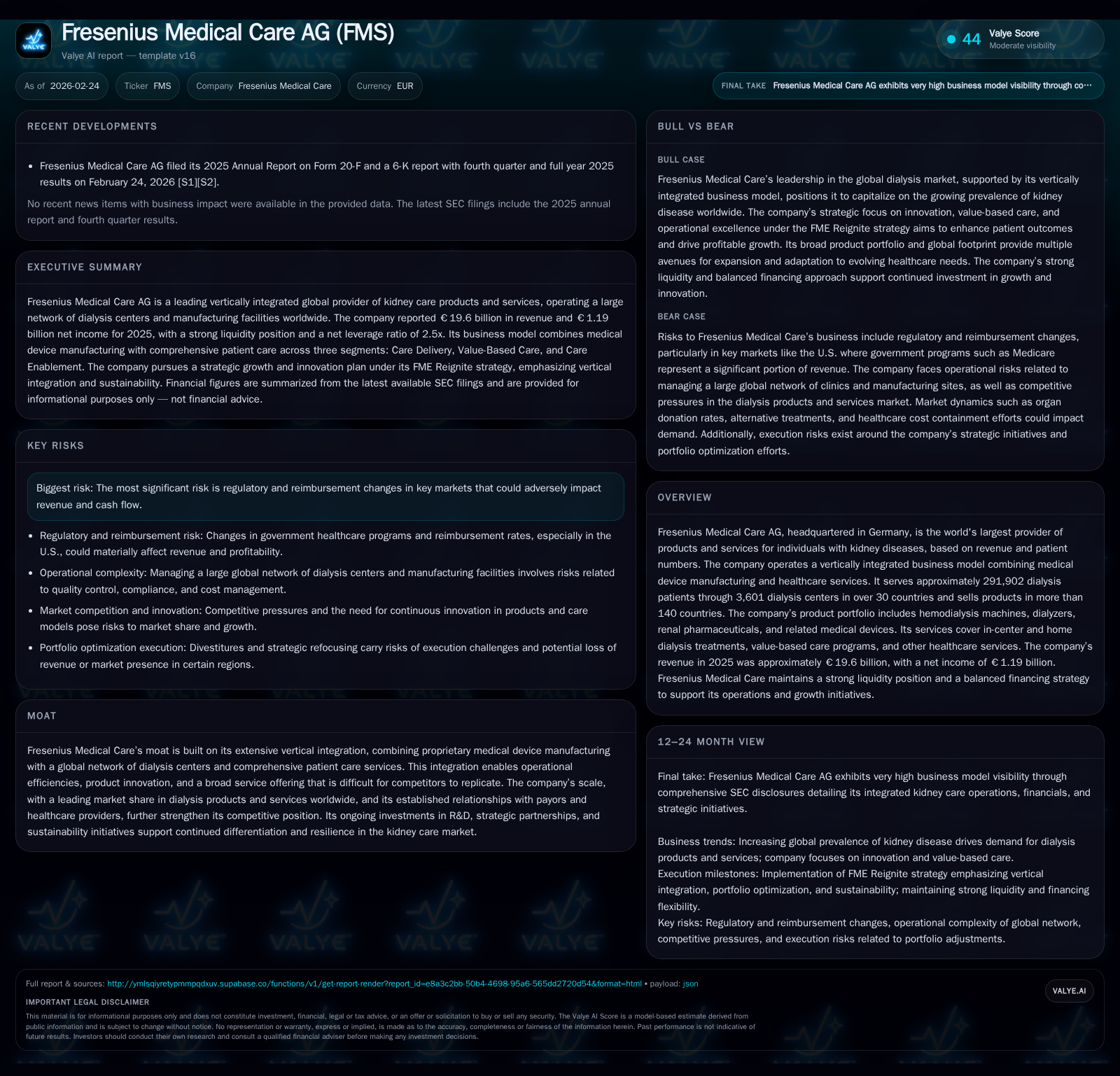

Fresenius Medical Care's Strategic Shift and Resilience in Kidney Care Markets

Examining Fresenius Medical Care’s financial evolution, integrated business model, and emerging growth drivers amid a complex regulatory landscape.

Fresenius Medical Care AG stands as the dominant global player in kidney care, leveraging its unique vertically integrated model that combines product manufacturing with extensive dialysis services. Over recent years, the company has exhibited steady revenue and profit growth driven by expanding patient volumes and innovation. Its strategic pivot toward value-based care programs introduces both substantial opportunity and risk, especially under shifting reimbursement frameworks. Capital allocation remains disciplined with solid free cash flow supporting dividends and operational investments. Regulatory uncertainties, especially around government payor policies, present ongoing challenges for Fresenius’s future growth trajectory.

Historical Performance and Growth Drivers

Fresenius Medical Care’s financial trajectory from 2013 through 2016 showcases a resilient expansion fueled primarily by increases in dialysis patient volumes—driven by demographic trends such as aging populations and rising chronic kidney disease incidence—as well as steady gains in its product sales worldwide [F1]. Revenues grew from approximately $5.0 billion in FY2013 to about $4.6 billion by FY2016 when measured for the latest quarterly point ending September; note that exact fiscal year-end comparisons need careful currency adjustment due to differing standards.

Operating income advanced with a compound annual growth rate (CAGR) near the mid-single digits but net income exhibited more pronounced improvement—with a 20.8% jump in 2016 over prior year—reflecting enhanced operational leverage and disciplined expense management amid scaling operations.

Operating cash flow also reflected robust health post-2013 troughs, rising over approximately $2.1 billion by FY2016. Capex steadily scaled alongside these flows to support capacity expansions across manufacturing facilities and dialysis centers. Approximate return on equity stabilized near 11.5%, indicative of efficient capital deployment relative to accumulated equity base.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2016 | 1243 | 2.1 | 2.6 | +20.8% | ||

| 2015 | 1029 | 2.0 | 2.3 | -1.5% | ||

| 2014 | 5.3 | 1045 | 1.9 | 2.3 | +5.9% | -5.8% |

| 2013 | 5.0 | 1110 | 2.0 | 2.3 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2016 | -277 | 1110 | 11.5 |

| 2015 | -263 | 1007 | 10.4 |

| 2014 | 318 | 930 | 11.1 |

| 2013 | 296 | 1287 | 12.0 |

Source: SEC companyfacts cache [F1].

Note: Revenue specific YoY comparisons unavailable for some years due to different tag periods.

These results reflect Fresenius’s ability to capitalize on global dialysis demand expansion factors, including shortage of transplant organs and increased survival rates among chronic disease patients requiring renal replacement therapy.

Vertical Integration: Core Moat and Competitive Edge

Fresenius Medical Care’s moat derives fundamentally from its vertically integrated platform that marries proprietary manufacturing of hemodialysis machines, dialyzers, renal pharmaceuticals, and related products directly with ownership and operation of a global network of over 3,600 dialysis centers serving nearly 292,000 patients across 30+ countries [S13]. This integration enables tightly coupled supply chain optimization—ensuring timely availability of consumables like bloodlines and concentrates tailored precisely for clinic needs—while synchronizing clinical outcomes alignment through standardized protocols embedded within its service offerings.

This operational synergy affords Fresenius differentiated pricing power as the company controls critical supply inputs along with complemented value-added services such as home dialysis training and vascular specialty care . The scale further accelerates innovation feedback loops—from product R&D leveraging real-world patient data—to rapid iteration on device performance enhancing dialyzer efficacy metrics.

Such integration complicates competitive entry barriers because standalone manufacturers or independent service providers lack Fresenius’s end-to-end control over technology development combined with direct patient access points—an advantage reinforced by long-term payor contracts shaped by clinical quality measures.

Value-Based Care Programs as a Growth Vector

A pivotal shift in Fresenius’s business model is the growing emphasis on value-based care programs structured around shared risk or full-risk capitation contracts with private payors and government entities such as Medicare/Medicaid in the U.S., accounting for a material portion of revenues particularly within the Value-Based Care segment [S1]. Under capitation, Fresenius receives fixed monthly payments per member (Member Months), effectively betting on managing total medical costs below premium revenue while achieving quality benchmarks.

This model hinges on sophisticated clinical cost management capabilities since losses can occur if medical expenses exceed fixed fees—highlighting intrinsic risk/reward tradeoffs absent in traditional fee-for-service setups [S1]. Membership growth signals higher potential revenue pools; however managing profitability demands tight cost control across hospitalization rates, medication use, outpatient service utilization, and preventive care effectiveness.

Shared savings arrangements add complexity as Fresenius shares upside profits generated by reducing overall expenditures but equally bears downside exposure if targets are missed—a structure requiring advanced population health management infrastructure enabled by integrated data platforms.

From an industry lens, embracing capitation aligns Fresenius with broader healthcare system reform trends shifting toward accountability for holistic patient outcomes but requires careful execution due to variability in payer program designs and regulatory oversight regimes.

Regulatory Environment and Reimbursement Risks

The highly regulated nature of kidney care delivery exposes Fresenius to substantive risks arising from reimbursement changes—the single largest external factor impacting revenue sustainability . Public programs like Medicare substantially influence U.S.-based dialysis treatment payment levels; any declines or tightening coverage criteria could materially impair revenue streams.

Further complicating the outlook are compliance requirements across multiple jurisdictions involving licensing, environmental controls linked to waste disposal from dialysis operations, anti-corruption statutes such as the Foreign Corrupt Practices Act (FCPA), and increasing scrutiny through whistleblower litigation challenging billing practices or contractual performance [S10,S11,S14,S19,S21,S24].

Moreover, macroeconomic uncertainties coupled with geopolitical events affect financial markets impacting both government budgets allocated for healthcare funding and private payor behaviors [S18,S19]. Payment delays or disputes amplify working capital pressures given substantial accounts receivable denominated under public payor schedules.

Mitigating these risks demands proactive regulatory monitoring combined with diversified geographic deployments reducing dependence on any single market while investing in compliance frameworks enabling agile responses.

Capital Structure, Liquidity, and Financing Strategy

As of year-end 2025 filings, Fresenius Medical Care maintained strong liquidity totaling approximately €1.6 billion in cash alongside €3.3 billion undrawn credit facilities—including a €2 billion syndicated credit line reserved primarily as backup funding—illustrating well-laddered debt maturity profiles extending into 2032 ensuring refinancing stability .

The company employs an active financial risk management approach featuring hedging against foreign exchange volatility (relevant given global footprint spanning >140 countries), interest rate exposures tied to bond issuances denominated in both euros and U.S dollars [S8,S14]. Net leverage ratios have been managed within self-imposed targets ranging between 2.5x-3x adjusted EBITDA levels as disclosed for FY2025 (~2.5x) reflecting balanced conservative debt policy consonant with steady free cash flow generation ambitions.

Capital Allocation: Capex, Dividends, and Buybacks

Capital expenditures have incrementally increased reaching roughly €915 million gross in 2025 focused principally on expanding production capacity (including acquisition of formerly leased facilities), new clinic development under Care Delivery segment as well as investment into Care Enablement technology assets underpinning global MedTech umbrella operations [S7,S12,S17]. This represented about 5% of total revenue that year (up from ~3-4% earlier), signaling an intensification of innovation capital deployment aimed at sustaining competitive differentiation while maintaining clinical quality improvements.

Operating cash flows remain robust (~$2.14 billion FY2016 equivalent), enabling free cash flow consistently above $1 billion after accounting for capex commitments [F1]. Dividend payout policies have demonstrated upward momentum with recent distributions approximating €416 million planned for payment covering fiscal year 2025 reflecting sound shareholder return focus balanced with investment needs [S8,F1]. Share repurchases lack explicit current quantitative disclosure though longstanding buyback authorizations provide flexibility for returning excess capital subject to evolving strategy [S1].

ROE approximated at ~11.5% aligns favorably within med-tech healthcare sector peers indicating competent capital efficiency deployment amidst careful cost management.

Near-Term Milestones and What to Watch

Investor attention should center on reported metrics emerging from the Value-Based Care segment—especially Member Months enrolled under risk sharing models—as they presage topline trajectory shifts given their outsized revenue potential contingent upon effective cost containment success rates [N3,N5,S1]. Further monitoring of operating margin expansions facilitated through risk contract scaling will offer early clues regarding margin sustainability improvements beyond traditional fee-for-service earnings bases.

Additional KPIs include chronic kidney disease prevalence trends globally affecting patient pool expansion rates alongside legislative policy developments impacting Medicare reimbursements particularly regarding bundled payments or executive order influenced models modifying ESRD coverage [S1,S18].

Ongoing Legacy Portfolio Optimization initiatives signal focus disposal of non-core assets enhancing balance sheet robustness albeit needing confirmation via quarterly filings whether target disposal pace sustains steady cash inflows supporting reinvestment priorities [S17].

Outlook on Innovation and Market Expansion

Research & Development remains cornerstone investing vehicle underpinning Fresenius’s vision targeting comprehensive renal care innovations spanning advanced hemodialysis machines featuring AI-enhanced capabilities to optimize ultrafiltration dynamics along with novel renal pharmaceuticals addressing comorbid conditions prevalent among ESRD patients [S7,S12,S17]. Digital health integration emerges as a potent enabler for remote patient monitoring enabling better adherence tracking critical under home dialysis therapies.

Geographically, developing markets present fertile growth avenues fueled by rising living standards facilitating greater access to life-saving interventions previously unaffordable or unavailable[S13]. Strategic penetration plans entail localized clinic rollouts backed by scalable supply networks leveraging modularity inherent within vertically integrated architecture allowing rapid adaptation tailored to regional clinical demand specifics.

Operational efficiencies derived from FME Reignite strategy including centralization efforts through Care Enablement are expected to consolidate fragmented legacy functions enhancing cost synergies while permitting accelerated innovation cycles targeted at sustaining leadership positions globally into the next decade [S17].

This analysis synthesizes Fresenius Medical Care AG’s documented historical performance data alongside contemporaneous management disclosures without issuing investment advice or price forecasts. It aims to provide internal stakeholders with a nuanced understanding of key operational levers, sector-specific dynamics affecting resilience amid evolving regulatory landscapes, plus capital deployment considerations underpinning sustained value creation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments