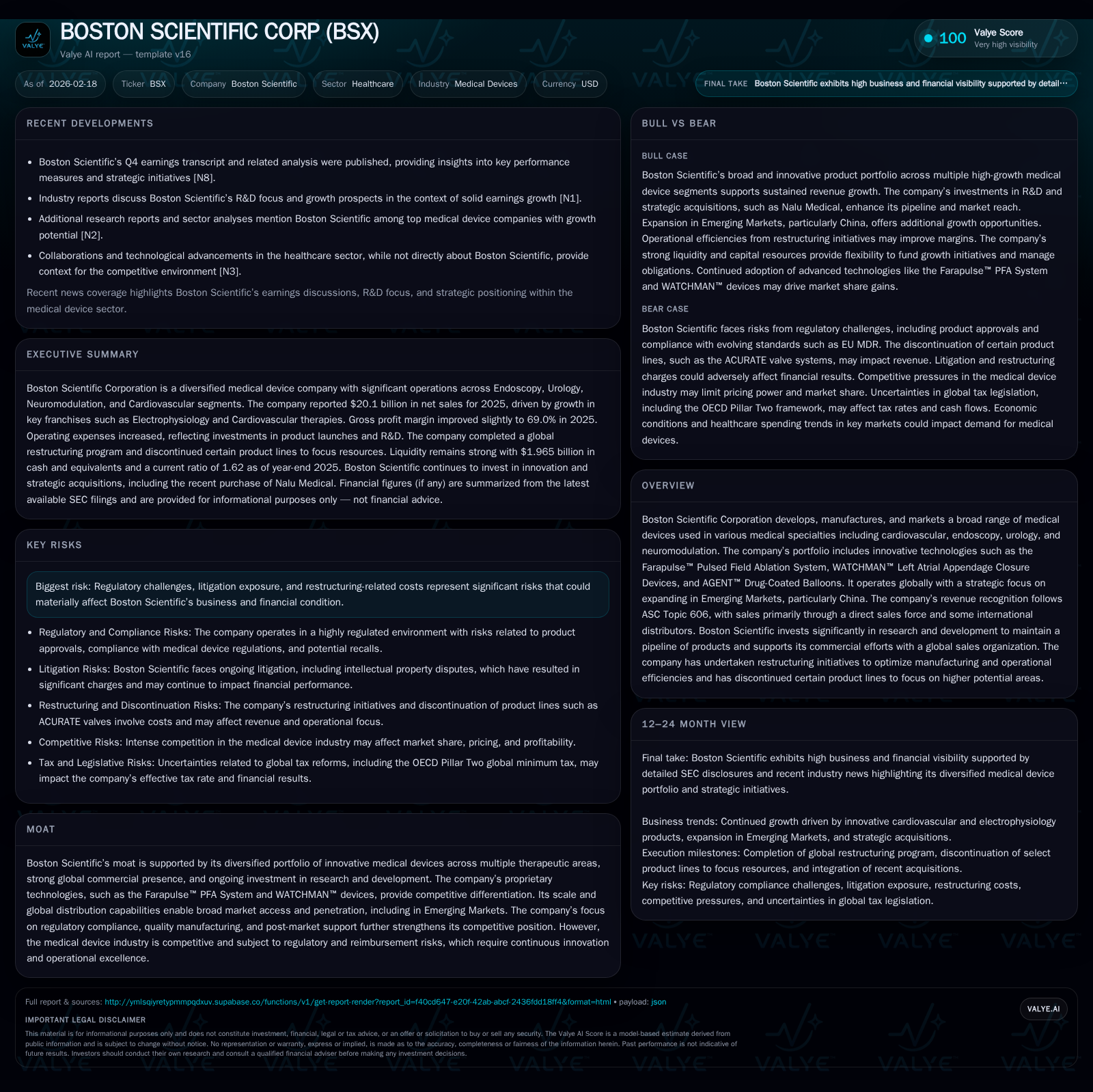

Boston Scientific’s Growth Fueled by Cardiovascular Expansion and R&D Amid Rising Legal and Restructuring Costs

Boston Scientific delivered double-digit revenue growth driven by cardiovascular and urology segments, supported by acquisitions and innovation while navigating legal exposures and operational restructuring.

In 2025, Boston Scientific Corp (BSX) reported robust revenue growth of nearly 20%, led by strong performance in cardiovascular and urology businesses, aided by the Axonics acquisition. Operating income rose almost 39% year-over-year reflecting operational leverage despite increased selling, general & administrative and research & development expenses. The company remains committed to innovation through substantial R&D investing in proprietary platforms such as Farapulse™ and WATCHMAN™, which underpin its competitive moat. Legal risks from ongoing patent suits and product liability claims persist, alongside restructuring cost absorption. Liquidity is solid with prudent debt management post-acquisitions. Future growth depends on continued regulatory approvals, adoption of new devices, and success integrating acquisitions.

Company Overview

Boston Scientific Corporation (BSX) operates as a global medical device manufacturer specializing across cardiovascular, endoscopy, urology, neuromodulation, and other surgical specialties. Its portfolio features proprietary technologies such as the Farapulse™ Pulsed Field Ablation System for electrophysiology procedures, WATCHMAN™ Left Atrial Appendage Closure Devices for stroke risk mitigation, and AGENT™ drug-coated balloons enhancing vascular interventions [S1]. The firm pursues growth through R&D investment complemented by strategic acquisitions aimed at expanding its technological breadth and geographic reach.

Historical Performance Trends

Between fiscal years 2023 to 2025, Boston Scientific posted accelerating top-line growth with full-year revenues advancing from approximately $14.24 billion in 2023 to $16.75 billion in 2024 (+17.6%), then reaching $20.07 billion in 2025 (+19.9%) [F1]. This expansion was underpinned notably by segment gains:

Historical performance (annual)

| FY | CFO ($bn) | OpInc ($bn) | Capex ($mm) |

|---|---|---|---|

| 2025 | 4.5 | 3.6 | 876 |

| 2024 | 3.4 | 2.6 | 790 |

| 2023 | 2.5 | 2.3 | 711 |

| 2022 | 1.5 | 1.6 | 588 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Net, Buybacks, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($bn) |

|---|---|---|

| 2025 | 3.7 | |

| 2024 | 0 | 2.6 |

| 2023 | 28 | 1.8 |

| 2022 | 55 | 0.9 |

Source: SEC companyfacts cache [F1].

Note: Net income data not sufficient for recent years; dividends suspended post-2023 [F1]

Operating income increased disproportionately faster than revenue in 2025 reflecting improved operating leverage despite significant rises in SG&A (+15%) and R&D (+27%) costs [S14]. Cash flow from operations grew substantially (+32%), supporting capex spending that incrementally rose by nearly 11%. These investments underpin production capacity expansion aligned with recent product launches.

Segment-wise breakdown shows cardiovascular business growing over 23% annually driven primarily by the Silk Road Medical acquisition but buoyed by strong organic demand particularly in interventional oncology and electrophysiology franchises [S7][S8]. Urology’s surge stems materially from the Axonics acquisition finalized mid-2024 plus robust stone management device sales [S7]. Endoscopy and neuromodulation segments also contributed steady mid-single-digit organic gains supporting diversified revenue streams.

Future Growth Drivers

Key catalysts include:

- The integration and commercial scale-up of acquired platforms such as Axonics (urology neuromodulation) and Silk Road Medical (vascular interventions).

- Continued market penetration of proprietary technologies like Farapulse™ PFA system that offers differentiated ablation treatment with potential to displace legacy cryoablation devices.

- Expansion into emerging markets focusing on China where rising healthcare infrastructure investments create demand upside [N13][S7].

- Enhanced clinical evidence and regulatory approvals supporting WATCHMAN™ devices which have reshaped stroke prophylaxis approaches.

- Ongoing investments in product pipeline through elevated R&D spending targeting both incremental device improvements and new modality innovations [S14].

Constraints on growth may arise from regulatory hurdles given the high scrutiny medical devices endure globally especially post EU MDR implementation costs totaling an estimated $475-$525 million through transition periods [S14], alongside competition intensity that necessitates continuous technology evolution.

Financial Expectations & Milestones to Watch

No explicit company guidance is available in the provided documents for FY2026 forecasts yet milestones to monitor include:

- Revenue progress within newly integrated Axonics products and advancements in neuromodulation market share.

- Approval status updates on pipeline technologies pending FDA or international agency clearance.

- Progress against supply chain optimization targets linked to restructuring completed under the 2023 Restructuring Plan [S14].

- Operating margin trends amid continued SG&A investments for global sales expansion especially digital sales enablement efforts.

- Litigation outcomes notably residual patent infringement disputes involving Synergy Stent System affecting royalty streams [S5][S6][S12].

Analysts should watch quarterly earnings calls for management commentary on these items as well as potential capital deployment changes.

Returns & Capital Allocation

With net income details sparse recently [F1], exact ROE calculations are limited but rough estimates based on operating income vs equity suggest modest returns likely pressured by litigation costs and restructuring investments (~0.8% reported net income relative to equity). The company generated approximately $3.65 billion free cash flow (CFO minus capex) in FY25 sustaining a strong liquidity position including nearly $2 billion cash equivalents [F1][S21].

Capital allocation priorities focus on:

- Conservative balance sheet management evidenced by compliance with low leverage ratios well below covenant maxima despite Qualified Acquisitions-related allowances including the large Axonics deal valued over $1 billion [S13][S17].

- Suspension of buybacks since early 2020 due to capital preservation strategy amid acquisitions; however, a buyback authorization of up to $1 billion remains unused at year-end [S10].

- Dividends have been minimal or absent since FY23 reflecting reinvestment emphasis amid evolving market conditions.

- Healthy cash flow generation provides optionality for further bolt-on acquisitions or increased shareholder returns subject to legal resolution progress.

Industry & Competitive Context Analysis

Boston Scientific operates within a fiercely competitive medical device industry characterized by rapid technology cycles, intense patent litigation exposure, and complex global regulatory compliance frameworks including EU MDR implementation that add cost burdens but also enforce quality standards elevating barriers for entrants . Regulatory risks encompass approval delays or product recalls while reimbursement policies influence adoption rates especially in public healthcare systems.

Innovative capabilities such as pulsed field ablation technologies represent an inflection point potentially displacing established modalities if clinical benefits translate broadly into adoption—this competitive dynamic highlights the importance of Boston Scientific’s robust R&D ecosystem alongside targeted M&A strategies to maintain therapeutic area leadership.

Risks & Litigation Exposure

The company faces multiple legal risks detailed extensively:

- Intellectual property disputes including the University of Texas patent infringement suit over Synergy Stent products which resulted in damages awarded but remain under appeal [S12][S16].

- Product liability cases predominantly tied to transvaginal surgical mesh products raise potential material settlement exposures though many resolved via master agreements [S16][S29].

- Regulatory investigations such as alleged Foreign Corrupt Practices Act violations require ongoing attention with risks ranging from fines to operational restrictions [S5][S6].

- Accrued legal reserves stand at approximately $242 million with additional contingent liabilities uncertain but material potential impact cannot be excluded [S11].

Such liabilities can impede market access or increase operating costs unexpectedly challenging profitability metrics.

Liquidity & Debt Profile

Boston Scientific ended FY25 with total debt at about $11.44 billion dominated by fixed-rate senior notes issued over multiple maturities extending beyond 2030 ensuring manageable refinancing risk [S13][S17][F1]. Cash on hand near $2 billion combined with undrawn revolving bank credit facility of $2.75 billion ensures ample liquidity buffers against contingencies including settlements or restructuring-related costs [S21].

Maximum permitted leverage ratio stood at 4.50x post-marked Qualified Acquisition step down following Axonics deal; actual leverage measured was comfortably lower at approx 1.92x EBITDA reinforcing financial flexibility adherence to covenant terms [S17][S18].

Conclusion

Boston Scientific demonstrates solid historical growth propelled by strategic acquisitions, diversified therapeutic coverage, cutting-edge product innovation backed by high R&D spend, and robust global commercial execution notably in cardiovascular and urology segments. Legal risks remain a notable drag alongside continued execution of manufacturing streamlining initiatives initiated under its restructuring plan.

Monitoring future regulatory clearances for pipeline devices, integration effectiveness for recent deals like Axonics, emerging market expansion success particularly China, plus litigation developments will be crucial indicators shaping Boston Scientific’s trajectory beyond FY25.

This analysis is based solely on publicly available information including company SEC filings dated through February 2026, supplemented by authoritative sector insights where noted without speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments