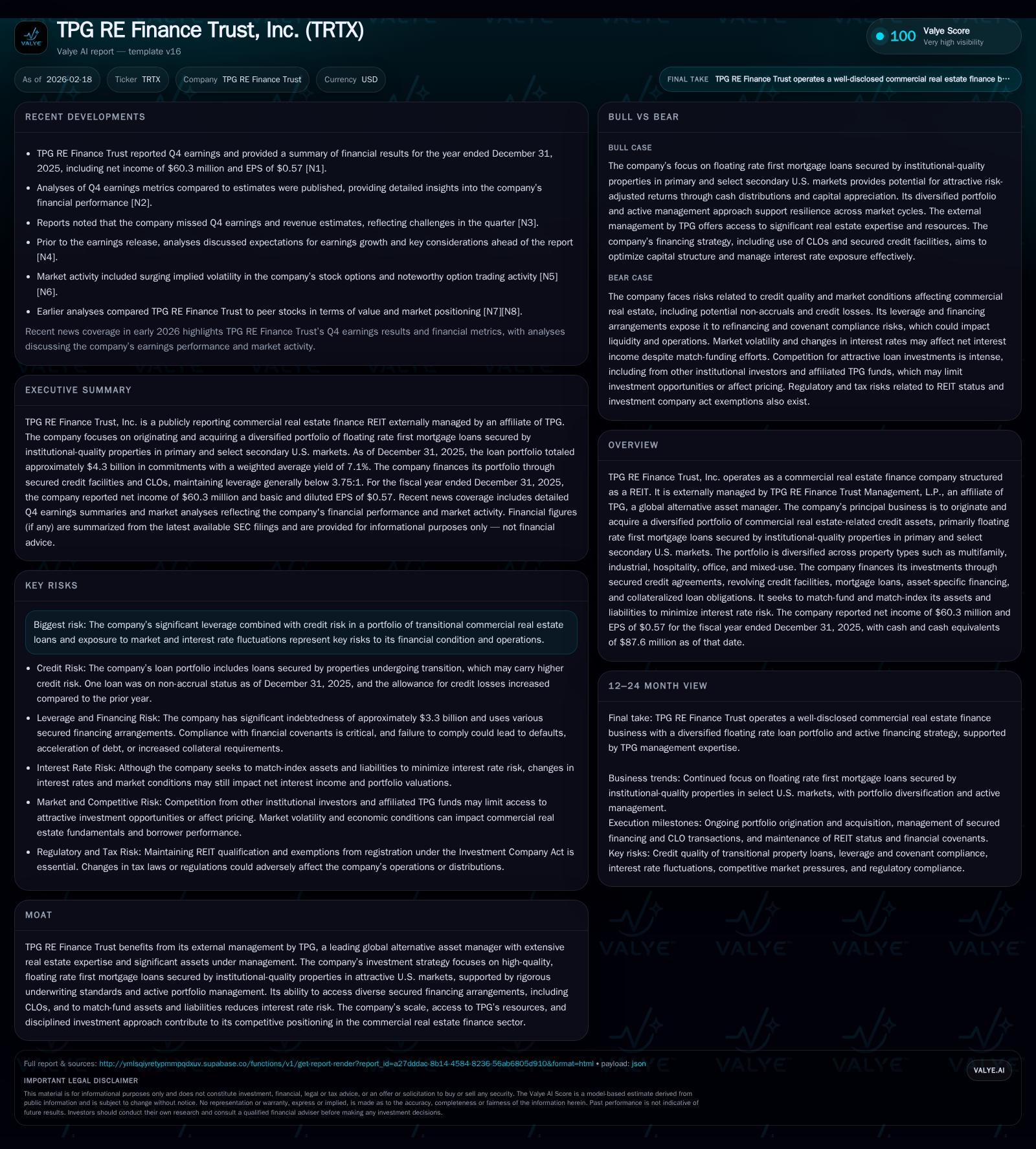

TPG RE Finance Trust's Financial Recovery and Strategic Financing in 2025

TRTX reversed multi-year net losses to achieve positive net income and robust operating cash flow in 2025, supported by disciplined portfolio and capital management.

TPG RE Finance Trust, Inc. (TRTX) demonstrated a significant financial turnaround in 2025 after posting substantial losses in 2022-2023. The company’s focus on floating rate first mortgage loans secured by institutional-quality properties, combined with strategic match-funding of liabilities and access to diverse secured financing avenues including CLOs, underpinned its recovery. While leverage remains substantial at approximately 3.1x debt-to-equity, TRTX improved returns on equity and expanded stock repurchases, signaling focused capital allocation amid prevailing risks from transitional asset credit quality and interest rate fluctuations. Going forward, monitoring covenant compliance, portfolio credit metrics, and capital market conditions will be key milestones.

From Losses to Positive Earnings: TRTX’s Turnaround in Net Income and Cash Flows

After enduring significant net losses through 2022 (-$60.1 million) and a sharper decline in 2023 (-$116.6 million), TRTX delivered a strong rebound with reported net income of $74.3 million in 2024 and $60.3 million in 2025 [F1]. This pivot illustrates enhanced operational efficiency paired with improved credit performance across the portfolio amid a recovering commercial real estate finance environment.

Operating cash flow (CFO) tracked positively throughout the period but showed moderation, peaking at $112.1 million in 2024 before settling at $90.4 million in 2025—a roughly 19% YoY decline likely reflecting more conservative credit conditions or timing variances in loan collections [F1]. Nonetheless, elevated CFO supports ongoing investment activity and shareholder distributions.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 60 | 90 | -18.9% |

| 2024 | 74 | 112 | +163.7% |

| 2023 | -117 | 80 | -94.2% |

| 2022 | -60 | 100 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc, Capex, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 25 | 5.6 |

| 2024 | 0 | 6.7 |

| 2023 | -10.4 | |

| 2022 | -4.5 |

Source: SEC companyfacts cache [F1].

Note: Dividends data not available; Capex generally negligible per historic filings.

Portfolio Composition and Credit Strategy: Floating Rate Mortgages Across Property Sectors

TRTX’s core portfolio strategy centers on first mortgage loans bearing floating interest rates indexed to one-month Term SOFR with credit spreads averaging roughly 320 basis points over benchmark rates [S10,S13]. The balance sheet comprised approximately $4.3 billion commitments across fifty loans as of December 31, 2025, with an unpaid principal balance near $4.12 billion [S13]. These loans are secured by institutional-quality properties primarily located in top U.S. metros like New York City, Los Angeles, San Francisco, Dallas, Phoenix, Miami among others—reflecting targeted geographic diversification within stable primary and select secondary markets [S12].

Property sector mix spans multifamily housing (largest segment), industrial warehouses, hospitality venues, office buildings under transition or repositioning strategies, as well as mixed-use developments offering diversified cash flow streams [S12]. Underwriting criteria emphasize moderate leverage with loan-to-value ratios around mid-60%s (65.7%) consistent with prudent risk-taking on transitional assets undergoing value enhancement initiatives like retenanting or refurbishment [S13,S8].

About half the loan book contains prepayment limitations such as yield maintenance clauses securing stable cash flow durations [S8]. This balances borrower flexibility with protection against early refunding risk for TRTX.

Leveraging Expertise: The Role of External Management by TPG in Investment Decisions

Serving as external manager since inception, TPG RE Finance Trust Management L.P., affiliated with alternative asset giant TPG Group boasting over $300 billion AUM across private equity and real estate platforms globally as of end-2025—brings substantial expertise and institutional scale advantage to TRTX’s business model [S1].

Management oversight is governed through an investment committee composed of senior TPG professionals who apply rigorous underwriting standards leveraging proprietary market insight for origination, acquisition decisions and active loan portfolio surveillance [S27,S15]. Additional synergy arises from access to TPG’s broader Real Estate platform—which manages over $38 billion—including private real estate credit funds enabling strategic sourcing coordination while adhering to strict duties-of-offer compliance among affiliated entities .

This structure affords TRTX differentiated access to secured financing alternatives (CLOs included), specialized underwriting protocols for transitional property credits alongside dynamic risk mitigation frameworks critical in fluctuating credit environments.

Managing Interest Rate Exposure: Match-Funding and Indexing Strategies

A cornerstone of TRTX’s financial engineering is precise match-funding whereby floating-rate assets indexed principally to one-month Term SOFR are paired closely with liabilities bearing identical benchmark indices—minimizing basis risk between asset yields and borrowing costs [S4,S7]. This match-indexing approach substantially buffers net interest income from volatility inherent in floating rate cycles.

Most borrowings (~82%) are structured without mark-to-market provisions ensuring stable balance sheet carrying values absent daily collateral calls due solely to market price swings on similar obligations—nonetheless ~18% do embed mark-to-market triggers typically linked to borrower collateral valuation declines rather than general interest rate shifts [S7]. There is notable absence of derivative instruments currently deployed for hedging purposes.

This tactical alignment means that increments in interest rates generally enhance net interest margins (given floating asset re-pricing), whereas downturns entail proportional income decreases modulated by effective floors embedded within loan agreements mitigating downside risk partially.

Capital Structure Overview: Debt Types, Covenants, and Leverage Metrics

TRTX’s capital structure is both diversified and complex reflecting a layered secured financing scheme totaling approximately $3.28 billion debt outstanding as of December 31, 2025 with principal components comprising collateralized loan obligations (CLOs) totaling nearly $2.6 billion (79%), secured credit agreements ($591 million), revolving credit lines ($31 million), plus asset-specific financings ($60 million) [S7,F1].

Financial covenants embedded within these agreements enforce constraints such as maximum total debt-to-equity ratios targeted below approximately 3.75x (currently nearer ~3.07x based on reported equity ~$1.07 billion) ensuring conservative leverage discipline adjusted dynamically per Manager’s discretion based on portfolio risk assessments [F1,S14,S16]._

The firm faces cross-default risks inherent in complex syndicated facilities whereby covenant breaches could precipitate accelerated paydowns or margin calls demanding additional collateral potentially disrupting liquidity unless remediated swiftly . A notable feature of securitization indentures is operational tests like overcollateralization ratios requiring potential diversion (“cash sweeps”) of loan proceeds away from distributions upon covenant stress scenarios affecting short-term distributable cash flow visibility for shareholders/fixed income investors.

Navigating Risk Factors: Credit, Market Volatility, and Regulatory Uncertainties

Principal risk exposures stem from credit quality given that many commercial mortgages finance properties undergoing transition phases subject to market-driven occupancy or rental volatility which affects borrower repayment capacity—heightened allowance for credit losses rose modestly from around $64 million at end-2024 to $77 million by end-2025 or ~180 basis points coverage on total commitments reflecting cautious reserving elevating loss protection margins slightly year-over-year [S20,S13].

The company maintains mechanisms for restructuring loans when warranted but acknowledges risk that valuations can deteriorate non-temporarily impinging cash flows leading potentially to foreclosures where properties become Recorded as REO assets currently aggregating around $237 million mostly comprising office and multifamily properties held temporarily pending disposition plans [S25,S12].

Additional risks include significant leverage exposure paired with concentration dynamics across certain metro areas combined with dependency on continued capital market liquidity availability given recent banking sector stresses impacting funding cost/timing dynamics going forward conditional on financing partners’ stability & regulatory landscape changes which could intensify compliance burdens or curtail permissible investment activities especially if classification under the Investment Company Act becomes suspect—a scenario management actively monitors to ensure ongoing exemptions intact protecting strategic flexibility .

Operational risks encompass reliance on TPG’s experienced investment personnel continuity plus cybersecurity safeguards given heavy dependence on integrated data processing systems administered externally likely constraining ramp-up speed if disruptions occur unexpectedly—a factor disclosed transparently by management limiting unilateral control but offset by TPG scale experience.

Capital Allocation Practices: Stock Buybacks, Dividends, and Equity Trends

In terms of capital return dynamics TRTX markedly increased common stock repurchase activity from inconsequential amounts ($37K) in FY24 to over $25 million in FY25 signaling confidence in intrinsic value relative to market pricing alongside prudent use of free cash generated despite no publicly disclosed dividends paid during the period leaving buybacks as primary shareholder return mechanism documented so far [F1].

Equity declined moderately from approximately $1.32 billion at end-2022 down to about $1.07 billion at end-2025 consistent partly with negative earnings periods earlier but also share repurchase outflows constraining book value evolution visibly influencing trailing return-on-equity calculations which approximate ~5.6% for fiscal year ended December 2025 reflecting underlying profitable pivot despite cyclical pressures balanced by capital return strategies supporting shareholder alignment absent dilution henceforth improvement signaled from previous impaired years [F1].

Robust operating cash flows further enable discretionary allocation flexibility but absence of explicit dividend policy disclosure requires attentive monitoring going forward.

Outlook and Key Milestones to Monitor in TRTX’s Next Reporting Period

While explicit guidance remains limited publicly scoped analytics emphasize several pivotal factors poised to govern near-term outcomes including:

- Maintenance of leverage within covenanted thresholds avoiding cross-default triggers particularly monitoring CLO coverage ratios along with secured facility debt yields amidst evolving credit spread environments,

- Continuation or moderation of stock repurchases balancing liquidity preservation versus opportunistic market valuation alignments,

- Monitoring non-accrual statuses especially the single multifamily property noted on watchlist signaling granular credit performance,

- Capacity for new originations sourced primarily through TPG platform leveraging competitive advantages against peers contending amid persistent competition from banks and other specialty finance entities,

- Vigilance towards macroeconomic developments impacting interest rate trajectories influencing net interest margins via SOFR adjustments,

- Regulatory landscape scanning addressing possible impacts from legislation affecting non-bank lender operations potentially altering permissible investment scopes or capital structuring norms [N1,N2,N5,S4,S20]

Investors should observe quarterly updates on portfolio health metrics including allowance adequacy changes plus realized loss levels; any unexpected margin calls or amended covenants triggering remedial actions; call activity on loans subject to prepayment penalties; additionally corporate governance disclosures relating to management continuity will remain important.

This analysis reflects information available based on SEC filings up to February 17th, 2026 and Nasdaq news sources as cited; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments