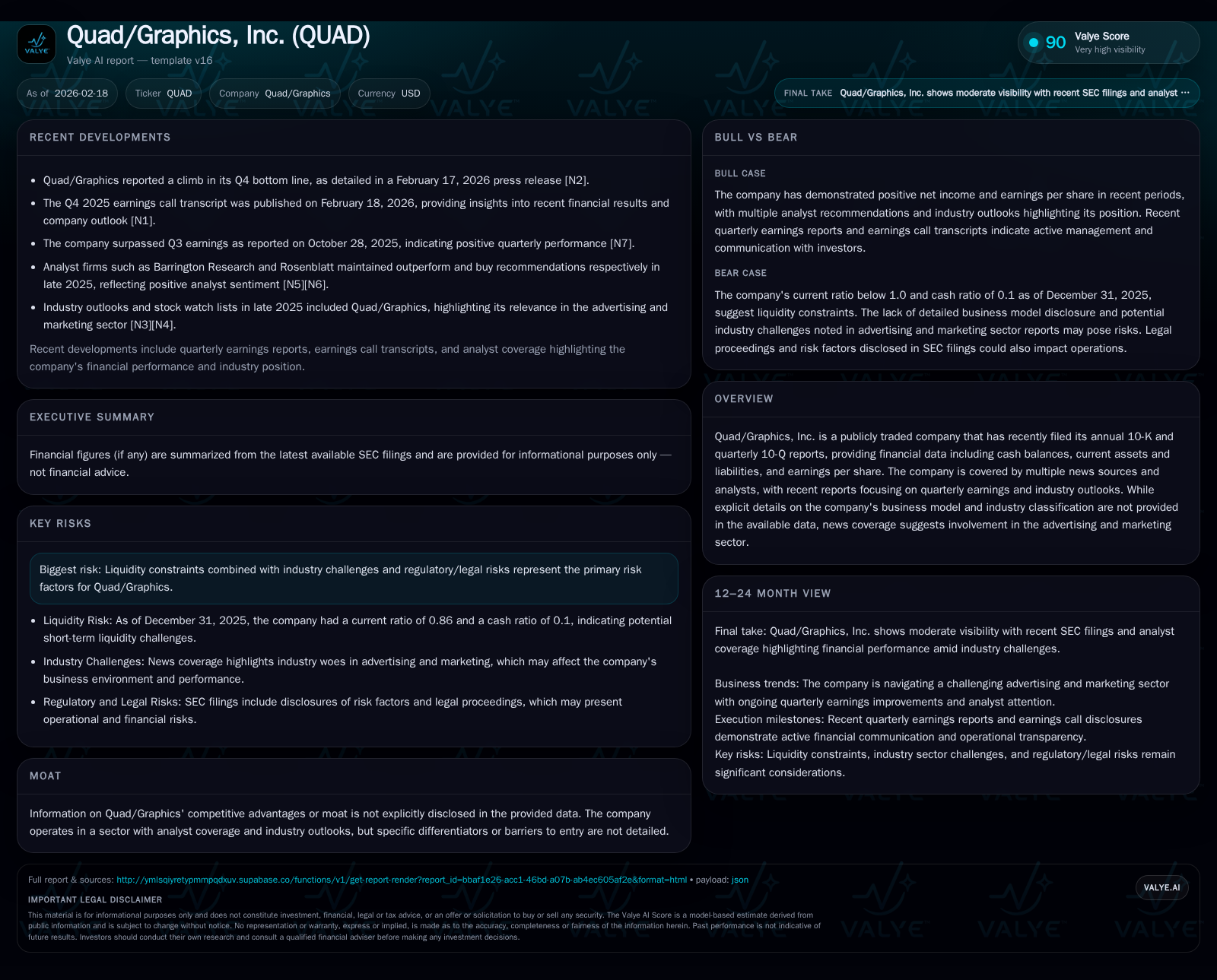

Quad/Graphics' Earnings Turnaround and Capital Strategy in a Tight Liquidity Environment

Quad/Graphics delivered a sharp rebound in operating income while facing significant balance sheet pressures, revealing a complex financial crossroads.

Quad/Graphics achieved an extraordinary 405.2% surge in operating income from FY2024 to FY2025, reversing several years of struggles, yet it continues to grapple with negative equity and liquidity constraints. The company’s capital allocation reflects a cautious but persistent dividend policy and selective share repurchases despite these financial headwinds. Leadership changes underscore efforts to drive operational discipline. However, regulatory risks and working capital demands remain notable challenges that cloud near-term prospects.

Financial Performance Reversal: Historical Growth Drivers and Operating Income Surge

Quad/Graphics exhibited a striking turnaround in operating income during the fiscal year ending December 31, 2025. After fluctuating between positive and modest levels—$53.5 million in FY2022 declining sharply to $19.2 million in FY2024—the company catapulted its operating income to $97.0 million in 2025 [F1]. This represents an exceptional year-over-year increase of approximately +405.2%, signaling substantial operational improvements.

Despite this robust operating income surge, net income shows more tempered gains with $10.2 million recorded for the first nine months of 2025 [F1], suggesting continued pressure from interest expenses or other non-operating factors.

Operating cash flow declined by about 15.1% from $112.9 million in FY2024 down to $95.9 million in FY2025 [F1], indicating working capital or cash cycle challenges despite profitability gains—typical for industries with complex receivables/payables dynamics.

Capital expenditures were reduced by approximately 21%, falling from $57.2 million in FY2024 to $45.2 million in FY2025 [F1], reflecting prudence amid liquidity constraints.

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) | Capex ($mm) |

|---|---|---|---|

| 2025 | 96 | 97 | 45 |

| 2024 | 113 | 19 | 57 |

| 2023 | 148 | 26 | 71 |

| 2022 | 155 | 54 | 60 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Net, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 14 | 8 | 51 |

| 2024 | 9 | 0 | 56 |

| 2023 | 0 | 13 | 77 |

| 2022 | 1 | 10 | 94 |

Source: SEC companyfacts cache [F1].

Note: Annual net income available only through trailing periods; dividend anomaly for FY2023 is noted.

Persistent Balance Sheet Pressures: Liquidity and Negative Equity Dynamics

At year-end December 31, 2025, Quad/Graphics reported current assets of approximately $538 million versus current liabilities of about $624 million, yielding a current ratio near 0.86—indicating short-term liquidity pressures where liabilities exceed liquid assets by roughly $86 million [F1]. This imbalance points to ongoing working capital management challenges.

More critically, shareholders’ equity was negative $59.5 million as of the same date [F1], marking a reversal from positive equity positions seen just a few years prior (e.g., $136.8 million at end-2021). Negative equity suggests accumulated losses or impairments imposing structural financial strain.

These factors heighten financial leverage risk and may restrict Quad/Graphics' flexibility for growth investments or navigating cyclical headwinds without external financing or restructuring initiatives [S9][S10][S18]. Risk disclosures across recent SEC filings emphasize potential liquidity squeezes alongside regulatory scrutiny that could affect future results [S4][S5][S7].

Capital Allocation: Balancing Shareholder Returns and Cash Preservation

The company's capital deployment reflects a cautious approach balancing shareholder distributions with liquidity preservation.

Dividends paid increased steadily—from negligible amounts in earlier years (e.g., ~$100K in FY2023) up to $14.4 million in FY2025—signaling management's intent to maintain shareholder returns despite constrained finances [F1].

Share repurchases recommenced modestly with $8 million spent in FY2025 following no buybacks in FY2024; prior years show intermittent repurchase activity (notably $12.6 million in FY2023), reflecting tactical capital return when conditions permit [F1].

Capex has been scaled back from mid-decade peaks (~$70+ million) to preserve free cash flow critical for servicing debt and managing working capital needs amid challenging conditions [F1].

This measured allocation strategy underscores priorities on sustaining free cash flow while selectively supporting shareholder value amidst financial constraints.

Leadership Changes and Governance Enhancements

Recent leadership restructuring includes appointing Dave Honan as President alongside his COO role, while Joel Quadracci remains Chairman and CEO—highlighting intensified operational focus [N1][S3][S20].

Board size was trimmed from ten to nine directors with shareholder approval on governance amendments including incentive plan updates designed to align executive compensation with long-term performance goals [S16][S17].

Such governance refinements aim to bolster strategic execution amid operational challenges common within the marketing services sector.

Regulatory and Legal Risks Impacting Earnings Visibility

Quad/Graphics continues to disclose significant legal proceedings and regulatory risks across multiple SEC filings [S4][S5][S6][S7], involving litigation exposures that may affect earnings predictability.

Management's risk narratives emphasize potential adverse outcomes from evolving industry regulations and contract complexities that could materially impact operations.

These factors contribute uncertainty around forward-looking results despite improving core operating metrics.

Outlook: Navigating Growth Amid Financial Constraints

Management commentary stresses balancing growth momentum with tight liquidity management as key priorities going forward [N1][N2][S2]. While margin expansion offers potential for improved profitability, persistent negative equity and working capital burdens remain constraining factors.

No explicit numeric guidance is provided; investors should monitor upcoming quarterly reports closely for evidence of sustained operating leverage or balance sheet stabilization initiatives.

Sector trends such as digital advertising growth may offset traditional print declines, though company-specific revenue details are not available within provided data.

Key Milestones and Metrics To Watch

- Upcoming quarterly earnings releases aligned with typical reporting schedules [N1][N2]

- Potential debt refinancing or liquidity events hinted at via SEC discussions though details are limited [S9][S10][S18]

- Further corporate governance developments or incentive plan changes informing strategic direction [S16][S17]

- Operating cash flow trends relative to working capital management as indicators of cycle efficiency;

- Legal developments affecting risk profile given ongoing disclosures;

- Absence of formal forecasts necessitates close attention to proxy indicators within quarterly filings.

Analysis based on publicly available SEC filings [F1-S#] and news reports [N#] as of February 18, 2026; no estimates or investment advice provided.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments