Dutch Bros Inc.: Navigating Rapid Growth Amidst Fierce Competition and Macroeconomic Headwinds

An in-depth analysis of Dutch Bros’ distinctive drive-thru model, digital innovation, and strategic scale as it confronts evolving market challenges.

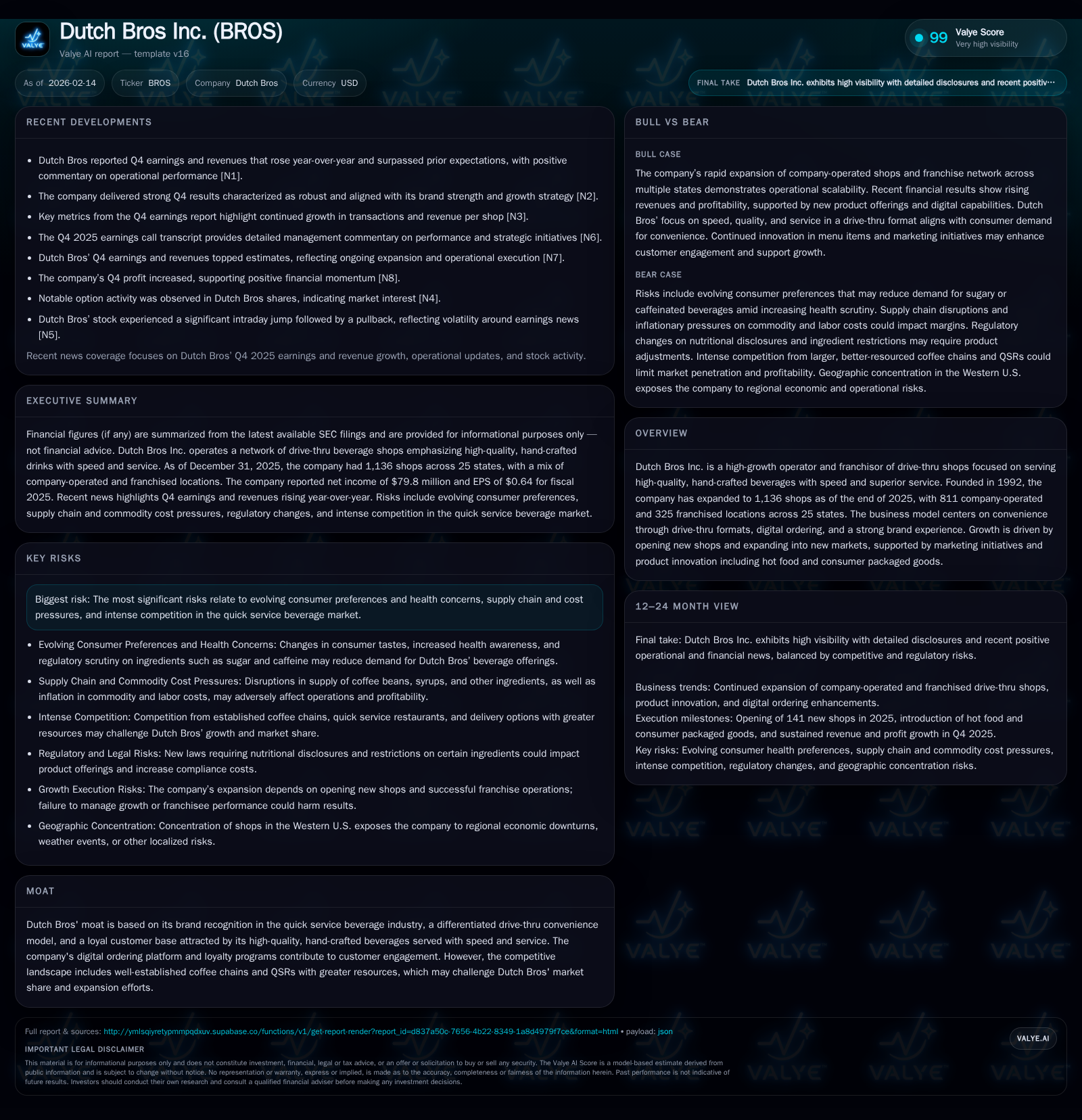

Dutch Bros Inc. has surged from a humble pushcart to operating 1,136 shops nationwide by the end of 2025, leveraging a drive-thru convenience model combined with high-quality handcrafted beverages. Recent Q4 earnings impressed with strong top-line growth and operational metrics, although stock volatility underscores underlying marketplace uncertainties. Balancing franchised outlets with company-operated stores provides both scalability and control challenges, while supply chain risks tied to tariffs and inflation loom large. Digital ordering and loyalty programs stand out as key competitive differentiators that foster customer engagement in an intensely competitive quick service beverage environment.

Fueling Growth: From Pushcart to 1,136 Shops

Dutch Bros Inc. exemplifies a high-velocity growth trajectory uncommon in the quick service beverage domain. Founded in 1992 by Dane and Travis Boersma with a simple espresso pushcart in Grants Pass, Oregon, the company propelled itself into one of the fastest-growing coffee brands nationally. By December 31, 2025, Dutch Bros operated 1,136 shops spanning 25 states—comprised of 811 company-operated outlets complemented by 325 franchised locations [S1][F1]. This dual footprint enables aggressive scale while retaining direct operational oversight on a majority of units.

This rapid expansion reflects a focused strategy that prioritizes drive-thru convenience paired with hand-crafted beverage quality—a combination intended to capture consumers seeking speed without sacrificing artisanal flavor profiles. The geographic spread beyond its Pacific Northwest roots signals not only ambition but an adaptability to varied regional markets.

In essence, Dutch Bros' story is one of transforming grassroots beginnings into a national platform characterized by substantial unit base growth and evolving product mix innovation.

Differentiation in a Crowded Quick Service Beverage Market

The quick service beverage ecosystem is notoriously saturated; formidable incumbents like Starbucks dominate footprint and consumer mindshare. Dutch Bros carves a distinct niche through its emphasis on drive-thru accessibility marrying speed with high-touch service culture—the “speed and superior service” ethos is central [S1]. Unlike traditional sit-down coffeehouses or heavy dine-in models, Dutch Bros' drive-thru-centric format taps into modern consumers' craving for efficiency without compromising drink customization or quality.

Beyond physical format advantages, their branding leans heavily on community engagement and employee enthusiasm which fosters customer loyalty. This is bolstered by premium handcrafted products that set the company apart from commoditized quick serves. These pillars collectively forge a defensible moat against competitors—especially those slower to innovate digitally or less flexible operationally [valye_report_excerpt].

Consequently, Dutch Bros' differentiation is multidimensional, simultaneously addressing convenience fatigue prevalent among consumers while creating an experiential connection rarely matched in the segment.

Q4 2025 Earnings Beat: Parsing the Metrics Behind the Surge

Dutch Bros’ Q4 earnings released February 13 showed both earnings per share and revenues surpassing consensus estimates year-over-year growth [N1][N2][N3]. Key metrics highlighted customer transaction growth alongside same-store sales increases—a signal of sustained demand rather than reliance solely on unit expansion. Such performance underpinned a sharp stock price opening jump of +17.7%, although this was tempered later in trading as profit-taking set in amid broader market volatility [N10].

Option market activity suggested heightened trader interest post-earnings but reflected polarized sentiment given prevailing macroeconomic uncertainty [N9]. Analysts extrapolated from underlying fundamentals noting Dutch Bros’ ability to maintain premium price points without eroding volume as encouraging amidst inflationary pressures [N8]. Yet vigilance remains warranted regarding execution risks tied to rapid growth cadence.

Dutch Bros thus stands at an inflection point where financial strength meets investor caution—demand durability juxtaposed against external economic headwinds.

Franchising and Company-Operated Balance: Scaling Without Dilution?

The company’s portfolio split—approximately 72% company-operated (811 shops) versus 28% franchised (325 shops)—reveals a hybrid model aiming for controlled expansion without compromising brand integrity [S1][valye_report_excerpt]. Operating the majority of locations directly allows tighter control over customer experience standards, training protocols, and operational consistency critical to maintaining Dutch Bros’ differentiated value proposition.

However, franchise growth supports capital-light expansion enabling access to new markets more rapidly than company operation alone would allow. This introduces complexity related to alignment of franchisees’ incentives with corporate objectives—disparate partner priorities can threaten uniformity in execution or lead to operational variability across regions [S1].

Effective governance mechanisms will be paramount as Dutch Bros balances empowerment with oversight amidst escalating scale—ensuring franchisees uphold brand ethos while achieving profitability goals.

Supply Chain and Tariff Turbulence: Brewing Under Pressure

Recent geopolitical developments pose tangible risks for Dutch Bros’ input costs and supply chain reliability [S2]. Heightened tariffs targeting imported green coffee beans have escalated sourcing expenses which traditionally represent a significant cost component. Inflation across raw materials including dairy further compresses margins.

Such pressures necessitate calibrated pricing strategies that avoid alienating price-sensitive customers while preserving profitability. Additionally, supply chain disruptions stemming from trade restrictions could impair timely shop replenishments risking inventory shortages or inconsistent product availability [S2].

Beyond financial implications, persistent supply uncertainty could erode customer trust if popular products are intermittently unavailable. These factors underscore why supply chain resilience constitutes a critical pillar underpinning Dutch Bros’ long-term operational stability.

Digital Ordering & Loyalty: Amplifying Brand Stickiness

A less overt yet powerful engine driving Dutch Bros’ competitive advantage lies in its digital innovation—the integration of ordering apps coupled with sophisticated loyalty programs cultivates heightened customer engagement [valye_report_excerpt][N13].

These platforms empower consumers with seamless pre-order capability enhancing convenience beyond physical store visits alone. Concurrently, data gleaned from app interactions informs targeted marketing initiatives fostering repeat purchases via personalized offers and rewards.

Such digital ecosystems translate into increased frequency per user—critical for maximizing lifetime value—and build barriers to exit as switching costs rise for loyal customers habituated to the Dutch Bros experience. In a sector where product commoditization is commonplace, these tools inject differentiation at the connection point between brand and consumer.

Competitive Landscape: How Dutch Bros Stacks Up

Operating within an arena crowded by heavyweights such as Starbucks—as well as quick service restaurant chains like McDonald’s intensifying their beverage focus—Dutch Bros leverages speed-oriented drive-thru formats paired with community-driven culture to run laps around broader incumbents’ traditionally sit-down focus [N6][N13][valye_report_excerpt].

Unlike large chains often encumbered by legacy footprints less optimized for swift service or digital ordering flexibility, Dutch Bros’ agility affords nimbleness facilitating tailored local marketing campaigns combined with rapid product innovation including hot food offerings.

However, competition extends beyond brick-and-mortar as delivery services increasingly capture off-premise demand challenging convenience paradigms historically owned by drive-thrus. While many rivals possess deeper pockets for huge marketing spends or technology investments, Dutch Bros’ authentic brand narrative anchored in speed must continue evolving to maintain relevance amid shifting consumer habits.

Overall competitive positioning reflects nuanced strengths balanced against formidable rivals’ resource heft.

Risks on the Horizon: Consumer Shifts, Competition, and Operational Challenges

Dutch Bros candidly acknowledges numerous risk vectors threatening sustained momentum [S1][S2]. Foremost among these are evolving consumer preferences increasingly emphasizing health-conscious options possibly detracting from indulgent beverage purchases. Moreover, intense competition narrows price elasticity forcing careful margin management.

Labor shortages challenge staffing stability crucial for consistent service excellence integral to brand identity. Geographic concentration primarily within Western U.S. elevates vulnerability to regional economic downturns or regulatory shifts impacting operations.

Brand reputation maintenance amplifies risk—any food safety incident or perceived quality lapse could disproportionately damage loyalty cultivated over decades. Furthermore, scaling culture alongside rapid unit additions demands robust leadership development lest employee engagement diminish impacting customer experiences negatively.

Dutch Bros must navigate these intertwined risks proactively sustaining its hard-earned brand equity amid unrelenting industry pressure points.

Valuation in Context: Balancing Rapid Growth Against Emerging Headwinds

The trading patterns following Q4 earnings highlighted both enthusiasm for Dutch Bros' growth narrative alongside wariness regarding execution complexity under challenging macroeconomic conditions [N14][N9][N10][F1]. Comparisons with peers like Campagnolo Holdings (CMPGY) reveal debates around relative value propositions factoring differences in growth rate sustainability versus margin resilience.

While fundamental financials showcase healthy net income generation ($79.8 million in net income at year-end 2025) coupled with solid liquidity ($269 million cash balances) supporting continued investment [F1], volatility induced by tariff risks and competitive dynamics tempers bullish outlooks.

Investors appear weighing evidence of strong operational execution against uncertainties inherent in scaling infrastructure amid rising input costs and consumer landscape shifts—a delicate balance requiring vigilant monitoring moving forward.

This analysis synthesizes publicly available information including company filings and recent news disclosures without providing specific investment advice or recommendations. It aims solely to provide an informed perspective on Dutch Bros Inc.’s current positioning within its industry context and related macroeconomic considerations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments