Senstar Technologies Catalyzes Supply Chain Adjustments into Growth Phase

Senstar’s latest quarter highlights strategic supply chain diversification and US domestic manufacturing to navigate tariff pressures and drive growth.

In its latest 6-K filings from May 2026, Senstar Technologies Corp outlined key operational shifts emphasizing diversification of supplier base and initiation of US-based production for core perimeter intrusion detection products. These changes aim to mitigate escalating trade tensions and tariffs impacting the company’s global supply chain across Canada, the US, EMEA, and APAC. Senstar’s business combines hardware sensor systems with video management software and recurring services, competing in a fragmented security market requiring innovation and reliability. Growth is catalyzed by expanded domestic manufacturing, loyal customer retention, and integration of recent acquisitions like Blickfeld GmbH. However, risks remain from trade policy volatility and supply constraints which may affect pricing and delivery.

Latest Quarterly Operating Update: Actions and Implications

Senstar Technologies Corporation’s May 4, 2026 filing (6-K) officially announced the submission of its 2025 annual report, accompanied by interim disclosures outlining strategic supply chain adjustments designed to confront rising global trade uncertainties [S2]. The company is actively pivoting sourcing strategies away from traditional APAC and certain EMEA suppliers by diversifying vendors and initiating localized manufacturing capabilities within the United States specifically for key products such as FiberPatrol and FlexZone [S1]. This move reflects management's recognition of persistent US tariff regimes and reciprocal international trade restrictions impacting component costs and logistics across its operating geographies of Canada, US, EMEA, and APAC.

This evolution marks an operational inflection point as Senstar recalibrates its global supply networks to better withstand tariff-induced cost pressures while preserving product availability. Notably, these efforts come amidst seasonal revenue patterns typical for the perimeter intrusion detection market—a sector heavily reliant on government budgets that crystallize late in fiscal years—and project delays caused by harsh weather conditions early in the year [S1].

Quarterly reports reaffirm that these tactical supply chain changes are becoming critical near-term priorities driving operational focus as zeroing in on margin stabilization against raw material cost inflation is essential.

Business Model and Core Product Portfolio Overview

Senstar generates revenues primarily through sales of physical security hardware—such as fiber optic intrusion detection sensors (FiberPatrol), radar-based perimeter detection (FlexZone), along with pipeline security systems (Omnitrax)—complemented by software offerings like Senstar Symphony which integrates video management with intelligent video analytics [S1]. These product lines are supported by recurring income from service contracts including maintenance agreements typically offered on fixed-price or time-and-materials bases plus software licensing fees.

Revenue recognition follows ASC 606 standards with distinct performance obligations identified between hardware shipments and ongoing services [S1]. This dual reliance on tangible equipment sales paired with enduring service relationships fosters higher customer stickiness especially in sectors where system reliability is mission-critical.

Product quality reputation figures prominently given the industry’s demand for low false alarm rates alongside high detection accuracy—parameters on which Senstar competes directly through proprietary technologies safeguarded by patents and trade secrets [S1]. The company’s software-centric solutions add further differentiation potential amid growing demand for integrated security operations centers capable of comprehensive surveillance analytics.

Competitive Landscape and Industry Dynamics

The perimeter intrusion detection system (PIDS) industry remains fragmented yet intensely competitive with no single dominant player [S1]. Senstar confronts rivals including Southwest Microwave Inc., AVA (formerly Future Fibre Technologies), Fiber Sensys (Optex), Gallagher Group among others [S1]. Competitiveness hinges on proven field performance minimizing nuisance alarms, comprehensive customer support networks, price competitiveness, and continuous technological innovation.

Senstar's position benefits from long-standing client relationships particularly in government procurement channels where elongated decision timelines introduce lumpy revenue patterns but bolster contract renewal potential if reliability standards are met [S1]. Geographic diversification across North America ($18M revenue), Europe ($13M), APAC (~$5M), plus smaller South American sales spreads regulatory risks but requires navigating complex trade policies aggravated by geopolitical frictions [S8].

Foreign exchange enters as a meaningful financial variable since revenues mainly denominate in USD/EUR while a sizeable portion of labor cost base is CAD/EUR denominated—currency swings thus affect reported earnings given exposure mainly to CAD/USD fluctuations [S1].

Growth Drivers: Domestic Manufacturing and Market Penetration

A pivotal growth catalyst lies in Senstar’s ongoing localization of core product manufacturing within the U.S., directly addressing tariff pass-throughs affecting components sourced predominantly from China and other parts of Asia-Pac [S1]. This industrial shift is complemented by expanding inventory buffers that mitigate near-term disruptions providing operational resilience against supplier bottlenecks.

Government budgets serve both as a tailwind following pandemic recovery trends increasing security upgrades spending particularly in critical infrastructure sectors such as utilities, transportation hubs, pipelines—a domain well-suited for Senstar’s fiber optic pipeline monitoring technology acquired via Blickfeld GmbH integration completed February 2026 [S17],[S19].

Technology investment continues apace with R&D expenses forecasted at approximately $4.2 million during 2026 focused on product innovations extending sensor performance capabilities alongside enhancements to their integrated Video Management Software (VMS) platforms supporting scalability demands [S6]. Strategic supplier diversification also plays a central role improving cost structures enhancing gross margins over time.

Risks and Headwinds: Trade Policies and Supply Vulnerabilities

Heightened geopolitical tensions underpin principal risks including unpredictable modifications to U.S.-imposed tariffs targeting industrial goods alongside retaliatory duties from European Union members threatening cross-border trade fluidity [S1],[N1]. These factors inherently raise input costs potentially squeezing margins absent offsetting price adjustments constrained by competitive market dynamics.

Supplier concentration notably in China exposes Senstar to both increased lead times amid export restrictions or customs delays plus currency devaluation impacts complicating CAD/USD revenue conversion [S1]. The seasonal nature of project execution dependent on weather conditions combined with government procurement timing variability introduces consistent periodic volatility affecting quarterly earnings predictability.

Prolonged supply-chain interruptions risk slowing innovation cadence indirectly if capital allocation diverts towards inventory buildup rather than R&D. Currency appreciation/depreciation cycles additionally contribute continuous earnings sensitivity particularly given expenses split geographically between North America-Europe-APAC currencies [S1].

Key Milestones and What to Watch Next

Stakeholders should monitor forthcoming quarterly releases for explicit Q2 2026 guidance updates clarifying presumed benefits from domestic production scalability gains alongside disclosure of new contract wins especially large-scale government infrastructure projects within North America facilitating backlog visibility [S2],[N2].

Progress regarding patent applications related to proprietary sensor designs will also be relevant for competitive moats enhancement. Observers should note capital expenditure plans focused on manufacturing line enhancements signaling operational execution capability familiarization with domestic suppliers.

Currency hedging initiatives if any will be pertinent given operating earnings exposure to FX volatility.

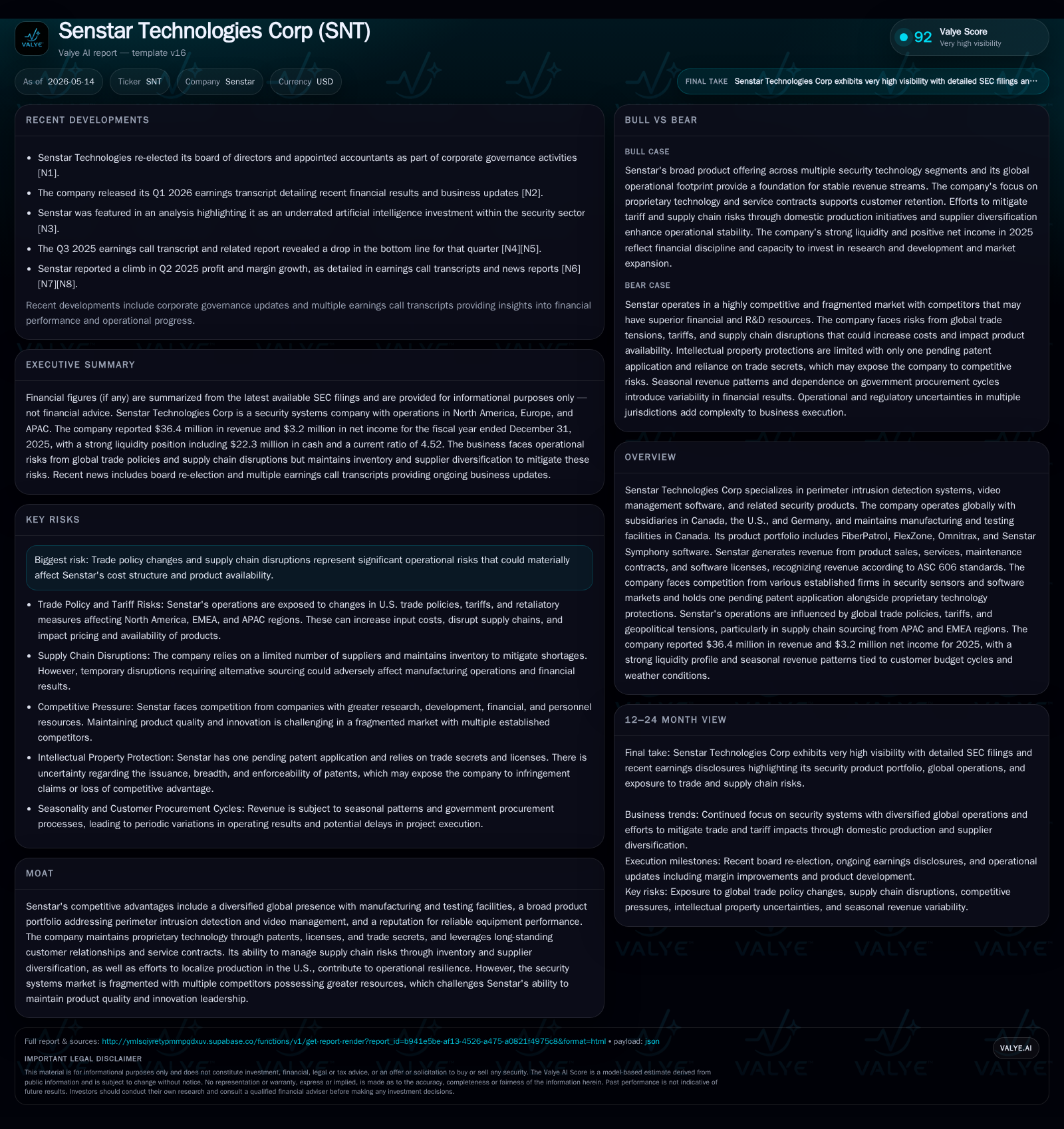

Financial Snapshot: Strengthening Liquidity and Profitability

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $22mm | |

| 2025-12-31 | ||

| Current assets | $41mm | |

| 2025-12-31 | ||

| Current liabilities | $9mm | |

| 2025-12-31 | ||

| Current ratio | 4.52x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period End |

|---|---|---|

| Revenue | 36,374,000 | |

| 2025-12-31 | ||

| Operating Income | 3,010,000 | |

| 2025-12-31 | ||

| Net Income | 3,217,000 | |

| 2025-12-31 | ||

| Cash & Equivalents | 22,341,000 | |

| 2025-12-31 | ||

| Current Ratio | 4.52 | |

| 2025-12-31 |

Despite mounting external pressures, Senstar maintains solid profitability supported by revenue growth reaching $36.4 million in fiscal year 2025 reflecting steady operational execution [F1]. Operating income remained positive at just over $3 million while net income sustained at $3.2 million underpinning bottom-line stability even amid competitive headwinds. The firm’s liquidity position is robust with over $22 million in cash reserves coupled with a strong current ratio of 4.52 reflecting comfortable short-term balance sheet cushioning facilitating investments into supply chain transformation projects without resorting to external financing [F1],[S2].

These financial fundamentals provide a credible foundation supporting the company’s strategic roadmap moving into calendar year 2026 amidst evolving market dynamics.

Disclaimer: This analysis is based solely on publicly available information from SEC filings dated up to May 2026 along with company disclosed earnings transcripts. It does not constitute investment advice or recommendations but aims to present an objective assessment grounded entirely in cited operating facts without speculative forecasts or valuation opinions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments