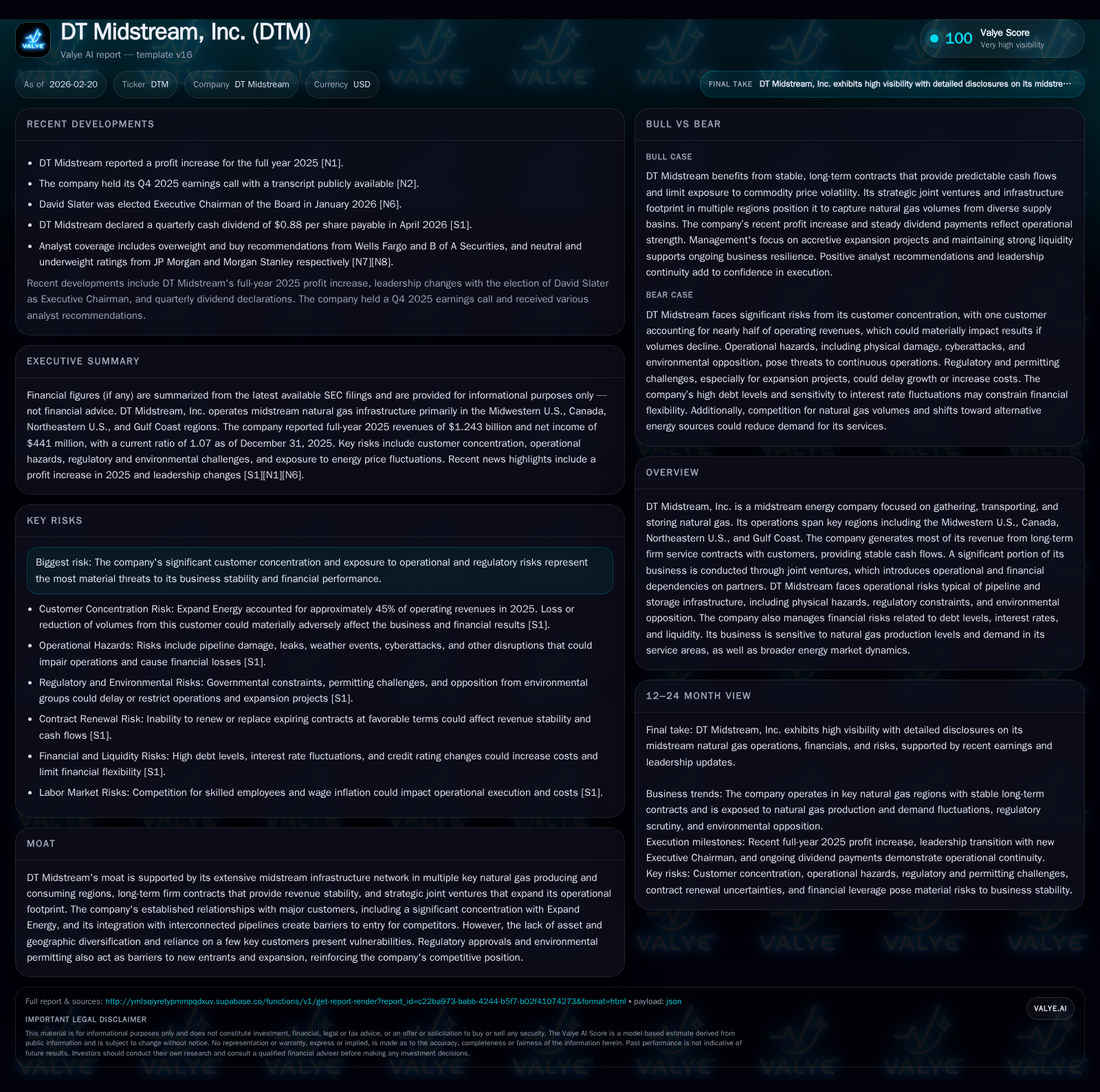

DT Midstream’s Growth and Cash Flow Strength Constrained by Customer Concentration and Regulatory Risks

A robust 2025 financial performance underscores DT Midstream's stable cash flow profile but highlights risks linked to customer concentration and evolving regulatory landscape.

DT Midstream, Inc. reported strong revenue and earnings growth in 2025 driven by long-term firm contracts and strategic infrastructure assets spanning key North American gas regions. Despite delivering a 26.7% revenue increase and expanding operating income by 25.6% year-over-year, the company’s heavy reliance on a single major customer, accounting for roughly 45% of operating revenues, poses concentration risk. Regulatory uncertainties and operational dependencies inherent to its midstream infrastructure footprint also remain key constraints on future growth. DT Midstream generated solid free cash flow supporting sustained dividend payments while navigating capital allocation amid increased Capex and managing debt levels approaching $3.35 billion.

Financial Performance Overview

DT Midstream demonstrated robust growth in fiscal year 2025, evidencing its ability to capitalize on its established midstream infrastructure and contractual framework. Revenues increased markedly by 26.7% year-over-year, reaching $1.243 billion [F1]. This growth was largely attributable to higher volumes gathered and transported across its network supported by long-term firm service agreements that underpin revenue consistency.

Operating income expanded by approximately 25.6%, arriving at $614 million for FY2025 [F1]. The company's operating margins benefited from the high proportion of firm service contracts typically structured with fixed demand charges or minimum volume commitments (MVCs), which provide protection against throughput variability and natural gas price fluctuations [S11]. Net income followed suit with a 24.6% rise to $441 million, indicating effective cost management despite broader inflationary pressures affecting operating expenses and capital costs [F1], [S10].

Operating cash flows grew by 13.6% to $867 million in the year ended December 31, 2025 [F1]. Capital expenditures increased by 21.7%, totaling $426 million as the company invested in maintaining and expanding assets reflective of midstream sector trends such as pipeline integrity management, compression facilities upgrades, and storage optimization [F1], [S13]. This investment level allowed DT Midstream to generate free cash flow (operating cash flow minus Capex) in the vicinity of $441 million—supporting liquidity and ongoing shareholder returns.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1243 | 441 | 867 | 614 | +26.7% | +24.6% |

| 2024 | 981 | 354 | 763 | 489 | +6.4% | -7.8% |

| 2023 | 922 | 384 | 798 | 471 | +0.2% | +3.8% |

| 2022 | 920 | 370 | 725 | 478 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 441 | 9.3 | |

| 2024 | 413 | 7.7 | |

| 2023 | 0 | 26 | 9.3 |

| 2022 | 3 | 387 | 9.2 |

Source: SEC companyfacts cache [F1].

Note: Dividends paid post-2021 are not available; share buybacks have been minimal.

Operational Footprint and Contractual Profile

DT Midstream operates an extensive network of pipelines, storage facilities, and gathering systems concentrated predominantly across the Midwestern U.S., Eastern Canada, Northeastern U.S., and Gulf Coast regions [S11]. While this footprint provides access to prolific natural gas basins, geographic concentration elevates exposure to regional production cycles, weather patterns, regulatory requirements, and market demand dynamics.

The company’s business model is anchored by long-term firm service contracts primarily composed of fixed demand charges or MVCs coupled with fixed deficiency fees—a structure that stabilizes revenues regardless of actual throughput fluctuations [S11]. This contractual setup offers insulation from commodity price volatility but includes renewal risk when contracts expire.

A material operational dependency lies in DT Midstream's relationship with Expand Energy, which contributed approximately 45% of consolidated operating revenues in fiscal year 2025 [S11]. This concentration introduces credit risk and volume volatility dependent on Expand Energy’s production activity or strategic decisions.

Joint ventures extend operational reach but add complexity through shared decision-making and financial outcomes (details not available in provided tags).

Industry-Specific Risks Impacting Growth Prospects

Growth prospects depend on sustained or increasing natural gas production within DT Midstream’s footprint alongside steady market demand for gas-fired power generation and industrial use.

However, several factors may constrain growth:

- Regulatory Environment: The Federal Energy Regulatory Commission (FERC) oversees interstate pipelines and is reviewing certification policies incorporating climate change considerations that may delay or complicate approvals for new projects or expansions [S20], [S16]. State-level regulations impose additional challenges including hydraulic fracturing controls potentially limiting upstream activity [S24].

- Environmental & Climate Considerations: Physical climate risks such as severe weather threaten infrastructure reliability while transition risks escalate compliance costs and could reduce demand through alternative energy adoption [S9].

- Operational Integrity: PHMSA pipeline safety mandates require ongoing inspections, repairs, integrity management investments, and compliance reporting that increase maintenance costs [S13], [S16]. Cybersecurity risks are emerging threats given reliance on digital control systems [S26].

- Customer Concentration: Heavy reliance on Expand Energy heightens vulnerability if contract terms become less favorable or if volumes decline due to drilling cutbacks or diversion [S11], [S1].

These risks reflect industry-wide challenges balancing capital-intensive infrastructure maintenance against uncertain production profiles shaped by commodity cycles and regulation.

Capital Structure and Liquidity

As of December 31, 2025, DT Midstream had approximately $3.35 billion in senior unsecured notes outstanding with no borrowings under its revolving credit facility providing liquidity flexibility [S4], [F1]. Debt agreements contain customary covenants offering reasonable operational latitude consistent with investment-grade credit profiles.

Interest expense exposure is mainly from fixed-rate notes; variable rate borrowings under revolving credit facilities would be sensitive to interest rate fluctuations if drawn upon [S4], [S6]. Rising interest rates pose headwinds affecting interest coverage ratios and refinancing conditions.

Liquidity metrics showed a current ratio near parity at approximately 1.07x supported by roughly $54 million cash alongside $318 million total current assets against $296 million current liabilities at year-end [F1], indicating capacity to meet short-term obligations though working capital buffers remain modest.

Returns Profile and Shareholder Distribution Policy

While explicit ROE disclosures are absent from filings, an approximation using net income over shareholder equity indicates a circa-9.3% ROE for FY2025—a moderate return typical for capital-intensive midstream utilities deploying steady but slow-growth assets [F1].

Information on dividends paid post-2021 is not available; share repurchases have been negligible suggesting retained earnings focus on Capex funding and debt servicing rather than aggressive distributions [F1]. Monitoring future disclosure for dividend policy updates will be important for assessing capital allocation strategy.

Future Growth Catalysts & Monitoring Points (Analysis)

Potential growth drivers include:

- Expansion projects boosting capacity or adding infrastructure within existing regions or adjacent basins.

- Favorable contract renewals sustaining or enhancing fixed fee revenues.

- Upstream recovery lifting drilling activity thereby increasing throughput volumes.

- Joint venture synergies contributing incremental EBITDA.

Negative catalysts could involve unfavorable contract renegotiations reducing tariffs or volumes; intensified regulation delaying projects; shifts in customer sourcing away from DT Midstream networks; or environmental incidents impacting operations.

Upcoming milestones include FY2026 quarterly operational results revealing volume trends post-renewal periods plus updates on FERC regulatory developments influencing project pipelines.

Strategic Considerations Regarding Risks

DT Midstream must balance maintaining high-quality infrastructure while managing concentration risk centered on few customers like Expand Energy who materially influence revenue stability. The company faces regulatory compliance cost escalation amid evolving climate policies while seeking measured organic growth fueled by rising natural gas use amid coal-to-gas fuel switching trends common in power generation sectors. Operational rigor addressing PHMSA pipeline integrity standards is critical given potential financial penalties for non-compliance including fines or reputational damage. Cybersecurity investments require prioritization due to growing digitization risks threatening operational technology environments.

Conclusion

DT Midstream delivered strong double-digit revenue and earnings gains in fiscal year ending December 31, 2025 supported by long-term contract structures underpinning consistent cash flows despite inflationary pressures. The company generated substantial free cash flow supporting ongoing Capex needed to maintain asset integrity within a complex regulatory environment. Nonetheless, significant concentration risk from reliance on a dominant customer (~45% revenues), combined with regulatory uncertainties including FERC policy shifts and tightening environmental controls around natural gas production remains a fundamental constraint shaping its risk-reward profile going forward. Investors should closely monitor contract renewal outcomes, regulatory developments especially related to pipeline certifications and emissions policies, upstream activity affecting throughput volumes as well as capital allocation decisions concerning dividends versus leverage management.

This analysis is based solely on publicly available information from company filings as of early 2026 combined with sector-specific contextual knowledge; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments