BAB, Inc.: Sustaining Franchise Growth Through Multi-Brand Synergies

An examination of BAB, Inc.’s franchising model leveraging Big Apple Bagels and My Favorite Muffin brands amid a competitive quick service retail landscape.

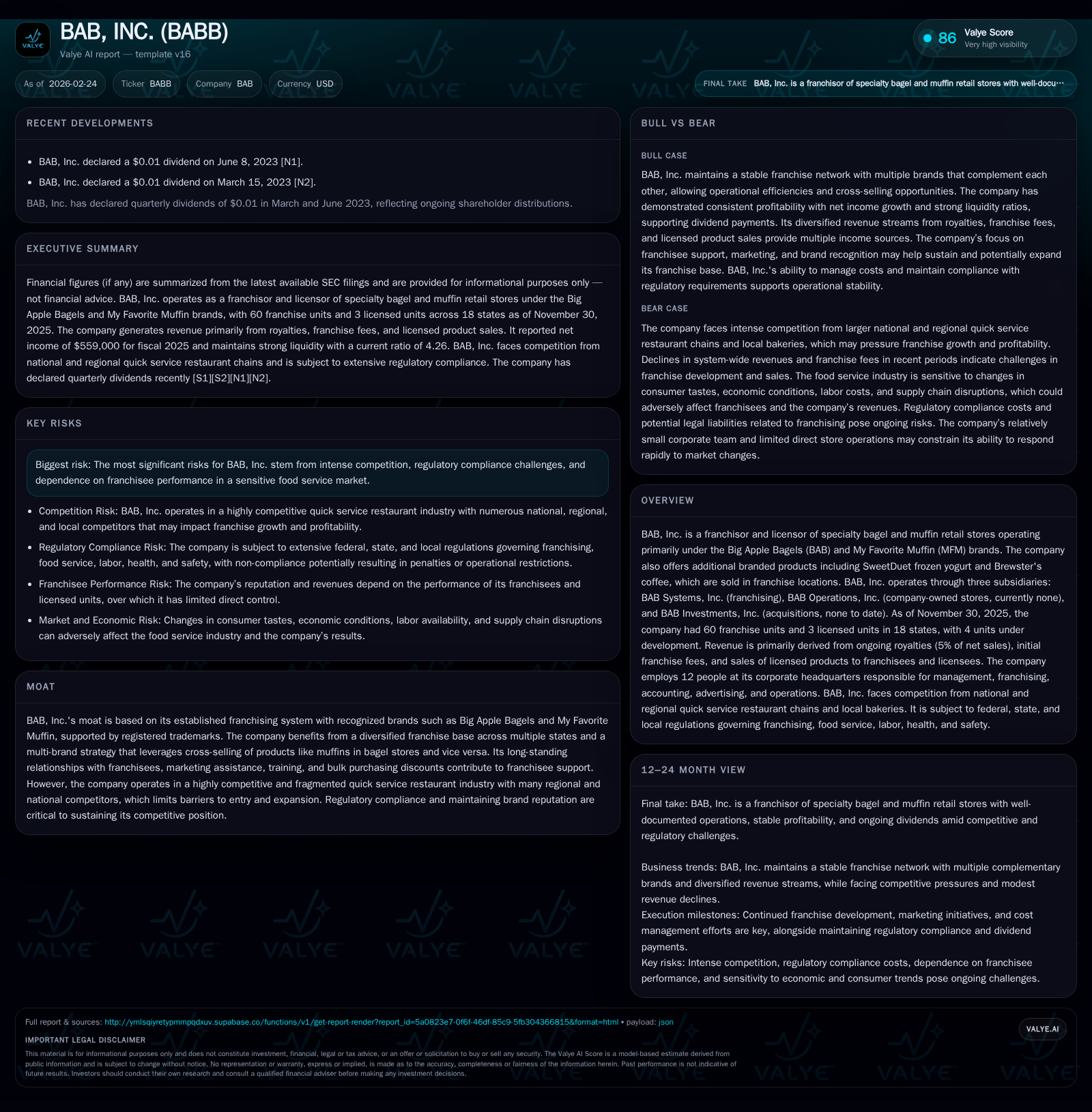

BAB, Inc. operates a multi-brand franchise system centered on Big Apple Bagels and My Favorite Muffin outlets, deriving primary revenue from franchise royalties and licensing fees. Despite modest contraction in system-wide revenues and franchise unit counts, operational leverage has fueled an 8.5% operating income increase in the latest fiscal year. The company’s growth strategy hinges on cross-selling synergies among its bakery and beverage brands while navigating intense competition and regulatory compliance costs. Financially, BAB maintains strong liquidity, steady dividends, and disciplined capital allocation with limited capex and no acquisitions to date.

Historical Performance and Revenue Drivers

BAB, Inc.’s financial foundation is built on the franchisor/licensor model primarily comprising the Big Apple Bagels (BAB) and My Favorite Muffin (MFM) brands. These brands bundle specialty bakery items such as bagels and muffins alongside complementary beverage lines including Brewster's coffee and SweetDuet frozen yogurt. As of November 30, 2025, BAB franchised 60 locations and licensed an additional 3 units across 18 states with four more units under development [S1],[S10].

Revenue is dominated by royalty income—constituting a fixed 5% fee on franchisees’ net retail and wholesale sales—while initial franchise fees and licensed product sales contribute supplementary streams [S2]. In FY2025, BAB reported $721k of operating income on revenues just over $2.17 million [F1]. This reflects a YoY revenue contraction of -2.1% from FY2024 totaling approximately $2.22 million yet an operating income increase of +8.5%, evidencing operational leverage within the franchising system despite flat or slightly declining system-wide sales [S1],[F1]. Net income rose by roughly +6.4% to $559k in FY2025.

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 559044 | 414388 | 721632 | +6.4% |

| 2024 | 525200 | 637753 | 665294 | +12.4% |

| 2023 | 467321 | 534366 | 614773 | +8.2% |

| 2022 | 431992 | 135044 | 607767 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | ROE% |

|---|---|---|

| 2025 | 435810 | 16.1 |

| 2024 | 363175 | 15.7 |

| 2023 | 363175 | 14.7 |

| 2022 | 290541 | 14.0 |

Source: SEC companyfacts cache [F1].

Note: Capex data is insufficient in recent years; omitted from YoY calculations [F1]

The company's capability to increase profitability amid modest revenue declines likely stems from disciplined cost control measures including reductions in marketing fund expenses and professional services observed in quarterly filings [S7],[S12]. Royalty revenues remain stable due to sticky underlying unit economics but are capped by plateauing store counts.

Expanding Footprint: Multi-Brand Strategy and Cross-Selling Initiatives

BAB exploits a multi-brand vertical integration strategy beyond core bagel sales through its ownership/franchising of the MFM brand alongside supplementary beverage products under Brewster's Coffee and SweetDuet frozen yogurt lines [S1],[S3]. This cross-merchandising allows BAB to embed muffin assortments within BAB stores while introducing bagel options into MFM cafes.

These synergies enhance average unit volume potential at franchise locations by broadening consumer appeal without necessitating separate outlets [S10]. The company does not promote Brewster’s as independent franchises; rather it leverages retail distribution through existing franchisees ensuring incremental licensing revenue with minimal capital investment.

This approach addresses broad sector challenges where fragmentation drives fierce competition among specialized quick-service providers vying for overlapping customer bases [S6]. By distributing multiple complementary product lines within each location footprint—averaging around ~1800 sq ft with seating for about 20–30 patrons—BAB aims to maximize per-unit sales efficiency while reducing customer churn risk through diversified menus [S3].

Industry analysis also notes that system-wide sales stability coupled with multi-brand vertical integration fosters resilient royalty streams which can better withstand localized competitive pressures or shifting consumer tastes that impact singular product categories.

Competitive Landscape and Regulatory Risks

BAB faces intense competition from established multi-unit restaurant chains specializing in bakery-cafe formats including Einstein Bros Bagels, Bruegger’s Bagel Bakery, Panera Bread Company as well as supermarkets catering fresh and frozen bakery goods [S6]. These competitors benefit from higher brand recognition or larger marketing budgets which compress BAB’s ability to expand without aggressive investment.

Additionally, market entry barriers remain low due to moderate startup costs typical of quick-service bakery outlets limiting BAB’s protective moat largely to brand equity and franchisee relationships rather than scale advantages [S6]. Maintaining consistent product quality across its geographically dispersed franchises is critical given potential adverse publicity risks inherent in foodservice industries.

Regulatory obligations impose further constraints including compliance with FTC’s Amended Franchise Rule mandating detailed disclosure via Franchise Disclosure Documents (FDD), state-specific franchising laws requiring registration or approval prior to offering franchises locally as well as various health safety inspections tied to food preparation licensing [S21],[S28]. Failure in maintaining these standards may expose the company to penalties or litigation risk adversely impacting brand reputation.

Labor cost inflation amid minimum wage hikes along with food ingredient supply volatility driven by weather or pandemic disruptions additionally pressure operators on margins indirectly affecting BAB’s royalty base performance [S6],[S21]. Although BAB trusts its stringent corporate oversight supports compliance efforts effectively across all units with strong employee relations at headquarters [S28], these external factors persist as strategic headwinds.

Financial Health: Profitability and Cash Flow Dynamics

Despite modest revenue contractions (-2.1%), BAB boosted operating income by +8.5% in FY2025 to roughly $722k reflecting ongoing operational efficiency improvements rooted partly in cost structure optimizations noted during quarterly reviews [F1],[S7]. Net income aligned upwards (+6.4%) at $559k corroborating effective expense management.

However, operating cash flow declined sharply by approximately -35% year-over-year to $414k indicating possible working capital inflation or timing differences between earnings recognition and cash collections [F1],[S7]. This divergence highlights the importance of scrutinizing noncash adjustments such as deferred taxes or uncollectible accounts provisions documented during management commentary phases [S7],[S17].

Balance sheet robustness is evident through a strong current ratio exceeding 4x driven by current assets near $2.5 million outpacing liabilities close to $0.59 million as of late FY2025 suggesting sound short-term liquidity positioning supporting business continuity under fluctuating environments [F1].

Estimated return on equity approximates at ~16%, indicating satisfactory profitability relative to shareholder capital without reliance upon leverage given negligible debt references throughout financial disclosures [F1],[S4],[S7]. This return profile aligns with typical asset-light franchisor models that capitalize on fee-based revenue streams granting efficient equity utilization.

Specialized Terms Analysis:

- Operating leverage is evidenced where fixed overhead absorption improves profit margins despite flat revenues.

- Working capital fluctuations may stem from deferred recognition practices linked to royalty accrual estimations.

- Free cash flow post-capex remains positive though capex is minimal reflecting maintenance investments rather than expansionary spending owing to franchise model nature.

Capital Deployment: Dividends, Buybacks, and Investment Outlook

BAB employs a conservative capital allocation philosophy prioritizing steady dividends over share repurchases or acquisition activity {not evidenced in records} marking an absence of buyback programs thus far since incorporation of the Investments subsidiary in 2009 has yielded no transactions [S1],[F1],[S28]. Dividends paid increased annually—from approximately $290k in FY2022 up to $436k in FY2025—mirroring underlying earnings growth supportive of payout sustainability while retaining ample liquidity for operational needs.

Capital expenditures remain notably low (historically trivial amounts below $3k annually), consistent with an asset-light franchising framework focusing capital emphasis on marketing support and franchise development assistance rather than capital-intensive store build-outs [F1],[S4].

This prudent deployment underscores readiness for opportunistic investments if appropriate but currently signals restraint aligned with steady-state operations versus aggressive footprint expansion strategies demanded within fast-growth concepts.

What to Watch: Key Milestones and Franchise Development Signals

While explicit forward guidance is absent from filings reflecting regulatory caution around forward-looking statements [S2], key metrics bear close monitoring:

- Franchise unit count trends form a proximate gauge for royalty base expansion potential noting recent contraction from 64 units down to about 60 settled franchises indicating slowing pace or elevated churn rates possibly warranting strategic recalibration.

- Royalty revenue stability versus initial fee fluctuations reflects underlying new store opening dynamics crucial for top-line trajectory assessment.

- Marketing fund expenditures which directly support brand awareness campaigns correlate positively with subsequent new franchise inquiries thus any spend uptick could signal imminent system-wide growth acceleration [S7].[N/A]

- Regulatory shifts especially any changes impacting disclosure requirements or labor laws carrying material compliance cost implications must be surveilled closely given their outsized influence on franchisor-franchisee relations {analysis}

- Nontraditional revenue channels such as licensed product partnerships beyond core mix expansions might offer incremental upside if effectively scaled preserving brand cohesion while diversifying income pools.

In summary, BAB’s multi-brand synergy strategy forms a resilient backbone amid industry fragmentation yet requires vigilant execution across key operational variables including ongoing franchise recruitment/retention effectiveness supported by timely marketing initiatives paired with rigorous regulatory compliance management constraining downside risks.

This analysis synthesizes publicly available filings without offering investment advice or price forecasts. Readers should consider supplemental sources for comprehensive valuation assessments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments