Quantum Corp’s Financial Restructuring Raises Prospects Amid Storage Sector Shifts

Quantum Corporation’s convertible debt issuance and early revenue improvements highlight a fragile yet pivotal stage in its turnaround within data storage and media archiving.

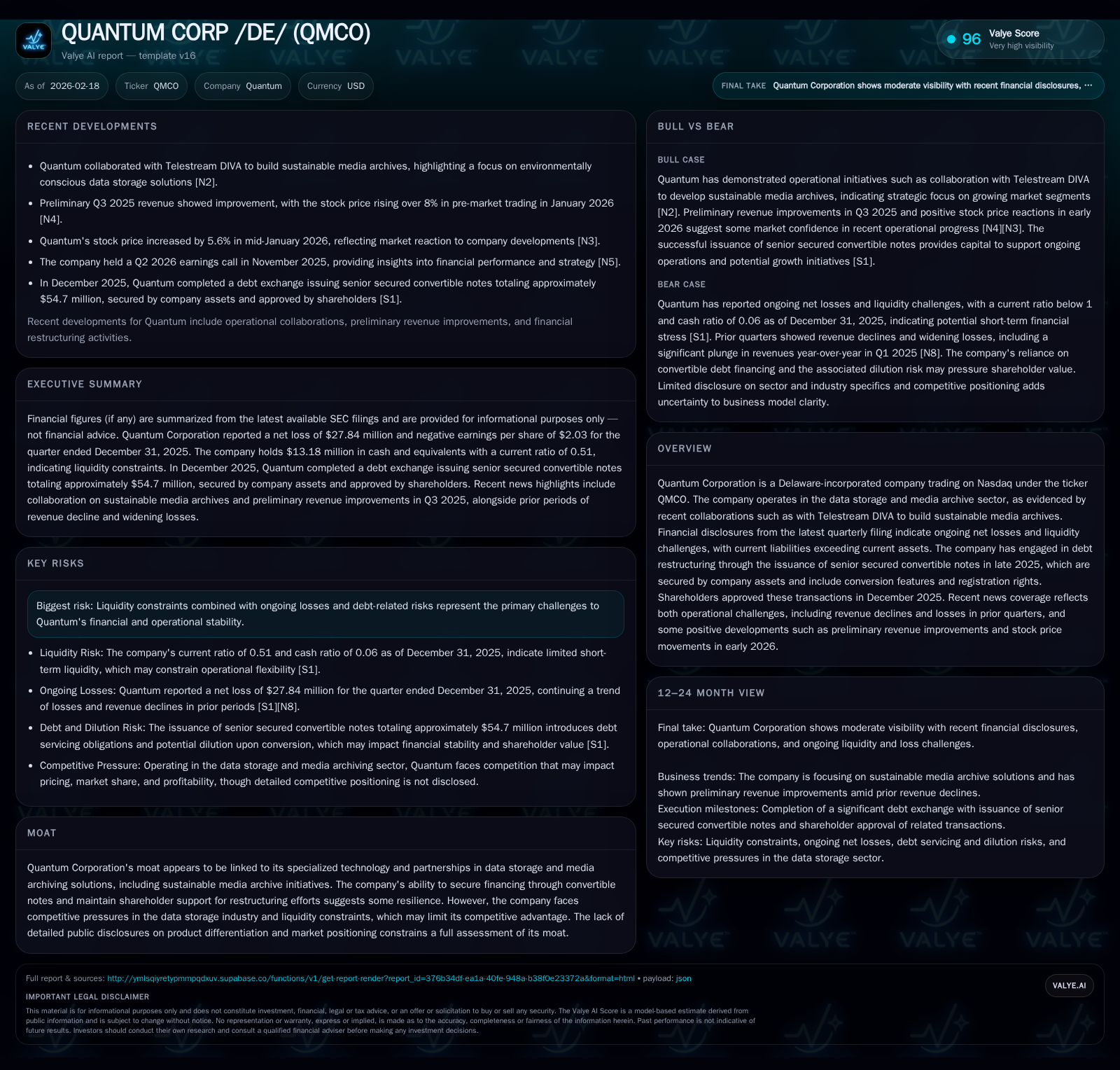

Quantum Corp has historically struggled with declining revenues, mounting losses, and liquidity challenges characteristic of the evolving data storage industry. The company’s strategic issuance of $54.7 million in senior secured convertible notes during late 2025, backed by shareholder approval, aims to alleviate near-term debt pressure while introducing conversion price mechanics and anti-dilution measures that could affect equity structure. Preliminary signals of revenue rebound, supported by innovative collaborations like its sustainable media archive partnership with Telestream DIVA, offer growth avenues. However, ongoing operational losses, negative cash flow trends, and a current ratio of approximately 0.51 underscore persistent solvency risks. Monitoring upcoming conversion price resets and quarterly milestones will be crucial for assessing Quantum's trajectory amid sector competitive pressures.

Revenue Trajectory and Historical Financial Challenges

Quantum Corporation’s revenue has demonstrated significant growth over the past several years, expanding from approximately $103 million in fiscal year 2019 to nearly $373 million by fiscal year 2022 [F1]. This represents an aggregate increase of about 261%, reflecting periods of rapid expansion coinciding with broader data storage demand surges. Nonetheless, this top-line progression masks fluctuating performance dynamics influenced by sector shifts such as increasing commoditization and evolving customer requirements.

Despite the revenue gains up through FY2022 (+6.7% YoY from FY2021 to FY2022), the company’s operating income trajectory reveals escalating challenges. Operating results turned persistently negative post-FY2019, with operating income losses deepening sharply to -$13.8 million in FY2022 and further deteriorating to -$41.7 million by FY2025 [F1].

Net income performance mirrors this pattern: after incurring $32.3 million losses in FY2022, Quantum’s net losses swelled dramatically to over $115 million by FY2025 [F1], indicating intensifying operational cost burdens and margin pressures despite growing revenues. This contrast between top-line growth and bottom-line erosion sets a challenging context for operational sustainability.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -115 | -24 | -42 | 5 | -507.6% |

| 2024 | -19 | -10 | -14 | 6 | +50.1% |

| 2023 | -38 | -5 | -26 | 13 | -17.5% |

| 2022 | -32 | -34 | -14 | 6 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -29 | 70.0 |

| 2024 | -16 | 15.6 |

| 2023 | -17 | 43.7 |

| 2022 | -40 | 25.5 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures beyond FY2022 are unavailable; operating income and net are full fiscal years ending March except the latest quarterly data ending Dec-31-25 [F1].

Operational Losses and Cash Flow Dynamics

The company’s financial health remains substantially impaired by continual operating losses eroding capital reserves [F1]. Operating cash flows have consistently been negative with an alarming deepening trend: CFO declined from a deficit of approximately $33.7 million in FY2022 to roughly -$23.6 million in FY2025 [F1]. When juxtaposed against capital expenditures fluctuating around $4.9-$12.6 million annually but showing a modest contraction (-15.7% from FY2024 to FY2025), the resulting free cash flow remains solidly negative (approximate FCF: -$28.6 million in FY2025) [F1].

This persistent cash burn exacerbates Quantum’s liquidity challenges amid its shrinking equity base (equity turning further negative to around -$164 million by FY2025) [F1], necessitating external financing maneuvers explored later herein.

The severity of loss-making operations limits reinvestment capacity unless substantial top-line growth or cost rationalization occurs.

Innovative Partnerships Fueling Growth Potential

Quantum’s collaboration with Telestream DIVA announced in early 2026 centers on creating sustainable media archives leveraging Quantum ActiveScale technology [N3]. This partnership integrates advanced storage solutions tailored for environmentally conscious media preservation workflows — a niche potentially differentiating Quantum against commoditized storage offerings.

By focusing on sustainable, scalable digital archiving platforms aligned with growing eco-friendly mandates in media industries, Quantum positions itself within a promising segment that could diversify revenue streams beyond traditional storage hardware sales [N3]. Such strategic alliances enhance technological moat formation by embedding Quantum’s products into media ecosystem workflows less vulnerable to pure price competition.

Convertible Notes Restructuring: Terms, Impact, and Shareholder Approval

In December 2025, Quantum executed a critical refinancing via issuance of approximately $54.7 million senior secured convertible notes exchanged dollar-for-dollar for existing term loan indebtedness owed primarily to Dialectic Technology SPV LLC [S4][S9][S10]. These notes bear an annual payment-in-kind (PIK) interest rate of 10%, compounding annually until maturity on December 18, 2028 [S4][S10].

Key terms include:

- Initial conversion price set at $10 per share common stock with anti-dilution protections favoring noteholders.

- Reset price mechanism scheduled at three sequential quarterly dates post-closing resets the conversion price downward if market prices warrant but floors at $4 per share [S10].

- Conversion upon maturity at an exchange price capped at 80% of market value calculated over recent trading days if not repaid.

- Potential forced conversions starting six months post-closing under defined conditions.

The note issuance was contingent on shareholder approvals acquired during the December 16, 2025 annual meeting with overwhelming consent across all proposals relating to debt exchange transactions [S6][S13]. Post-conversion dilution risk is material; immediate full conversion plus warrant exercises could represent roughly 36.9% ownership dilution to existing shareholders [S10].

This restructuring reflects a balancing act: relieving immediate debt servicing burden while exposing shareholders to dilution contingent on stock price development.

Liquidity Constraints and Balance Sheet Stress Tests

As of the end-December quarter of fiscal year 2025, Quantum reported current assets standing at $103.6 million versus current liabilities totaling approximately $203.2 million — equating to a stressed current ratio near just 0.51 [F1]. This pronounced shortfall underscores acute liquidity risk.

Management disclosures confirm stringent liquidity covenants embedded within both convertible notes indenture and amended term loan agreements mandating minimum quarterly liquidity thresholds ramping progressively from $3.75 million Q1-26 up to $7.5 million by Q4-26 [S4][S10][S24]. Failure to maintain these levels could trigger technical defaults or accelerated repayments.

Regulatory filings also spotlight ongoing operational uncertainty around liquidity sufficiency amid persistent net losses without clear path yet to positive cash generation [S2][S24]. This environment requires vigilant treasury management alongside timely revenue momentum capture.

Capital Allocation Landscape: Dividends, Buybacks, and Investment Patterns

Reflecting this tenuous financial position, Quantum has suspended dividend payments entirely — no data indicates dividend distributions historically or recently as per available XBRL tags [F1]. Similarly, there is no sign of share repurchase activity consistent with conserve-and-rebuild strategic posture advocated in recent SEC communications [S14][S19][S21].

Capital expenditures showed moderation from peaks near $12.6 million (FY2023) down towards roughly $4.9 million by FY2025 (-15.7% YoY), signaling restrained reinvestment possibly prioritizing maintenance CAPEX over growth initiatives [F1].

These capital allocation decisions align with efforts focused on stabilizing balance sheet health over returning capital to shareholders or aggressive expansion.

Key Milestones to Watch: Upcoming Quarters and Conversion Price Triggers

Investors should monitor impending reset price dates embedded within the convertible note indenture set across the first three calendar quarters following issuance — these may recalibrate conversion economics depending on market prices around each date [S10].

Additionally, forthcoming quarterly earnings reports will serve as critical checkpoints particularly after preliminary Q3 fiscal results indicated tentative revenue improvement leading to notable pre-market stock rises (+8%) in January 2026 [N2], which can signal traction towards financial stabilization.

Potential forced conversions or optional pre-maturity exchanges planned within the indenture add layers of complexity requiring close attention given their implications for equity dilution timing.[N2][S10]

Industry Context: Data Storage Competitive Pressures and Technological Moat

Within the data storage domain — particularly focusing on media archiving — commoditization continues driving margin compression broadly due to intensified competition from hyperscalers and cloud providers integrating low-cost object storage architectures.

Quantum attempts differentiation through specialized solutions integrating sustainability considerations and collaboration ecosystems exemplified by its Telestream DIVA alliance targeting carbon-conscious media archive deployment.[N3]

This niche focus could strengthen Quantum's technological moat by embedding deeper into workflow-dependent infrastructure rather than competing solely via hardware pricing or generic cloud storage access.

However, high fixed costs reflected in sustained operating losses combined with liquidity fragility impose constraints on agile response capabilities relative to larger peers.[F1]

Execution against emerging innovations will be essential for translating early revenue upticks into durable competitive advantage.

Disclaimer: This analysis is based solely on publicly available information as of February 18, 2026 including SEC filings and news reports cited herein; it does not constitute investment advice or recommendations but aims to provide objective insights into Quantum Corporation’s financial condition and sector positioning.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments