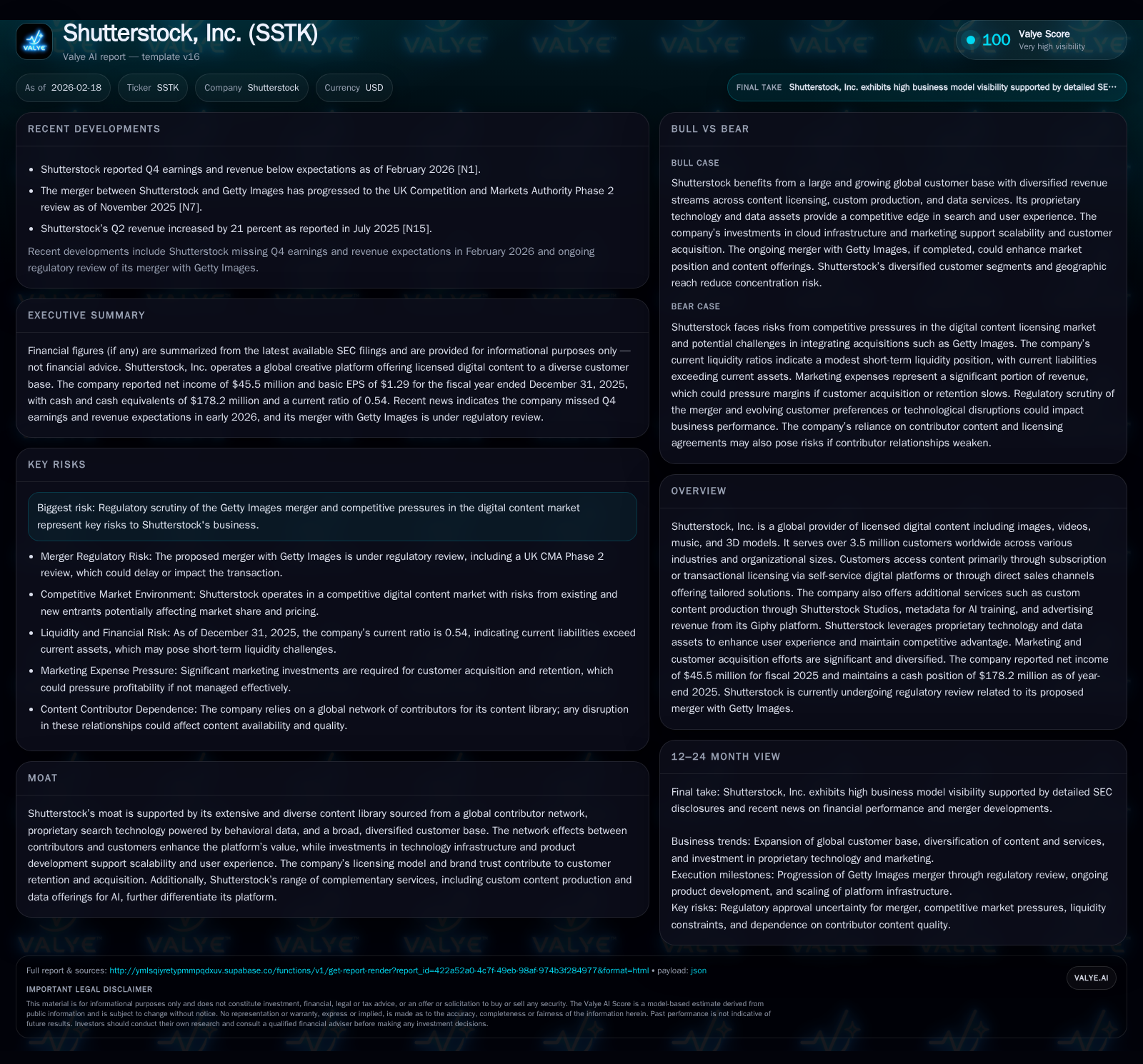

Shutterstock’s Growth Challenges and AI-Driven Content Expansion in a Competitive Market

Shutterstock faces growth headwinds following recent earnings misses but leverages AI content and strategic services amid regulatory and competitive constraints.

Shutterstock, Inc. operates one of the world's largest digital content marketplaces, providing licensed images, videos, music, and 3D models globally. After steady operating income growth, it posted mixed earnings results with net income up 27% year-over-year in 2025, while facing ongoing competitive pressure and regulatory scrutiny related to its Getty Images merger. The company is expanding AI-driven metadata offerings and custom content production services to sustain future growth. Strong operating cash flow supported dividends, though share buybacks paused recently, reflecting cautious capital allocation amid uncertain macroeconomic and regulatory environments.

Historical Performance and Revenue Drivers

Shutterstock has demonstrated a generally stable trajectory in operating income over recent years despite industry headwinds. The company increased operating income by approximately 9.2% to $75.1 million in fiscal year (FY) 2025 compared to relatively flat figures in FY2024 ($68.7 million) and FY2023 ($68.4 million) [F1]. This improvement points to operational leverage achieved through scale and improving cost controls amid reinvestments.

Net income also posted robust growth of roughly 26.6% in FY2025 to $45.5 million from $35.9 million the prior year — partly driven by better cost efficiency despite stiff competition [F1]. The company’s ability to sustain profitability underscores its effective monetization of licensed content across multiple product categories.

Operating cash flow climbed sharply by over fourfold from $32.6 million in FY2024 to $166.7 million in FY2025 [F1]. This surge provides operational liquidity cushioning against shrinking margins seen elsewhere in tech-focused marketplaces.

Capex declined modestly by approximately 9% to $42.9 million in FY2025 from $47.2 million the prior year indicating moderated investment intensity after infrastructure buildup for platform enhancements [F1].

Summary Financials

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 45 | 167 | 75 | 43 | +26.6% |

| 2024 | 36 | 33 | 69 | 47 | -67.4% |

| 2023 | 110 | 141 | 68 | 45 | +44.9% |

| 2022 | 76 | 158 | 94 | 43 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 47 | 0 | 124 |

| 2024 | 42 | 42 | -15 |

| 2023 | 39 | 28 | 96 |

| 2022 | 35 | 73 | 115 |

Source: SEC companyfacts cache [F1].

Note: Revenues were not available for disclosed periods beyond early quarters; buyback trends show program pause in latest year.

Business Model Nuances and Content Offerings

At its core Shutterstock operates a large-scale creative marketplace sourcing images, videos, music tracks, and emerging generative AI content from millions of contributors worldwide [S7][S14]. This broad content spectrum caters to diverse customer segments including corporate marketing teams, media companies, small businesses, social influencers, and individual creators [S5][S13].

Customers access content primarily through subscription plans or transactional licenses via self-service platforms or dedicated sales channels offering enhanced rights and workflow integration [S5]. This two-pronged model balances scalability with tailored enterprise solutions.

A key moat element lies in Shutterstock’s proprietary search technology powered by first-party behavioral data continuously refining relevance algorithms based on user interactions—a critical differentiation given the explosion of online visual content sources competing for attention [S16][S26].

Beyond stock content licenses, Shutterstock has strategically grown ancillary revenue streams: metadata licensing for machine learning AI training; ad-supported distribution via Giphy assets; and custom high-quality content creation through Shutterstock Studios—a vertically integrated service targeting brands needing scalable production support [S7][S13]. These avenues offer increasing margin enhancement potential versus commoditized stock downloads.

Industry Context and Competitive Dynamics

The digital content licensing market remains highly competitive with low entry barriers attracting numerous platforms from legacy Getty Images to tech-adjacent companies like AdobeStock and Freepik plus rapid innovation from AI-driven image generators such as Midjourney and DALL-E [S26].

Shutterstock faces pressure to maintain pricing power while investing heavily in marketing—spanning SEO, paid search campaigns, partnerships—and technology infrastructure to sustain user experience quality across languages and geographies [S12][S26].

Regulatory scrutiny around Shutterstock’s acquisition of Getty Images adds complexity pertaining to antitrust concerns and integration risks which may distract management focus or delay synergy realization [S20].

Geographic Reach & Customer Diversity

The company’s globally diversified revenues lower dependence on any single market: over half from North America (51%), followed by Europe (~27%), with remaining revenue from rest of world markets totaling ~22%—all contributing to risk diversification amid regional economic variability [S12][S16].

Customer concentration is limited; the aggregate top-25 customers accounted for less than 20% of total revenue in the last fiscal year supporting stable revenue streams without significant exposure to large single accounts losing business unexpectedly [S12].

Financial Position and Capital Allocation

Shutterstock maintains a healthy liquidity position with approximately $178 million cash and equivalents at year-end December 2025 coupled with revolving credit facilities totaling up to $250 million plus a $125 million term loan facility—providing ample financial flexibility despite sector cyclicality [S4][S6][F1].

Capital allocation reflects balancing shareholder returns through dividends alongside restrained share repurchases—the latter paused in FY2025 after sizable buybacks over prior years totaling upward of $40 million annually until recently [F1][S9]. Dividend payments grew modestly signaling commitment to shareholder income amid re-evaluation of capital deployment priorities under current market uncertainties.

Return on equity stands near an estimated ~7.8% based on net income relative to equity—a moderate level consistent with the competitive nature of licensing marketplaces requiring ongoing reinvestment into growth initiatives such as AI products and global localization efforts [F1].

Future Growth Prospects & Monitoring Points

Several factors could drive incremental expansion:

- Heightened adoption of AI-generated content licensing combined with metadata sales for training data opens new high-value use cases aligning with market trends towards generative AI adoption across media industries [N1][S7].

- Expansion of Shutterstock Studios’ custom production capabilities addresses growing demand from brands seeking efficient outsourced creative workflows bolstering recurring revenues at attractive margins.

- Continued investments enhancing search algorithm sophistication alongside multilingual platform capabilities improve stickiness among global users.

- Strategic partnerships or further acquisitions could broaden asset libraries or accelerate entry into adjacent market verticals.

Constraints include:

- Regulatory outcomes regarding the Getty deal may impose integration risks or additional compliance costs.

- Competition intensifying not only on pricing but also on technology innovation complicates customer retention efforts.

- Macroeconomic pressures impacting discretionary marketing budgets could dampen new customer acquisition rates as seen in recent quarterly earnings misses cited by management updates [N1].

Key Milestones To Watch (Analysis)

- Progress on integration with Getty Images’ assets including monetization of combined libraries.

- Growth trajectory and margin profiles from emerging AI-driven metadata products.

- Quarterly customer acquisition/retention metrics across subscription tiers.

- Regulatory developments related to merger approvals.

- Marketing spend efficiency versus return trends signaling sustainable unit economics.

Note: Specific forward-looking guidance or milestone timelines are not available in provided disclosures.

Conclusion & Disclaimer

Shutterstock operates at the intersection of digital creativity supply chains and accelerating adoption of artificial intelligence-powered content generation tools—a domain marked by rapid innovation but intense rivalry and regulatory oversight. Its established marketplace ecosystem coupled with diversified product suite including bespoke production services position it well for medium-term expansion opportunities though recent earnings softness highlights prevailing headwinds. The firm’s prudent capital stewardship reflected by solid operating cash flows funding dividends yet curtailing stock buybacks indicates a measured approach amidst evolving external challenges. This analysis is grounded entirely on publicly filed financials and company disclosures without recommendation toward investment action. Readers should conduct further due diligence considering broader market conditions before forming conclusions about Shutterstock's valuation or strategic outlook.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments