Ranger Gold Corp. Confronts Capital Constraints While Pursuing Mining Property Acquisitions

Ranger Gold remains an exploration-stage gold mining company with no revenues or assets, reliant on capital infusions and due diligence to break ground.

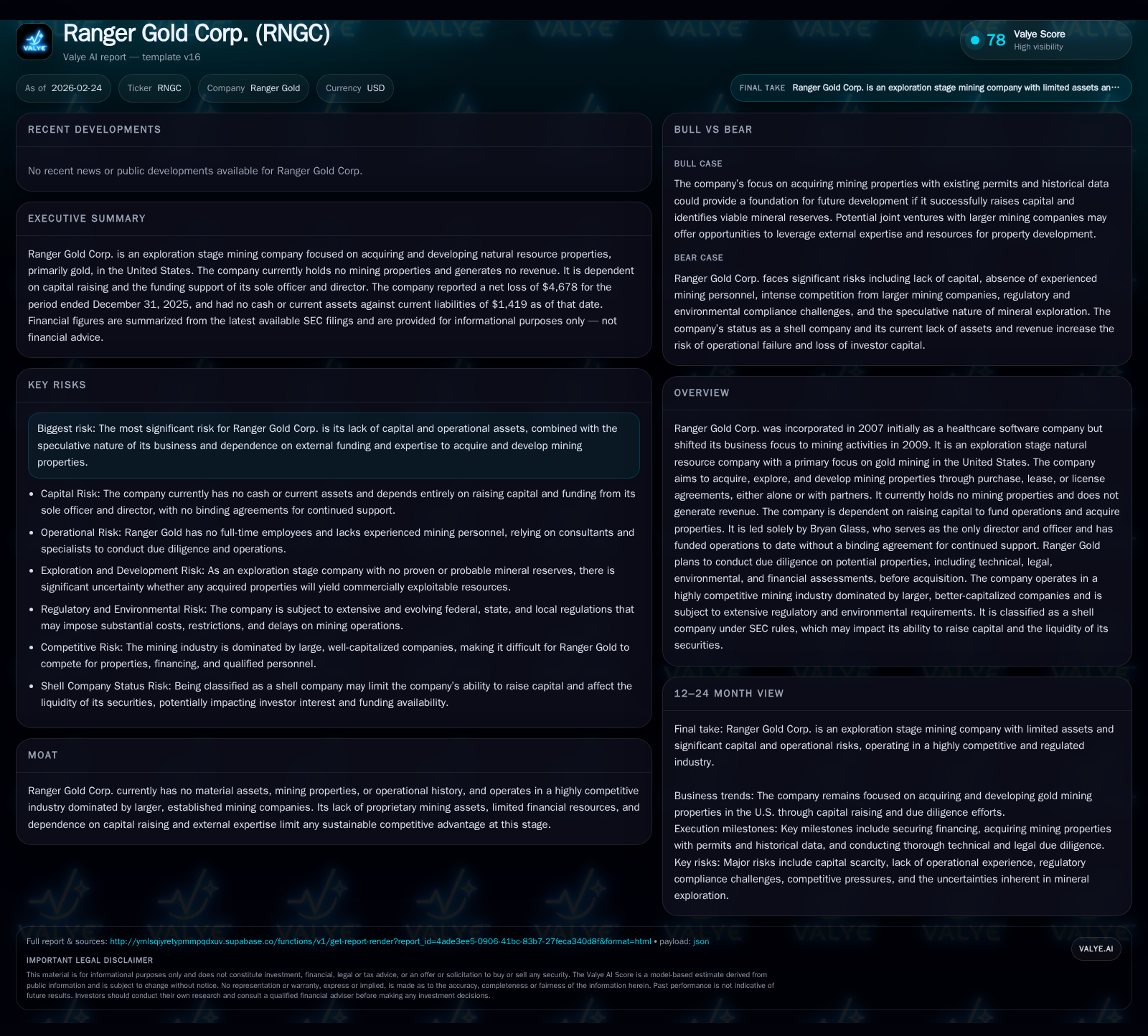

Ranger Gold Corp. shifted from healthcare software to gold mining in 2009 and currently holds no mining properties or operational history. The company depends entirely on raising capital to pursue acquisitions and conduct due diligence on potential mining properties. Led solely by Bryan Glass, Ranger Gold faces substantial obstacles including lack of experienced personnel, capital constraints, and intense competition from well-established miners. Without material assets or revenues, the company is classified as a shell and exploration-stage entity, with significant regulatory and environmental hurdles ahead.

Company Background and Historical Performance

Ranger Gold Corp., incorporated in Nevada in 2007 initially as Fenario Inc., began as a healthcare software developer focused on proprietary solutions for providers and insurers [S1]. In 2009, upon founder exit, the firm pivoted exclusively to the exploration stage natural resource sector with a focus on gold mining within the United States [S1][S19]. Despite acquiring rights to some mining properties between 2009-2013, Ranger Gold never commenced substantive operations or generated revenues throughout this period or subsequently.

Since 2013, Ranger Gold discontinued SEC reporting until filing for reinstatement in late 2018. The court appointed Bryan Glass custodian of the company in early 2019; he became sole director/officer shortly thereafter while injecting limited funding valued at $20,000 in exchange for stock [S1][S15]. The company was a reporting entity again as of August 2022 but remains categorized as a smaller reporting shell company with no operating assets or income generating activities [S1][S21].

Financially, Ranger Gold has recorded consistent operating losses over recent years (annual operating loss was approximately -$27.8K USD fiscal year-to-date FY2025) [F1]. The company reported zero revenues for all years available (FY2023–FY2025). Net incomes mirrored operating losses accordingly, reaching -$7.7K for FY2025 [F1]. Negative operating cash flows also reflect ongoing expenses consumed by administrative costs and preliminary activities (-$29K CFO FY2025) [F1]. Equity remains negative at -$16.2K USD reflecting accumulated losses greater than contributed capital [F1]. Liquidity is effectively nil with current liabilities surpassing current assets and no disclosed cash reserves.

Historical performance (annual)

| FY | Rev | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | -7716 | -29062 | -27846 | -79.7% |

| 2024 | 0 | -4294 | -47404 | -46321 | +80.0% |

| 2023 | 0 | -21504 | -18261 | -21504 | |

| 2012 | 0 | -100976 | -98717 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 47.5 |

| 2024 | |

| 2023 | 663.1 |

| 2012 |

Source: SEC companyfacts cache [F1].

*Latest annual figures approximate year ended March/December depending on filing.

Note: Dividends paid and share repurchases data are not available in provided tags; thus cannot be reported.

Business Model and Industry Context

Ranger Gold seeks to operate as an active natural resource company by acquiring or leasing mineral rights to explore and develop gold properties primarily within U.S. jurisdictional boundaries [S1][S19][S15]. The company does not plan direct greenfield exploration but prefers acquiring properties where geological surveys, permits, existing mine plans, or historical production data are available [S24]. This strategy intends to reduce exploratory risk by focusing on assets with some precedent of mineralization.

Mining claims may be patented or unpatented public lands regulated under federal statutes such as the General Mining Law of 1872; alternatively private fee lands or tribal lands may be pursued through purchase or lease agreements [S26][S28]. Acquisitions might be sole ventures or joint ventures partnering with larger miners possessing greater operational capacity and capital [S13]. This flexibility is vital given Ranger Gold's constrained access to financial resources.

The precious metals industry is bifurcated between senior producers with global operations managing full-scale mines versus junior explorers like Ranger Gold focused largely on early-stage resource identification and evaluation. Competition for promising claims is fierce; incumbents frequently outbid juniors due to better financing options and established relationships with regulators [S13]. Moreover, compliance demands under environmental regulations such as CERCLA (Superfund), RCRA (waste disposal), CAA (air emissions), CWA (water discharges), plus NEPA’s environmental impact statements create protracted permitting timelines imposing significant cost burdens before projects commence [S4][S8][S20].

Regulatory Landscape and Risks

SEC disclosures highlight substantial regulatory challenges faced by Ranger Gold including:

- Need for multiple federal/state/local permits covering air quality (CAA), water discharge (CWA), waste management (RCRA), groundwater protection (SDWA/UIC), reclamation bonding requirements, endangered species protections among others [S4][S22][S28].

- Potential CERCLA liability exposes owners/operators to costly cleanup obligations even post-closure.

- Permits may impose production limits or require costly mitigation measures undermining economic viability.

- Legal due diligence necessary to confirm title ownerships and avoid encumbrances that could impair operations.

- Capital intensive nature of compliance may delay or prevent acquisitions absent sufficient funding.

Given Ranger Gold’s lack of internal experienced staff, it emphasizes engaging qualified external consultants for geological assessments as well as legal/environmental due diligence prior to acquisition decisions [S24][S25][S28].

Growth Outlook and Milestones

Currently without any producing assets or revenues, Ranger Gold’s growth depends fundamentally on securing capital to fund property scouting and due diligence fieldwork/testing of candidates amenable to economical extraction processes [S6][S15]. Key milestones include:

- Announcement of definitive property acquisitions or binding agreements securing mining rights.

- Completion of qualified person reports assessing proven/probable reserves compliant with SEC definitions critical for financing eligibility.

- Establishment of joint ventures recruiting operational partners possessing development capacity.

- Capital raises targeting exploration budgets.

- Regulatory permit applications signaling progression beyond feasibility stage.

No explicit guidance or timelines have been provided within filings or public disclosures beyond these strategic outlines [N#]. Thus timelines remain speculative pending asset acquisition success.

Capital Structure and Returns Analysis

Financial metrics reveal typical early-stage exploration challenges:

- Negative equity of approximately $16.2K USD as of latest fiscal reporting reflecting accumulated losses exceeding capital contributions [F1].

- Consistent operating losses averaging tens of thousands annually demonstrate ongoing cash burn supporting overhead without productive activity yet realized [F1].

- Negative operating cash flows reinforce reliance on external funding sources absent revenue generation [F1].

- No dividends paid nor share repurchases executed; typical for pre-revenue companies prioritizing cash retention for operations [F1].

- Return on equity calculation is distorted by negative equity but indicates losses rather than profits historically recognized [F1].

Founder Bryan Glass remains sole financier through informal loans/equity infusions without binding commitments posing sustainability risk if support diminishes unexpectedly [S6][S16]. As a shell company subject to resale restrictions under Rule 144 until cessation status confirmed after subsequent filings restricts liquidity for investors holding shares currently [S21].

Overall returns will remain negative until asset acquisition matures into revenue-positive operations—highlighting critical dependency on procedural execution competence coupled with effective capital sourcing ability.

Mining Asset Life Cycle Considerations

Mining companies typically progress through long life cycles starting from identification through exploration drilling defining resource quantities (inferred → indicated → measured categories), moving into reserve classification (probable → proven) per SEC guidelines before development permits issuance allows construction/production phases. Expenses incurred pre-reserve confirmation must be expensed affecting financial statements adversely until sustainable production yields positive EBITDA results [S14]. Ranger Gold is wholly immersed within this stage emphasizing need for geological rigor alongside economic feasibility studies factoring metallurgical recovery rates — vital to determine cut-off grades justifying profitable processing investments.

Successful junior miners create value by upgrading resource confidence enabling improved capital market access or joint venture partnerships bringing scale economies and technical know-how absent internally today at Ranger Gold.

Summary Judgment: Critical Dependencies Define Path Forward

Ranger Gold exemplifies early-stage explorers facing classic uphill battles:

- No owned mineral properties,

- Null revenues,

- Minimal liquidity,

- Single-person leadership,

- Intensive environmental/legal compliance burdens,

- Fierce competition favoring deeper-pocketed players. Its business model focuses on meticulous property selection enabled by professional external due diligence prior to acquisition—reflecting prudent risk mitigation but delaying near-term optionality realization. Financial sustainability hinges heavily upon founder commitment alongside successful external fundraising initiatives which remain uncertain without verified resource-based assets underpinning credible mine plans advancing toward production milestones. Investors should note that without demonstrable mined reserves or recurring cash flows within foreseeable horizons operational viability remains speculative.

Disclaimer: This analysis relies strictly on publicly available SEC filings up to February 2026 without extrapolation beyond provided data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments