enGene Holdings Expands $125M Loan Facility to Fuel Pivotal Phase 2 Gene Therapy Trial Milestones

enGene Holdings advances its lead gene therapy candidate with expanded financial backing and evolving clinical trial design.

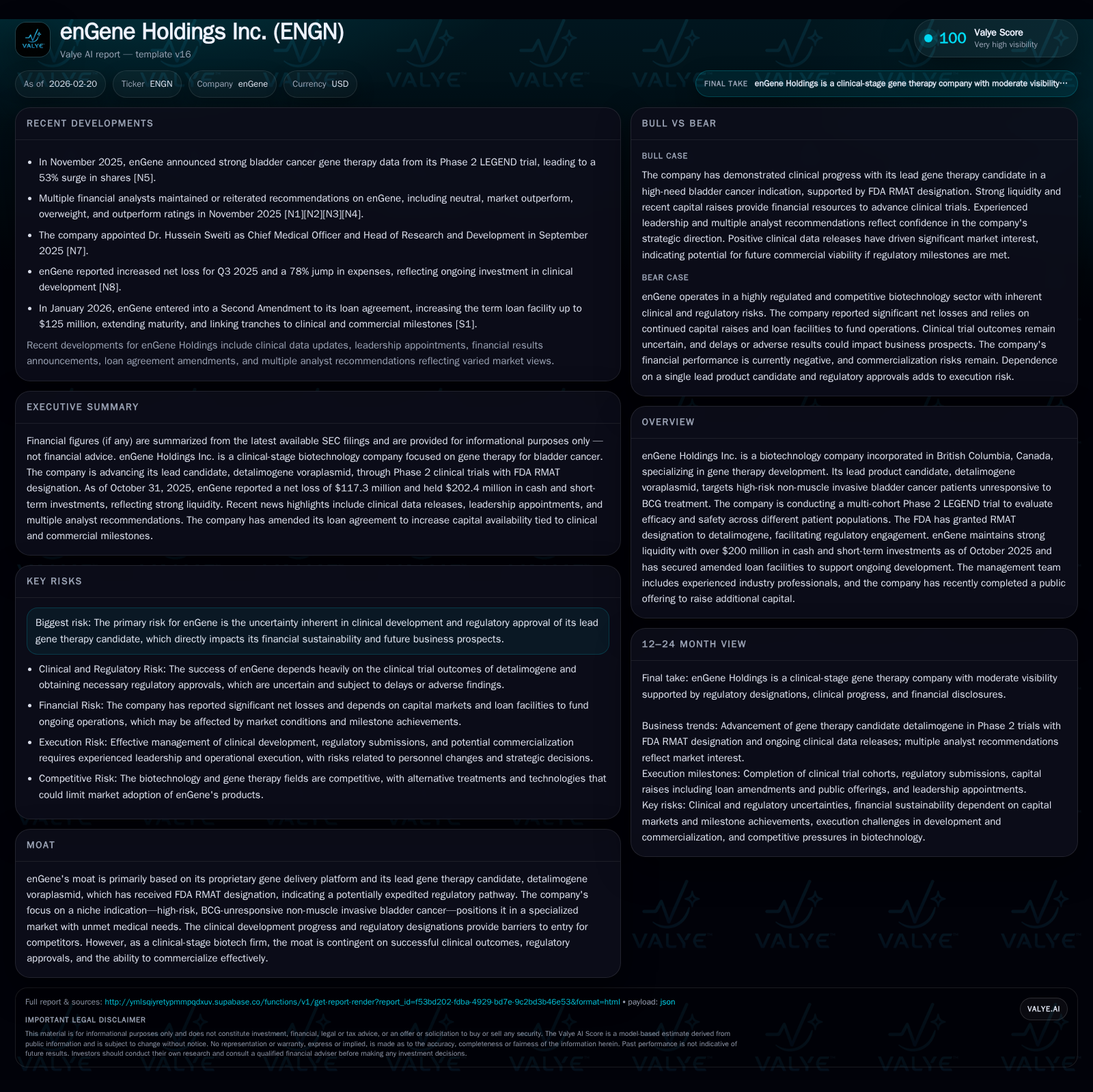

enGene Holdings Inc., a clinical-stage biotechnology company specializing in gene therapies for high-risk non-muscle invasive bladder cancer (NMIBC), experienced significantly increased operating losses in fiscal 2025 amid key clinical progress. The company raised approximately $130 million through an equity offering in late 2025 and amended its loan agreement to provide up to $125 million in milestone-contingent financing. With FDA RMAT designation for its lead candidate, detalimogene voraplasmid, enGene plans a Biologics License Application submission in the second half of 2026. Supported by strong liquidity, ongoing pivotal Phase 2 LEGEND trial activities continue, although substantial execution risks remain inherent to clinical development.

Company Overview

enGene Holdings Inc. is a clinical-stage biotechnology company developing gene therapies targeting challenging cancers such as non-muscle invasive bladder cancer (NMIBC). Its lead candidate, detalimogene voraplasmid, is designed for high-risk NMIBC patients who are unresponsive or inadequately treated with Bacillus Calmette-Guérin (BCG). The company operates primarily out of Canada and is listed on Nasdaq under the ticker ENGN. The FDA has granted RMAT designation for detalimogene voraplasmid, potentially expediting regulatory review.

Historical Financial Performance

As a pre-revenue biotech firm focused on clinical development, enGene's financials exhibit significant R&D-driven losses that have deepened over recent years:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -117 | -99 | -123 | 1485000 | -112.7% |

| 2024 | -55 | -48 | -62 | 925000 | +44.8% |

| 2023 | -100 | -25 | -26 | 318000 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -101 | -69.9 | |

| 2024 | 0 | -49 | -20.2 |

| 2023 | 0 | -25 | -137.8 |

Source: SEC companyfacts cache [F1].

Note: Revenue data are not available in provided filings.

The operating loss nearly doubled from FY2024 to FY2025 (a -97.7% year-over-year change), driven by expanded clinical trial enrollment and operational scale-up necessary for the pivotal Phase 2 LEGEND study [F1]. Net income worsened similarly due largely to increased R&D expenses and administrative costs associated with being a publicly reporting entity.

Operating cash flow turned more negative by over 100% YoY reaching -$99 million in FY2025, illustrating intensive cash burn supporting drug development without offsetting revenue inflows at this stage. Capital expenditures increased moderately as the company invested further in laboratory infrastructure and technology platforms.

Equity decreased materially from $272.6 million at FY2024 year-end to $167.7 million at FY2025 year-end primarily due to accumulated net losses despite recent equity raises [F1][S16]. This reflects the capital-intensive nature of early-stage biotechnology development.

Capital Structure and Liquidity Position

enGene held robust liquidity as of October 31, 2025 with cash and equivalents totaling approximately $50.2 million and current assets exceeding current liabilities by a factor of about 6.3x [F1], supporting ongoing pivotal trial activities.

In November 2025, the company completed an underwritten public offering raising approximately $130 million gross proceeds through common shares and pre-funded warrants priced near $8.50 per share [S16][S22]. This financing supplemented internal resources addressing anticipated funding requirements.

Simultaneously, enGene amended its term loan facility with Hercules Capital and other lenders increasing total borrowing capacity from $50 million up to $125 million [S4][S5]. The amended loan agreement provides for multiple tranches contingent upon achieving defined clinical milestones (e.g., pivotal Phase 2 cohort endpoints), regulatory milestones including FDA approval steps, and commercial milestones signaling readiness for market launch.

The loan bears interest payable monthly at rates indexed to prime plus fixed spreads capped near ~10%, with upfront facility fees ranging from approximately 0.50% to 0.75%. Additionally, the company issued warrants representing roughly 1.5% coverage tied to advances made under the facility exercisable at prices around $9.18 per share [S8][S12].

This structured financing approach balances dilution risk against non-dilutive debt capital while providing operational flexibility aligned with biotech sector norms where milestone-based funding is common given developmental uncertainties.

Clinical Development Progress and Future Outlook

enGene’s lead program focuses on detalimogene voraplasmid targeting high-risk NMIBC patients either unresponsive or naïve to BCG treatment—a population with limited therapeutic options often facing radical surgery or systemic therapies.

The ongoing LEGEND Phase 2 open-label study enrolls multiple cohorts differentiated by prior BCG exposure status:

- Cohort 1: BCG-unresponsive carcinoma in situ (CIS) ± papillary disease (pivotal cohort)

- Cohort 2a: Treatment-naïve CIS patients lacking adequate prior BCG treatment

- Cohort 2b: CIS patients inadequately treated with BCG

- Cohort 3: High-risk papillary-only BCG-unresponsive subgroup [S29]

Following FDA feedback, pivotal Cohort 1's primary endpoint shifted towards evaluating complete response (CR) at any time coupled with duration of response as key secondary endpoints—an alignment consistent with regulatory precedents for this indication [S29]. Preliminary safety data released November 2025 indicated manageable adverse events predominantly grades one/two without drug discontinuations due to severe toxicity [S28].

Regulatory strategy includes filing a Biologics License Application (BLA) by H2 calendar year 2026 leveraging RMAT designation benefits to expedite review [S24]. Approval would enable monotherapy use integrated into community urology settings where most NMIBC management occurs.

Commercial rights retention within the U.S., combined with selective partnering outside the U.S., positions enGene for strategic market access optimization globally [S24].

Beyond detalimogene, enGene pursues its proprietary DDX gene delivery platform aiming for broader applications delivering genetic medicines across mucosal tissues—reflecting a 'pipeline-in-a-product' approach enhancing long-term value creation [S24].

Capital Allocation and Return Metrics

enGene does not currently pay dividends nor engage in share repurchases consistent with typical early-stage biotechnology firms focused on pipeline advancement [F1][S27].

Return metrics indicate negative performance reflective of R&D investment intensity: approximate return on equity (ROE) stood near -69.9% for FY2025 based on net loss relative to shareholder equity [F1]. Free cash flow remains deeply negative; estimated at approximately -$101 million in FY2025 (operating cash flow less capex) underscoring reliance on external financing sources for liquidity maintenance.

Investor returns depend heavily on successful clinical outcomes de-risking regulatory submissions followed by commercial uptake contingent upon reimbursement dynamics within specialized oncology markets.

Risks and Considerations

the principal risks involve uncertain efficacy results from pivotal cohorts which could delay approval timelines or necessitate extended studies increasing capital consumption [S24][S26]. Intellectual property protection is critical amid competitive gene therapy pipelines targeting overlapping indications globally [S24]. Manufacturing scale-up feasibility post-approval remains an industry challenge impacting commercialization economics.

Changes in healthcare policy or payer acceptance introduce additional uncertainties affecting revenue potential beyond current disclosures.

Reliance on debt facilities and equity issuances emphasizes sensitivity to capital markets conditions which may fluctuate based on sector sentiment or macroeconomic factors.

Conclusion

enGene Holdings Inc exemplifies a late-stage pre-commercial biotechnology firm aggressively financing pivotal trials targeting niche oncology segments enabled by innovative genetic delivery platforms. Enhanced financial flexibility via amended credit facilities alongside successful equity offerings provides runway visibility into critical regulatory submission milestones scheduled later this year. Continuous monitoring of LEGEND study outcomes alongside milestone-linked tranche draws will be essential indicators of operational execution amid inherent industry risks surrounding trial success rates shaping enGene’s developmental trajectory. This analysis is strictly based on publicly filed information without extrapolative projections or investment recommendations.

Disclaimer: This report synthesizes publicly available SEC filings referenced herein and does not constitute investment advice or securities recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments