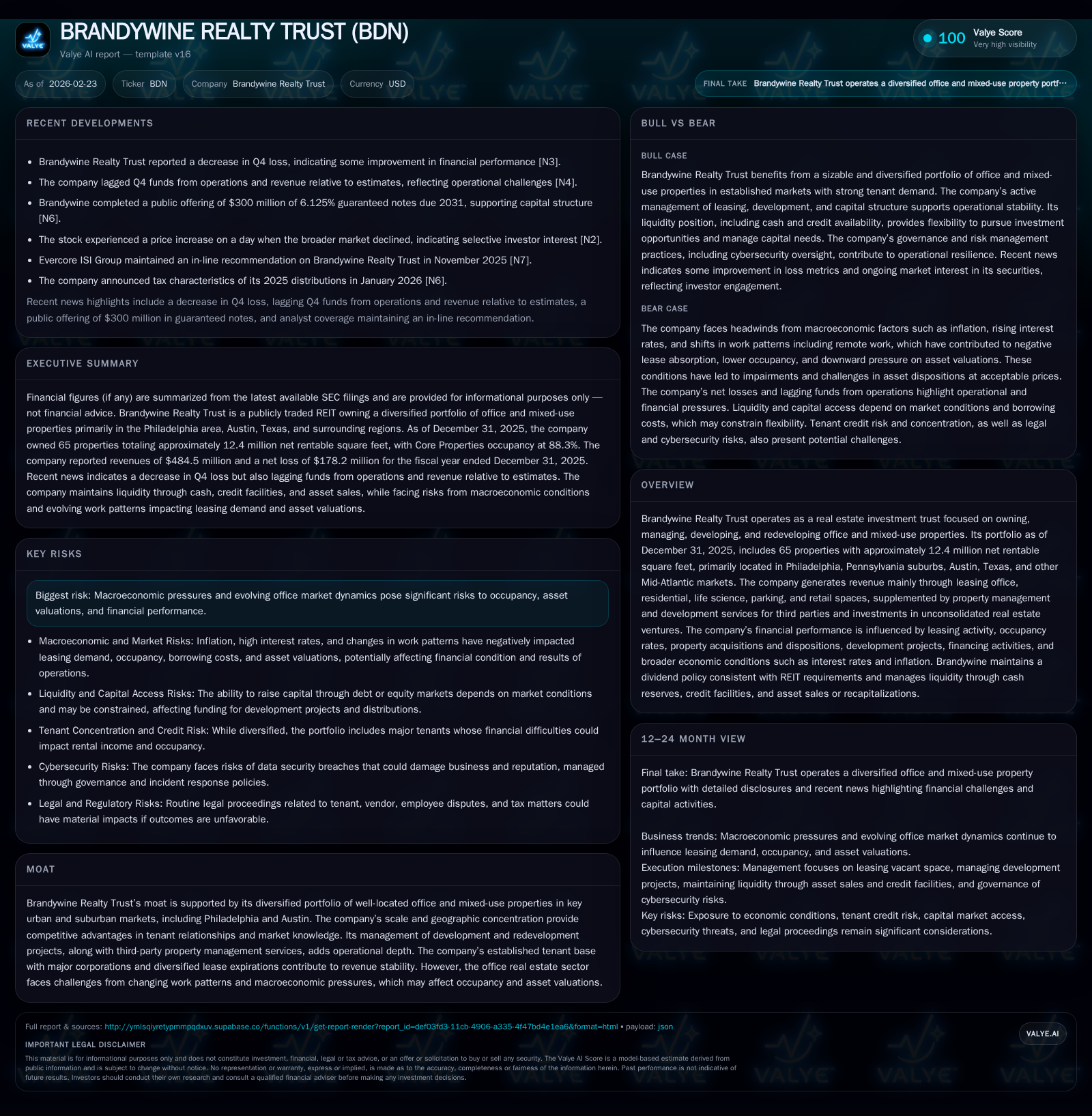

Brandywine Realty Trust’s Winding Path: Balancing Urban Office Assets and Market Pressures

Brandywine Realty Trust manages a geographically concentrated office and mixed-use portfolio while contending with macroeconomic challenges impacting leasing and valuations.

Brandywine Realty Trust recorded a 4.2% revenue decline and a halving of operating income in FY 2025, driven by pressures on leasing activity within its core urban office markets. The company’s portfolio, concentrated in Philadelphia and Austin, displays stabilized occupancy near 88%, supported by diversified lease structures and active redevelopment projects. Capital structure refinements, including debt repayments and new issuances, enhance liquidity but credit rating downgrades raise financing costs. Dividend payouts remain aligned with REIT obligations, though operational cash flow contraction warrants close monitoring. Key risks include evolving office demand patterns and inflation-driven expense pressures, with future performance hinging on leasing renewals and development stabilization.

Historical Financial Trajectory: Revenue and Operating Income Dynamics

Brandywine Realty Trust's financial results over the past four fiscal years reveal a trajectory shaped by the ebb and flow of commercial real estate fundamentals amid rising macroeconomic headwinds. In FY 2025, revenues contracted by approximately 4.2% YoY to $484 million from $506 million in the prior year period [F1]. This decrease mirrors subdued leasing momentum across its key office markets as enterprises cautiously recalibrate space needs.

Operating income registered a steeper decline, halving to $26.7 million in FY 2025 from nearly $54.9 million the prior year — a stark 51% reduction that underscores margin compression pressures attributable to increased tenant installation costs and upkeep expenses unrecouped through leases [F1]. The pronounced swing from a $21.6 million operating loss reported in FY 2023 toward operating profitability by FY 2024 was thus partly reversed.

Net income remains negative but showed modest improvement: losses eased 9% to $178 million compared to FY 2024's -$196 million figure, reflecting impairments related primarily to certain consolidated joint ventures balanced against operational gains [F1]. The persistence of losses signals ongoing valuation challenges within the office sector.

Operating cash flow (CFO) experienced a material contraction of over one-third (-35.6%), amounting to roughly $117 million for FY 2025 compared with $181 million in FY 2024 [F1,S26]. Reduced collections, higher capital expenditures for tenant improvements, and elevated maintenance contributed to this squeeze.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 484 | -178 | 117 | 27 | -4.2% | +9.0% |

| 2024 | 506 | -196 | 181 | 55 | -1.8% | +0.4% |

| 2023 | 515 | -197 | 177 | -22 | +1.7% | -465.6% |

| 2022 | 506 | 54 | 209 | 120 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -22.5 |

| 2024 | -18.9 |

| 2023 | -14.9 |

| 2022 | 3.3 |

Source: SEC companyfacts cache [F1].

Note: Capex data insufficient for multi-year trend inclusion; ROE not directly reported but implied negative given net losses vs equity base

Portfolio Composition and Occupancy: Drivers of Past Performance

Brandywine maintains a focused portfolio concentrated largely within high-demand urban and suburban corridors anchored by Philadelphia's central business district (CBD), Austin markets, and neighboring Mid-Atlantic regions [S1]. As of December 31, 2025, the firm owned sixty operational properties totaling approximately 11.3 million net rentable square feet (NRSF) spanning predominantly office (56) with four mixed-use assets that blend residential, life sciences, retail, and parking components.

The portfolio exhibits solid stabilized occupancy levels near 88%—notable given widespread office sector softness nationally—supported particularly by marquee assets such as Cira Center (730k NRSF at ~94%) and flagship properties along Arch Street commanding occupancy above the high-80s percentile range [S1]. The presence of multitenant leases with fixed or CPI-indexed annual escalations mitigates inflation exposure while underpinning revenue stability despite rising property operating costs.

Development activity further bolsters value creation potential; three projects reside in various stages of development or redevelopment—with emphasis on tactical densification or upgrading for evolving tenant requirements—and two recently completed properties are poised for stabilization [S1]. These initiatives acknowledge changing office utilization dynamics by incorporating flexible workspaces and amenities targeted at life science tenants—a sector displaying more resilient demand curves.

Recent Earnings Highlights and Market Reactions

The Q4 earnings announcement for FY 2025 revealed results trailing consensus estimates on both Funds From Operations (FFO) metrics and revenues [N1], which triggered heightened share price volatility despite some optimism expressed regarding operational resilience in concentrated markets [N3]. Concurrently, Brandywine reported a reduced net loss versus the previous quarter partially attributable to lower impairment charges recorded earlier in the year [N4].

Investor sentiment appeared bifurcated: concerns over macro-driven softness tempered enthusiasm while recognition of management's proactive capital allocation garnered cautious approval.

Growth Outlook: Development Projects and Leasing Environment

Management commentary highlights ongoing commitment toward completing existing development/remodeling projects intended to enhance asset class mix efficiency and tenant appeal across its portfolio [N6,S6]. Leasing environments are characterized by challenging renewals influenced by remote work persistence which depresses demand yet open opportunities for flexible contract structures.

Heightened tenant installation costs combined with modestly lower leasing spreads suggest growth headwinds will persist through near term before normalization potentially emerges once newer assets stabilize occupancy rates sufficiently [S9]. Innovation within mixed-use offerings—integrating life sciences spaces with residential—represent tactical responses aimed at tapping into robust sub-market segments not uniformly affected by traditional office market volatility.

Capital Structure Evolution and Liquidity Position

Brandywine prudently managed its capital structure over the trailing period evidenced by full repayment of its $245 million secured facility ahead of maturity in October 2025 alongside issuance of several unsecured notes aggregating over $1 billion due between late-2027 through early-2031 horizons . This refinancing strategy shifted overall debt weighted-average cost upward modestly (to approximately 6.3%), reflecting tightening credit conditions amplified by rating agency downgrades incurred through mid-2023 that pushed senior unsecured notes into speculative-grade territory (Ba2 Moody’s; BB+ S&P) with associated interest rate step-ups affecting note coupons on outstanding tranches [S17].

The company's liquidity position remains well-supported with unutilized revolver capacity exceeding $560 million net of letters of credit plus approximately $32 million cash on hand at year-end contiguous with expected operating cash inflows sufficient for upcoming maturities coverage under current assumptions [S8,S9]. Covenants consistently monitored remain compliant including leverage caps below stipulated ratios (~0.60x leverage ratio limit) preserving financial flexibility.

Dividend Policy, Share Buybacks, and Shareholder Returns

Dividend payments conform strictly with REIT distribution requirements; though explicit payout ratios relative to FFO were not provided externally, disclosures indicate distributions surpass minimum taxable income thresholds requisite for maintaining federal REIT status [F1,N2,N6]. No recent share repurchase activities were reported suggesting that limited free cash flow since peak years has constrained excess return pathways beyond dividends.

The company's dividend policy shows consistency but faces pressure from compressed operating cash flows which have contracted markedly since earlier periods; continuous reassessment tied to leasing success rates and cost control remains critical for sustainable shareholder returns without dilutive equity issuances.

Key Risks from Market Trends and Operational Factors

Crucial risks emerge from macroeconomic volatility notably rising interest rates elevating borrowing costs alongside inflationary headwinds inflating property operating expenses beyond recoverable pass-throughs under triple net lease frameworks impairing margins further [S1]. Remote work trends persistently challenge fundamental office demand reducing absorption velocity causing potential longer-term vacancies or downward pressure on rental rates.

Compounding these are cybersecurity risks—although governance around IT security appears robust featuring quarterly board oversight reports from an experienced Chief Technology & Innovation Officer tasked explicitly with incident response policies—any material breach could erode stakeholder trust or lead to regulatory ramifications impacting operations [S1].

What to Watch: Milestones and Indicators for Future Performance

Looking ahead (analysis), investors should monitor key operational indicators such as:

- Renewal rates and spreads on existing leases especially within newly redeveloped mixed-use components,

- Occupancy stabilization milestones for properties recently completed or placed into redevelopment pipeline,

- Access to capital markets reflecting cost-of-debt trajectories amid fluctuating credit ratings,

- Maintenance or changes in dividend distribution levels versus FFO stability,

- Tenant installation cost trends against recovered expense reimbursements,

- Progress updates on innovation-driven mixed-use projects adapting to market demand shifts.

These metrics will collectively validate management's strategic navigation balancing core urban asset stewardship against pervasive sector headwinds impacting Brandywine Realty Trust's trajectory moving forward.

Disclaimer: This analysis is provided solely for informational purposes without any recommendation regarding buying or selling securities related to Brandywine Realty Trust.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments