up to May 14, 2026. It does not constitute investment advice or recommendations regarding Healthier Choices Management Corp.'s securities. Investors should conduct their own due diligence before making any investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments