Brookfield Renewable’s Strategies Amid Fiscal Hurdles and Expansion Plans

BEPC leverages its diversified renewable portfolio and capital deployment to counteract recent financial headwinds while aiming for sustainable growth.

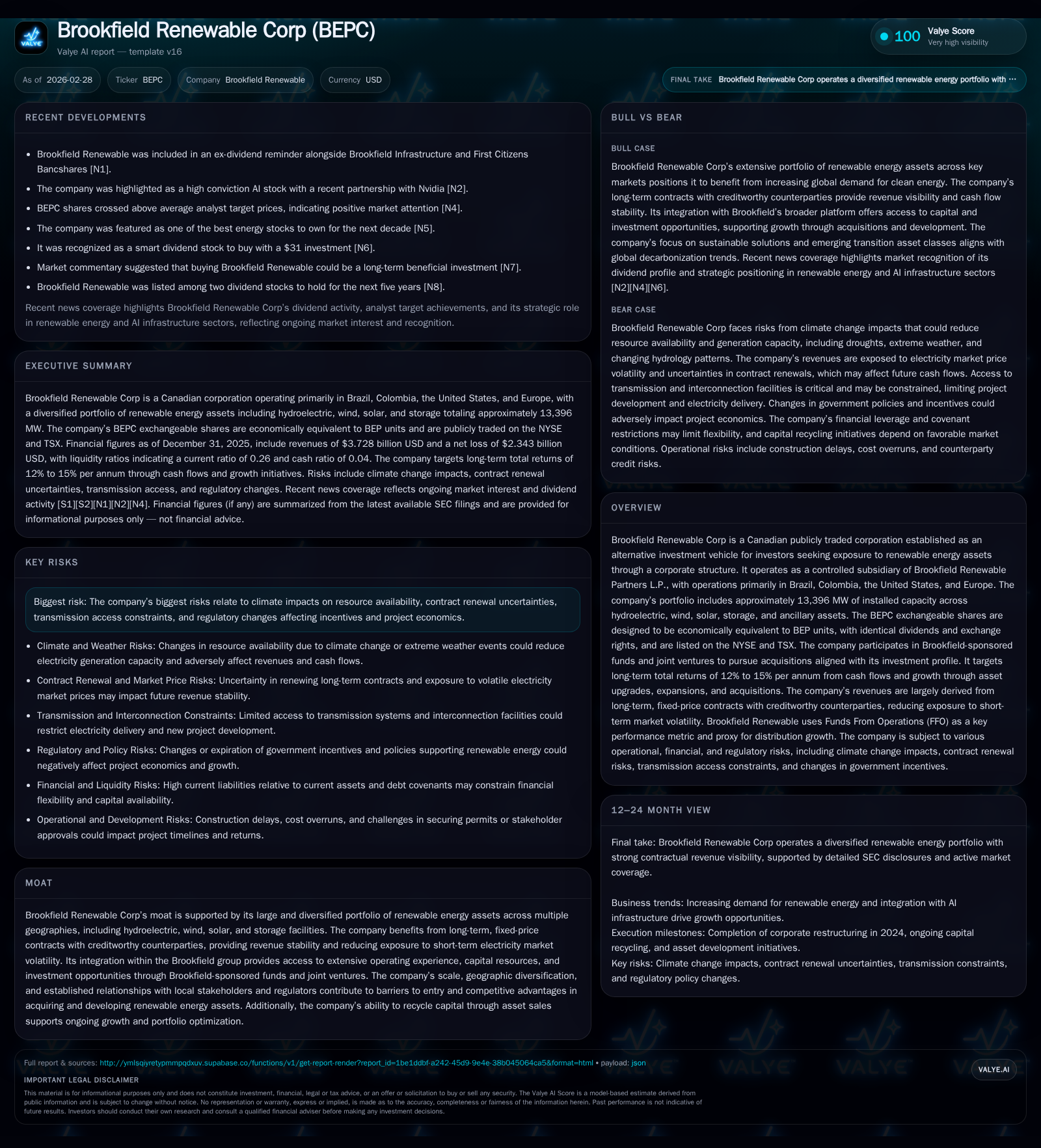

Brookfield Renewable Corp (BEPC) operates a substantial renewable energy asset base across key global regions, yet faced a notable revenue decline and net loss in 2025 driven by resource variability and asset sales. Despite the fiscal setbacks marked by a -10% revenue contraction and a sharply negative net income swing, BEPC’s strategic capital allocation—including disciplined dividend policies supported by funds from operations (FFO), ongoing asset recycling, and access to Brookfield-sponsored joint ventures—aims to stabilize cash flows and foster long-term growth. The company’s expansive hydroelectric, wind, solar, and storage footprint aligned with long-term fixed-price contracts provides a structural moat, but exposure to climate variability and regulatory shifts remains a critical risk to monitor.

Historical Performance and Revenue Dynamics

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 3.7 | -2.3 | -10.0% | -641.1% |

| 2024 | 4.1 | 0.4 | +4.4% | +40.6% |

| 2023 | 4.0 | 0.3 | +5.0% | -83.4% |

| 2022 | 3.8 | 1.9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -25.4 |

| 2024 | 3.6 |

| 2023 | 1.8 |

| 2022 | 11.0 |

Source: SEC companyfacts cache [F1].

Brookfield Renewable Corp (BEPC) reported revenues of approximately $3.73 billion in fiscal year 2025, marking a 10% decline compared to $4.14 billion in 2024 [F1]. This contraction reflects unfavorable hydrology conditions at U.S. and Brazilian hydroelectric facilities alongside recently completed asset sales that collectively reduced generation volumes by over 4 million MWh equivalent [S18]. Notably, on a constant currency basis excluding dispositions and acquisitions, revenue still fell by about $156 million primarily due to lower spot prices on uncontracted Colombian generation stemming from system-wide higher hydrology at the market level.

Net income suffered a dramatic deterioration from a positive $433 million in 2024 to a loss of $2.34 billion in 2025 [F1][S9]. This swing is attributable largely to significant non-cash remeasurements of shares classified as financial liabilities related to fluctuations in BEP unit prices and financial instruments post-Arrangement restructuring—the company recorded an $848 million loss on exchangeable shares remeasurement as well as an $813 million charge on interests held in Brookfield Renewable Holdings Corporation (BRHC) Class C shares [S9]. These accounting adjustments mask underlying operational cash flow resilience.

Operating Cost Structure and Asset Developments

Direct operating expenses totaled $1.50 billion in 2025 versus $1.77 billion in 2024 reflecting portfolio streamlining through asset sales but also increased expenditures stemming from additional power purchases in Colombia. Such power purchases are passed through directly to customers under contractual arrangements mitigating margin impact but increasing gross cost lines [S4][S9]. Management service costs rose modestly by roughly $4 million year-over-year to $110 million.

Depreciation declined slightly from $1.26 billion to $1.24 billion driven by derecognition of sold assets during the year consistent with BEPC’s active asset recycling approach designed to optimize capital deployment efficiency across its mix of hydroelectric, wind, solar and energy storage projects spanning four principal geographies: Brazil, Colombia, North America (primarily the U.S.), and Europe [S4][S14]. This multi-technology composition buffers capacity factor variability inherent to individual renewable resources allowing smoother operational leverage.

Capital Allocation Approaches: Dividends, Buybacks, and Debt Management

BEPC’s dividend policy is anchored on funds from operations (FFO), which serve as a forward-looking proxy for distribution sustainability aligned with operating cash flow rather than GAAP earnings that are influenced heavily by non-cash charges [S7][S16]. While there has been no material buyback program disclosed recently, the company actively recycles capital via portfolio sales such as recent interests sold in hydroelectric assets generating proceeds used for accretive growth investments or debt reduction.

Liquidity-wise, BEPC holds an undrawn revolving credit facility of $150 million with a ten-year term subject to annual extensions providing short-term funding agility [S3]. As of December 31, 2025, cash & equivalents stood at approximately $682 million but this is contrasted by considerable current liabilities around $15.45 billion resulting in a conservative current ratio near 0.26 highlighting the tightly managed working capital cycle within its complex structured financials [F1][S3]. The company reported an approximate negative return on equity (ROE) of -25.4% driven largely by the net loss against equity base at year-end ($2.34B loss vs ~$9.23B equity), underscoring that accounting impacts weigh heavily despite ongoing cash-generative business units [F1].

Long-Term Growth Drivers Anchored in Geographic and Technological Diversification

Looking ahead, BEPC’s long-term growth engine reflects both its geographic diversity—spanning mature U.S., South American emerging markets like Brazil/Colombia where inflation indexed tariffs prevail—and European operations benefiting from stable policy regimes—and its diversified technology stack comprising around 13.4 GW installed capacity inclusive of hydroelectric (~majority share), complemented by wind farms, solar arrays plus emerging battery storage assets enhancing grid flexibility [N4][S14][F1].

This geographic spread mitigates localized climate risk exposure while harnessing varying hydrological baselines and wind/irradiance profiles which underpin production stability over multiple weather cycles—a key buffer against capacity factor volatility commonly plaguing stand-alone projects. Furthermore, participation alongside Brookfield-sponsored funds bolsters acquisition pipelines facilitating disciplined expansion targeting annual total returns between 12%–15%, blending organic upgrades such as repowering older turbines plus bolt-on deals expanding footprint or entering adjacent transition solution businesses at scale [N4][S16].

Risks from Climate Variability and Regulatory Landscapes

The principal operational risks identified revolve around hydrological fluctuations impacting water availability for hydro plants; variability in wind speeds affecting turbine output; solar irradiance irregularities potentially curtailing photovoltaic yields; as well as extreme weather events such as droughts or floods imposing physical or logistical disruptions [S23]. These climate-related risk vectors translate into potential deviations in expected electricity output consequently affecting revenue streams.

Regulatory uncertainties compound these exposures given that many assets operate under long-duration contracts tied partly or wholly to governmental incentive frameworks that may evolve with shifting policy regimes globally. Transmission constraints particularly evident in congested grids can also restrict delivery capacity thereby capping utilization rates despite available generation capability [S28]. Managing these requires proactive engagement with authorities alongside technical investments improving grid interconnectivity.

Financial Liquidity, Capital Structure, and Leverage Considerations

Despite robust total assets exceeding $46 billion due principally to property plant & equipment valued at nearly $40 billion post revaluation gains recognizing improved power prices across South America & Europe along with currency effects (e.g., Euro strengthening vs USD), BEPC's balance sheet reveals high leverage levels with over $15 billion recorded as non-recourse borrowings at December 31, 2025 [F1][S11]. Non-recourse financing typical for infrastructure enables project-level debt separation reducing consolidated risk but complicates debt servicing profiles.

Additional complexities arise from intercompany financing arrangements including related party loans bearing market-based interest rates (~7.5%) reflecting tax optimization strategies within the group currently contributing roughly $45 million annual interest expense burden [S20]. Financial covenants embedded within loan agreements restrict discretionary activities ranging from incurrence of further indebtedness to asset disposal caps posing potential operational constraints under stressed scenarios [S21]. Nonetheless access to diversified funding channels including private Brookfield funds enhances capital raising agility critical for future growth deployment.

What to Watch: Outlook on Operational Milestones and Market Conditions

Investors should monitor forthcoming contract renewal outcomes especially those underpinning large hydroelectric portfolios where renegotiation terms may influence future price floors or escalation formulas. The timing and scale of new project commissioning episodes across solar-storage initiatives will likewise inform incremental capacity additions whilst asset sale transactions remain busy avenues for capital recycling fueling accretive reinvestment strategies enhancing cash returns over time.

Operational FFO trends remain key barometers serving as practical surrogates for dividend coverage given their closer linkage to underlying cash flows versus volatile net income reporting subject to accounting remeasurements. Market sentiment appears constructive recently as BEPC crossed above average analyst price targets indicating positive outlook perceptions though geopolitical/policy unpredictabilities require continued vigilance [N8][N11].

This analysis is based solely on information available through February 28, 2026 and does not constitute investment advice. It aims to present an objective view of Brookfield Renewable Corp’s strategic positioning relative to its recent performance data drawn from SEC filings combined with sector-specific considerations relevant to renewable infrastructure operators.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments