OPENLANE Advances Digital Automotive Remarketing Amid Financial Shifts

OPENLANE’s financial results reflect tension between technology investments and market conditions in the wholesale automotive remarketing space.

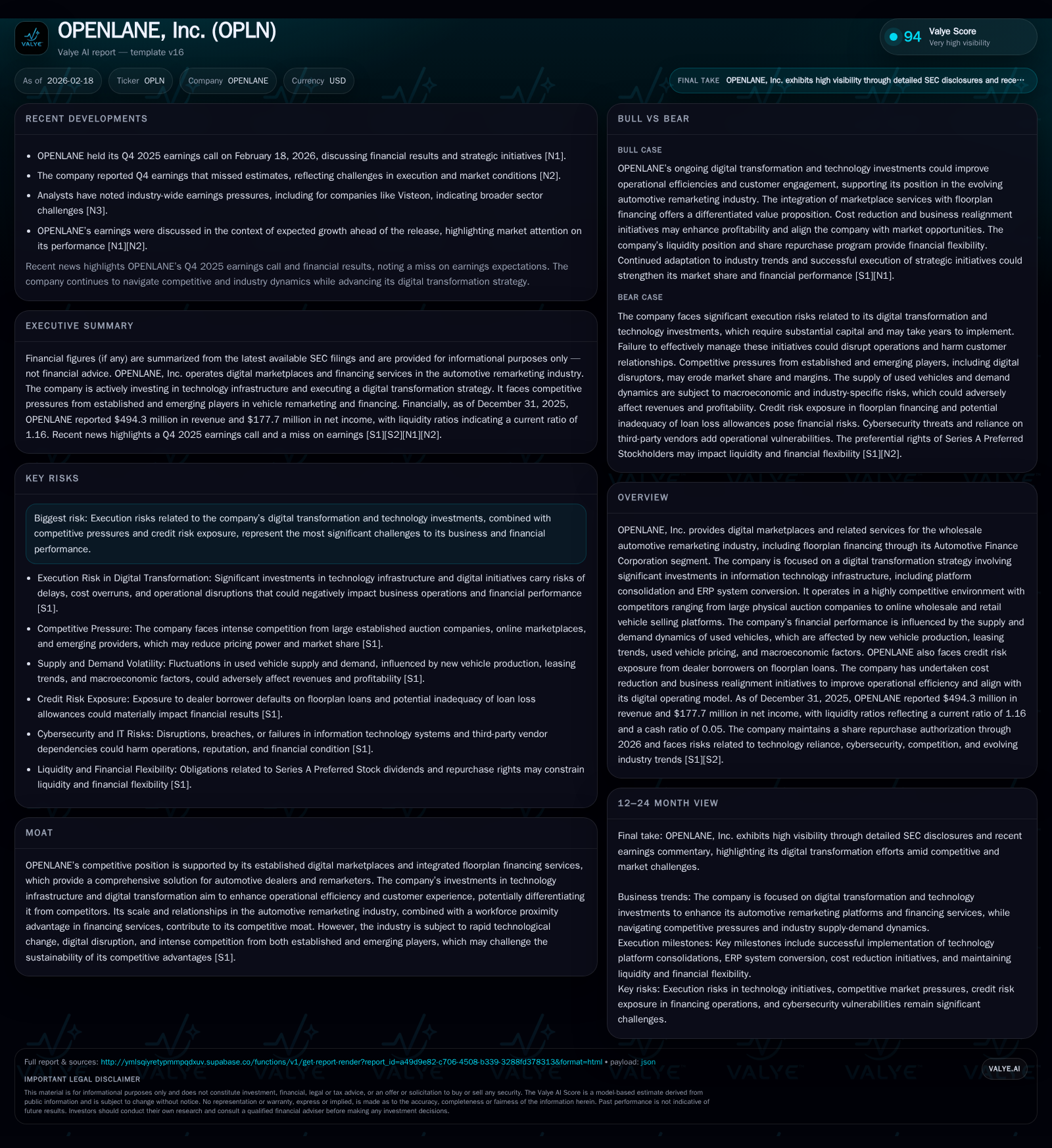

In FY2025, OPENLANE grew revenues by 8.6% to $494 million, yet operating income declined 46% amid significant IT infrastructure investments linked to its digital transformation strategy. Despite margin pressure, net income rebounded sharply due to factors including improved financing income. The company's integrated platform combining digital wholesale marketplaces and floorplan financing underpins its competitive moat but faces execution risks from ERP conversion and technology consolidation initiatives. Macroeconomic headwinds and used vehicle market dynamics continue to influence credit risk and operational performance. Capital allocation favors share repurchases over dividends, with ongoing liquidity pressures shaped by $550 million debt and revolving credit facility availability. Monitoring ERP milestone execution, operating margins, and credit loss trends will be key measures in 2026.

Historical Growth Trends: Revenue Expansion vs. Profit Volatility

OPENLANE has exhibited consistent topline growth over the four-year period ended FY2025, illustrating resilience in an evolving wholesale automotive remarketing landscape. Revenue increased from $372.8 million in FY2022 to $494.3 million in FY2025, marking an approximate compounded annual growth rate driven by marketplace transaction volume gains and rising floorplan financing activity [F1]. Specifically, FY2025 revenue advanced by 8.6% year-over-year from $455 million in FY2024.

However, profitability shows volatility reflective of strategic investments. Operating income declined materially from $79 million in FY2024 to $42.5 million in FY2025 (a 46% decrease) despite top-line expansion [F1]. This decline is attributed primarily to increased expenditures on technology infrastructure supporting the company’s digital transformation initiatives.

Conversely, net income rebounded strongly after a loss of -$154.1 million in FY2023 back into positive territory at $109.9 million in FY2024 and further up to $177.7 million (+61.7% YoY) in FY2025 [F1]. This bottom-line recovery likely reflects favorable capital structure impacts or non-operating items beyond core operations.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | OpInc ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 494 | 178 | 43 | 55 | +8.6% | +61.7% |

| 2024 | 455 | 110 | 79 | 53 | +16.3% | +171.3% |

| 2023 | 391 | -154 | 57 | 52 | +5.0% | -163.9% |

| 2022 | 373 | 241 | 88 | 61 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): CFO, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 46 | 14.3 |

| 2024 | 30 | 8.2 |

| 2023 | 22 | -11.6 |

| 2022 | 182 | 15.9 |

Source: SEC companyfacts cache [F1].

Note: Dividends were zero across all years based on available data.

Digital Transformation Strategy and Competitive Positioning

OPENLANE’s core strategic focus is executing a comprehensive digital transformation aimed at modernizing its information technology infrastructure to sustain leadership in digital remarketing integrated with floorplan financing.

The company is undertaking platform consolidation alongside an enterprise resource planning (ERP) system conversion intended to unify legacy systems into a scalable architecture that supports emerging technologies such as artificial intelligence [S1][S12]. These initiatives involve significant capital investment and carry execution risks including migration complexity, service disruptions, and integration challenges.

The digital marketplaces operated by OPENLANE provide dealer-to-dealer wholesale channels for used vehicles while Automotive Finance Corporation (AFC) offers complementary floorplan financing solutions proximal to customers—a synergy providing competitive differentiation against physical auction houses and online platforms alike [S13]. AFC competes primarily through quality of service, convenience, scope of offerings, and proximity to customers.

However, rapid technological disruption poses challenges as new entrants may leverage advanced digital capabilities faster than incumbents can transition legacy systems or build proprietary advantages [S1][S13]. Successful modernization will be critical for maintaining market position.

Used Vehicle Market Dynamics Shaping Demand and Risks

Fundamentals in the used vehicle segment remain volatile due to factors such as residual values of off-lease vehicles, new vehicle production shortfalls affecting upstream supply chains, leasing behaviors influencing return volumes, and macroeconomic conditions impacting consumer demand for used cars [S1].

These dynamics affect remarketing transaction volumes on OPENLANE’s platforms as well as collateral values securing AFC’s floorplan loans.

Inventory valuation shifts can cause cyclicality in credit risk exposure since dealer repayment ability is closely tied to used vehicle prices—impacting loan delinquencies or defaults during downturns [S18]. Thus, market conditions continuously influence both transactional revenues and credit portfolio performance.

Capital Allocation: Share Buybacks, Dividends, and Investment Priorities

OPENLANE’s capital allocation favors share repurchases over dividends—a pattern consistent over recent years.

In April 2025, the board approved up to $250 million for share repurchases through December 31, 2026 via open-market or negotiated transactions under Rule 10b5-1 compliant plans [S5][S6][S15]. Approximately $45.6 million was repurchased during FY2025 compared with $30 million in FY2024 indicating increased buyback activity [F1].

No dividends have been declared recently per available data.

Capital expenditures remained stable around $50–$60 million annually aligned mainly with technology platform development supporting the digital transformation strategy [F1][S12], balancing investment needs with shareholder returns.

Liquidity and Debt Structure Pressures Amid Macroeconomic Headwinds

As of December 31, 2025, OPENLANE carried approximately $550 million of term debt excluding securitization liabilities not secured by general assets [S4][S8], which imposes restrictive covenants limiting additional borrowing despite approximately $410 million net revolver availability after letters of credit [S25].

Variable interest rates expose the company to potential increases in finance costs amid uncertain economic conditions affecting used vehicle demand patterns [S4][S25].

Liquidity management remains critical given cash flows must cover scheduled debt service alongside ongoing IT investments plus discretionary share repurchases.

Credit risk is a key concern stemming from exposure to dealer borrowers on floorplan loans who may face insolvency or repossession when market conditions deteriorate unexpectedly—a risk heightened by volatile consumer behavior influenced by inflation or economic slowdown [S18][S26].

Future Growth Outlook and Key Execution Risks

Management commentary highlights anticipated growth fueled by completion of digital platform upgrades along with expansions into adjacent remarketing services enabled by improved scalability [N1][N4]. However, clear quantitative guidance is not provided; instead milestones focus on staged ERP rollouts with benchmarks related to user adoption and operational stability.

Key risks include delays or cost overruns on IT migration projects potentially disrupting operations causing revenue losses or reputation damage; intensifying competition leveraging AI-powered tools; regulatory scrutiny especially regarding privacy laws affecting data-driven offerings; and maintaining disciplined credit underwriting within AFC amid fluctuating collateral values [S1][S7][N4].

Performance Metrics to Monitor in 2026

Investors should watch for:

- Operating margin trends post-digital investment absorption,

- Milestone achievements within ERP system conversion impacting throughput or customer satisfaction,

- Credit loss ratio developments within AFC’s loan portfolio reflecting dealer payment health,

- Progress against authorized share repurchase budgets,

- Cash flow adequacy balancing capex commitments with debt servicing obligations.

Note: Return on equity is approximately estimated at 14.3% based on latest net income ($177.7M) over equity ($1,240.7M) per fiscal year-end data; operating cash flow figures are available only for earlier years so current CFO trends cannot be conclusively assessed from provided tags; dividend payments have been zero recently while share buybacks totaled $45.6M in FY2025 indicating capital return policy focus but no dividend yield currently exists per available data [F1].

Disclaimer: This analysis is based solely on publicly available information as of February 18, 2026 without any investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments